Assessing Williams-Sonoma (WSM) Valuation After A Strong Multi-Year Share Price Run

Williams-Sonoma, Inc. WSM | 180.17 | -0.11% |

Williams-Sonoma: recent performance snapshot

Williams-Sonoma (WSM) has drawn fresh attention after a strong multi year total return profile, with the stock also showing gains over the past year, month, and past 3 months.

At a share price of $216.78, Williams-Sonoma has seen firmer momentum recently, with a 30 day share price return of 8.9% and a 90 day gain of 13.0%. Its three year total shareholder return of about 2.5x highlights how strong the longer term journey has been.

If this performance has you thinking about what else might be setting up for a strong run, it could be worth sizing up the 23 top founder-led companies as another source of potential ideas.

With shares at $216.78, slightly above both analyst targets and some intrinsic value estimates, the big question now is whether Williams-Sonoma still offers a compelling entry point or if the market is already pricing in future growth.

Most Popular Narrative: 9.1% Overvalued

Against the latest fair value estimate of about $199, Williams-Sonoma’s $216.78 share price sits on the richer side. This is exactly what the most followed narrative is trying to unpack using an 8.56% discount rate.

Supply chain optimization, including AI-driven forecasting, multi-sourcing strategies, and domestic manufacturing investments, is improving cost efficiency and order fulfillment, mitigating margin pressures from tariffs and global volatility and protecting net margins.

Curious how steady mid single digit growth, firm margins, and a higher future earnings multiple all come together to justify a premium price tag? The full narrative lays out the exact revenue path, profit profile, and valuation assumptions behind that fair value line.

Result: Fair Value of $199 (OVERVALUED)

However, that premium relies on housing related demand and tariff costs holding up, and either a weaker home spending backdrop or sharper tariff shocks could quickly challenge it.

Another angle on valuation

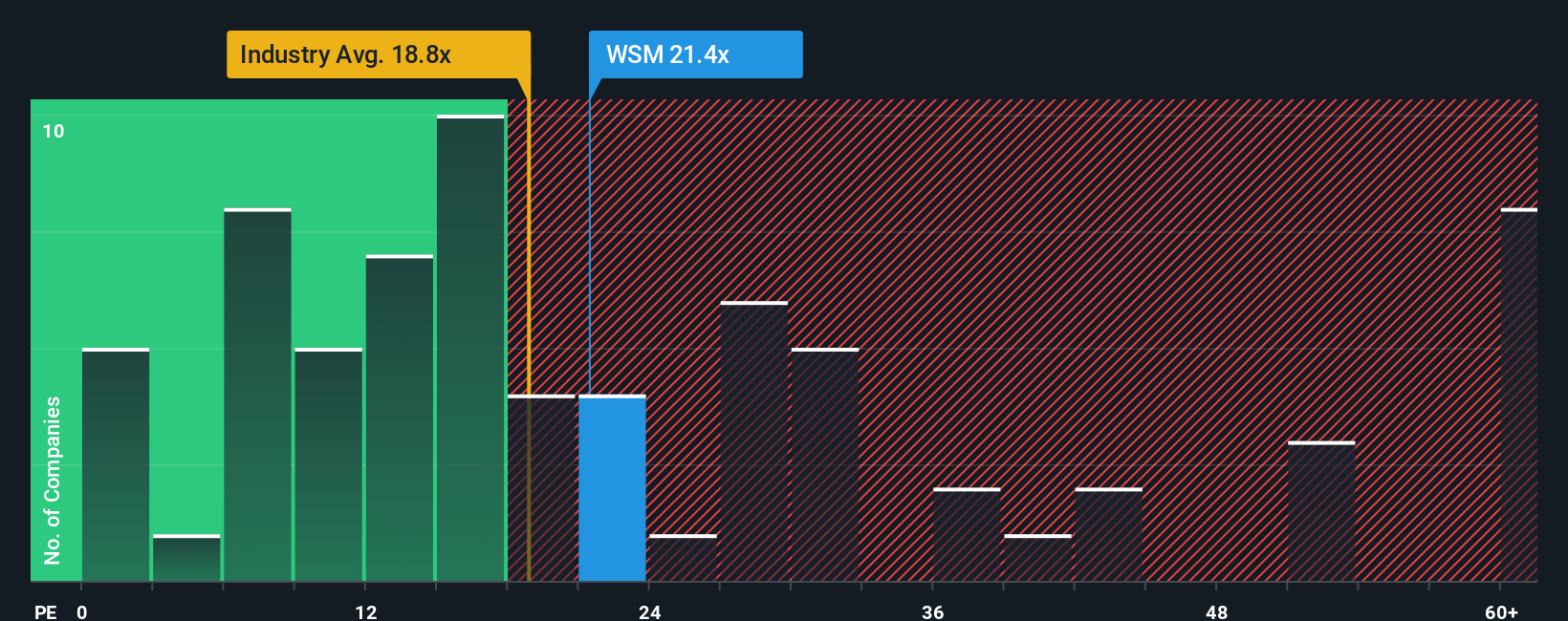

So far, the focus has been on fair value estimates around $199 that point to Williams-Sonoma looking about 9% overvalued at $216.78. The market’s own P/E tells a slightly different story.

On a P/E of 22.9x, Williams-Sonoma trades above the US Specialty Retail average of 20.7x and above its fair ratio of 17.1x, yet below peer levels of 25.6x. That mix implies investors are already paying up for quality, while still accepting less optimism than some peers. Is that a premium you are comfortable underwriting, or is it a signal to demand a wider margin of safety?

Build Your Own Williams-Sonoma Narrative

If you see the numbers differently, or if you prefer to stress test the inputs yourself, you can build a fresh Williams-Sonoma story in just a few minutes: Do it your way

A good starting point is our analysis highlighting 1 key reward investors are optimistic about regarding Williams-Sonoma.

Looking for more investment ideas?

If Williams-Sonoma has sharpened your focus, do not stop here. Broaden your watchlist with a few focused stock ideas that match how you like to invest.

- Target resilient value by checking companies our screener flags as 51 high quality undervalued stocks with solid fundamentals backing up their prices.

- Prioritize income potential by scanning 14 dividend fortresses that may help anchor your portfolio with regular cash returns.

- Protect your downside by reviewing 83 resilient stocks with low risk scores that score well on stability and risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.