تقييم شركة وييرهاوزر (WY) مع تأكيد خطة توزيع الأرباح على عوائد رأس المال

ويرهوزر كو WY | 0.00 |

أعادت شركة وييرهاوزر (WY) التركيز على الأرباح بعد أن أعلن مجلس إدارتها عن توزيع أرباح نقدية أساسية ربع سنوية قدرها 0.21 دولار أمريكي للسهم الواحد. ومن المقرر صرف الأرباح في 22 يونيو/حزيران للمساهمين المسجلين في 5 يونيو/حزيران.

على الرغم من هذا التركيز المتجدد على العوائد النقدية، إلا أن أداء سهم شركة وييرهاوزر كان ضعيفًا مؤخرًا، حيث أغلق عند 22.68 دولارًا أمريكيًا، وانخفضت عوائد السهم خلال يوم واحد وشهر واحد وثلاثة أشهر. كما كانت عوائد المساهمين الإجمالية على مدى سنوات سلبية، مما يشير إلى تراجع الزخم على الرغم من إطار توزيع الأرباح.

إذا دفعتك هذه القصة المتعلقة بالدخل إلى التفكير في أماكن أخرى قد تختبئ فيها القيمة، فقد تكون هذه لحظة جيدة لتوسيع نطاق بحثك واكتشاف أفضل 19 شركة يقودها مؤسسوها

مع انخفاض سهم شركة Weyerhaeuser لأكثر من يوم واحد، وشهر واحد، وثلاثة أشهر، وعلى مدى سنوات عديدة، ومع ذلك يتم تداوله بخصم عن أهداف أسعار المحللين، فهل يشير هذا الضعف إلى فرصة استثمارية مربحة مقومة بأقل من قيمتها الحقيقية، أم أن السوق قد أخذ في الحسبان بالفعل نموها المستقبلي؟

الرواية الأكثر شيوعًا: 28.1% أقل من قيمتها الحقيقية

مع إغلاق سهم شركة Weyerhaeuser عند 22.68 دولارًا مقابل القيمة العادلة المتوقعة البالغة 31.55 دولارًا، فإن سعر السهم الحالي أقل بكثير مما يعتبره هذا الرأي الذي يحظى بمتابعة واسعة معقولًا، مما يخلق توترًا واضحًا بين تسعير السوق وإمكانات التدفق النقدي المتوقعة.

تمثل اتفاقية احتجاز الكربون وتخزينه مع شركة أوكسيدنتال بتروليوم فرصة نمو في قطاع حلول المناخ الطبيعية التابع لشركة وييرهاوزر، ومن المرجح أن تعزز الأرباح المستقبلية. وسيؤدي استمرار أعمال بناء منشأة EWP في أركنساس وعودة العمليات إلى طبيعتها في منشأة مونتانا إلى زيادة الإنتاج، مما سيؤثر إيجاباً على الإيرادات وصافي الأرباح.

هل ترغب في معرفة كيف يساهم توسع أعمال حلول المناخ ومنتجات الأخشاب الهندسية ذات القيمة العالية، إلى جانب هوامش ربح أكبر وأرباح أسرع، في تبرير فجوة القيمة العادلة هذه؟ يُفصّل التقرير مسار الإيرادات، ومستوى الربح، ومضاعف التقييم التي يجب أن تتوافق لتقليص الفجوة بين 22.68 دولارًا و31.55 دولارًا.

النتيجة: القيمة العادلة 31.55 دولارًا (أقل من القيمة الحقيقية)

ومع ذلك، يمكن أن تتغير قصة القيمة العادلة هذه بسرعة إذا أدى ضعف الطلب على الأخشاب أو القيود التجارية الدولية إلى انخفاض الأحجام وهوامش الربح بشكل أكبر مما يفترضه المحللون حاليًا.

