Assessing Waste Management (WM) Valuation After Recent Share Price Softness

Waste Management, Inc. WM | 0.00 |

Recent share performance and business snapshot

Waste Management (WM) has traded softer recently, with the stock down about 5% over the past month and about 4% over the past 3 months, offering investors a chance to reassess the business.

The company reports annual revenue of US$25.4b and net income of US$2.8b. This reflects a large, diversified operation spanning collection and disposal, recycling, renewable energy, healthcare solutions, and other environmental services.

At a share price of US$217.90, WM has eased in recent months, with the 30 day share price return down 5.1%, while the 5 year total shareholder return of 68.2% points to a much stronger longer term journey. This suggests recent weakness reflects cooler momentum rather than a complete shift in how the market views its prospects.

If WM’s recent pullback has you thinking about where else to put fresh capital to work, it could be a good moment to broaden your search and check out 35 power grid technology and infrastructure stocks

With WM’s share price softer in the short term and tools like analyst targets and intrinsic value models pointing to some gap, the key question is simple: is this a genuine opportunity or is the market already pricing in future growth?

Most Popular Narrative: 14% Undervalued

On the most followed narrative, Waste Management’s fair value of $253.12 sits above the last close of $217.90. This puts the focus firmly on whether the market is underestimating its future cash generation under a 7.25% discount rate.

The company's strategic investments in sustainability, particularly in the areas of recycling and renewable energy, are showing strong, high-return growth, which could drive future revenue increases. The integration and optimization of WM Healthcare Solutions are on track to deliver significant synergies, anticipated to reach $250 million annually by 2027, positively impacting earnings.

Curious what kind of revenue and margin profile is needed to support that valuation gap? The narrative leans on steady compounding, higher profitability, and a richer future earnings multiple. The exact mix of growth and margins might surprise you.

Result: Fair Value of $253.12 (UNDERVALUED)

However, the picture can shift quickly if the integration of Stericycle drags on profitability or if regulatory changes raise costs for renewable energy and recycling projects.

Another way to look at valuation

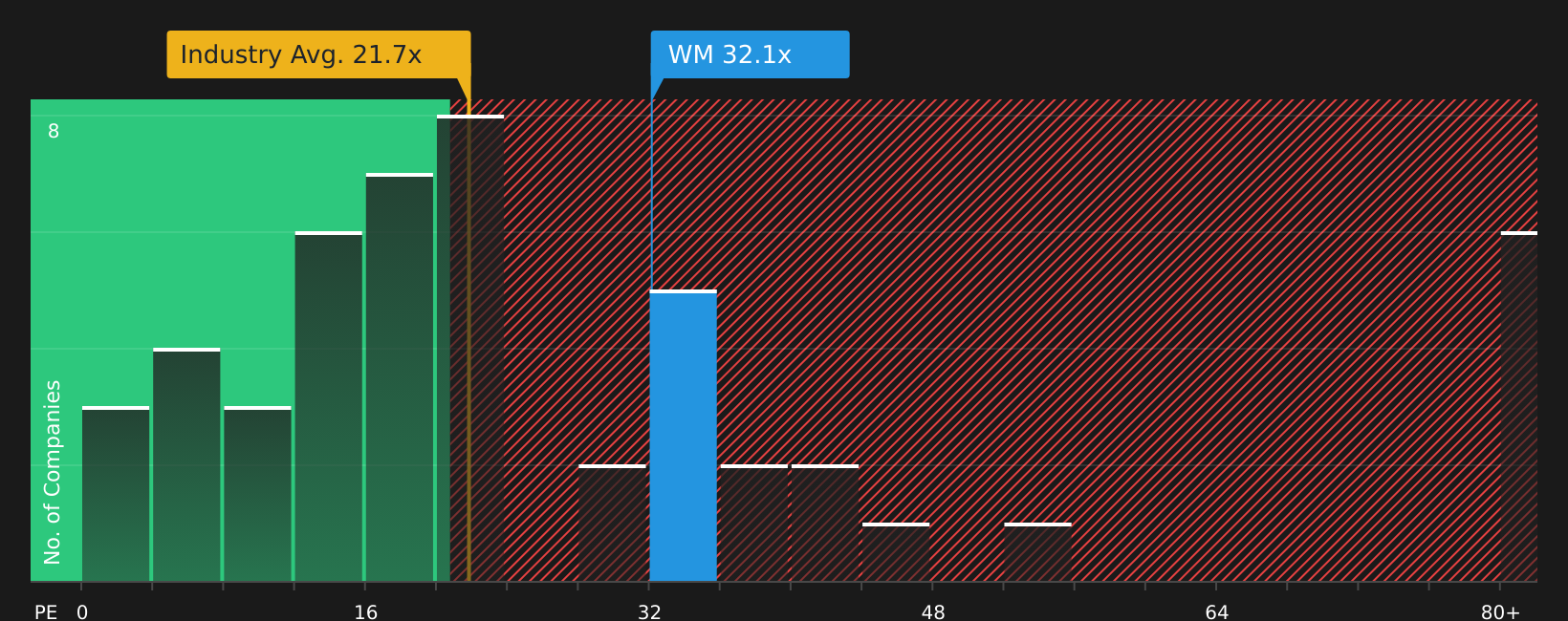

That fair value narrative suggests WM is undervalued, but the market is sending a different signal. The stock trades on a P/E of 31.3x, above the US Commercial Services industry at 22.4x and also ahead of its 29.9x fair ratio, which points to valuation risk rather than clear upside.

For a closer look at how those earnings multiples compare with what the fair ratio suggests the market could move toward, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With this mix of caution and optimism in mind, it may be helpful to review the data yourself in the near future and carefully consider both sides using 4 key rewards and 2 important warning signs

Looking for more investment ideas?

If WM is already on your radar, do not stop there. Broadening your watchlist now can help you spot opportunities before everyone else notices them.

- Target long term wealth building by focusing on quality at a fair price through the 48 high quality undervalued stocks.

- Strengthen your income stream by scanning for reliable payers using the 10 dividend fortresses.

- Prioritise resilience and capital preservation with the 68 resilient stocks with low risk scores before market conditions shift again.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.