طريقة أخرى للنظر إلى التقييم

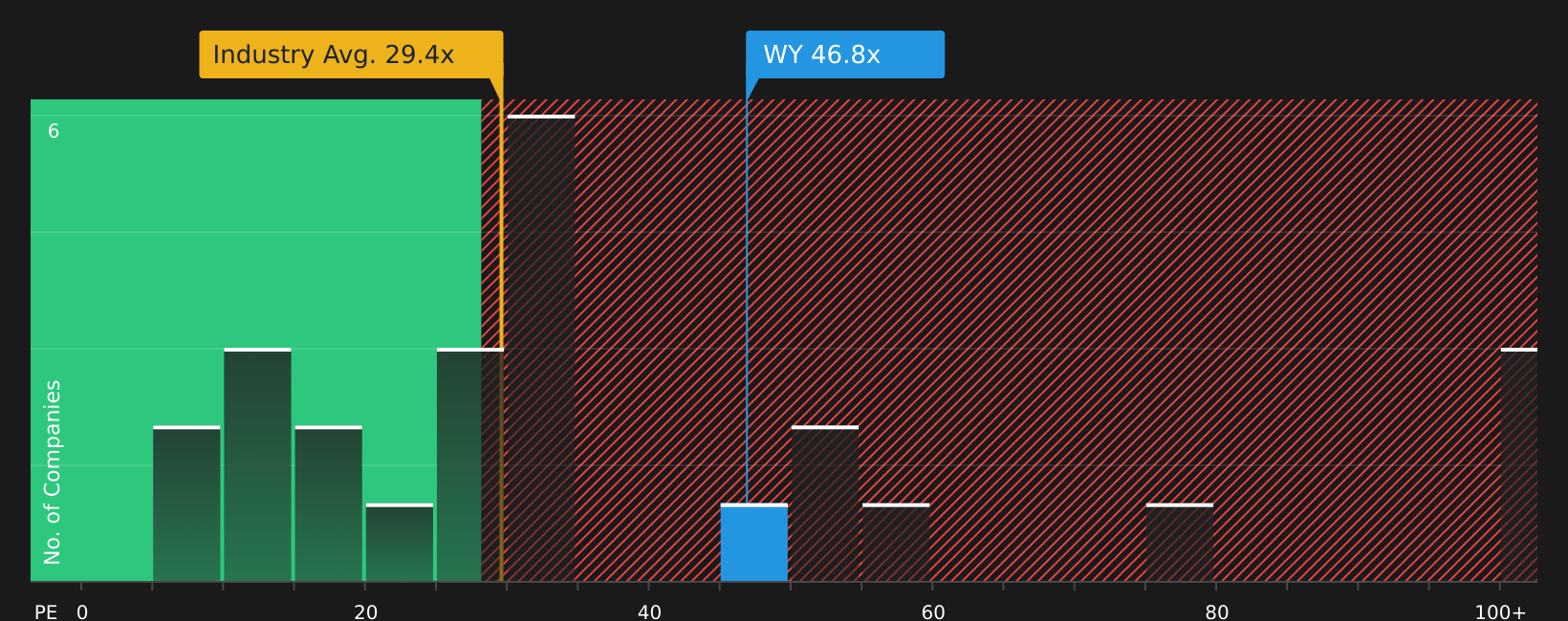

تشير القيمة العادلة المتوقعة البالغة 31.55 دولارًا إلى إمكانية ارتفاع السعر، لكن نسبة السعر إلى الأرباح الحالية البالغة 41.2 ضعفًا تتجاوز أيضًا متوسط نظيراتها البالغ 39.8 ضعفًا ومتوسط صناديق الاستثمار العقاري المتخصصة في الولايات المتحدة البالغ 29.3 ضعفًا، على الرغم من أنها أقل من النسبة العادلة البالغة 44.4 ضعفًا. فهل يمثل ذلك هامش أمان أم مبالغة في التقييم؟

لمعرفة كيفية مقارنة مضاعفات الأرباح هذه بمزيد من التفصيل، بما في ذلك ما قد يعنيه إذا اقتربت نسبة السعر إلى الأرباح من النسبة العادلة ومستوى الصناعة، ألق نظرة فاحصة على ما تقوله الأرقام عن هذا السعر - اكتشف ذلك في تحليل التقييم الخاص بنا.

الخطوات التالية

إذا جعلك هذا المزيج من إمكانات الدخل، وتساؤلات التقييم، وتغيرات المزاج العام، تشعر بعدم اليقين، ففكر في مراجعة المكافآت الرئيسية الثلاث وعلامات التحذير المهمة الثلاث على الفور.

هل أنت مستعد لإيجاد فكرتك التالية؟

إذا حسّنت شركة وييرهاوزر تفكيرك، فلا تتوقف هنا. وسّع قائمة مراقبتك الآن وامنح نفسك المزيد من الخيارات قبل الخطوة التالية.

- استهدف الشركات ذات التدفقات النقدية القوية والعوائد الثابتة من خلال الاطلاع على قائمة الشركات الـ 12 التي توفر توزيعات أرباح قوية .

- ابحث عن الشركات ذات الجودة العالية التي قد يتم تداولها بأقل مما تشير إليه أساسياتها من خلال قائمة تضم 50 سهماً عالي الجودة مقوم بأقل من قيمته الحقيقية .

- أعط الأولوية للاستقرار والقوة المالية من خلال مراجعة الشركات في أداة فحص الأسهم ذات الميزانية العمومية القوية والأساسيات (45 نتيجة) .

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.