ATI (ATI) Is Down 5.7% After Shift From Russell Value To Growth Indices Has The Bull Case Changed?

ATI Inc ATI | 0.00 |

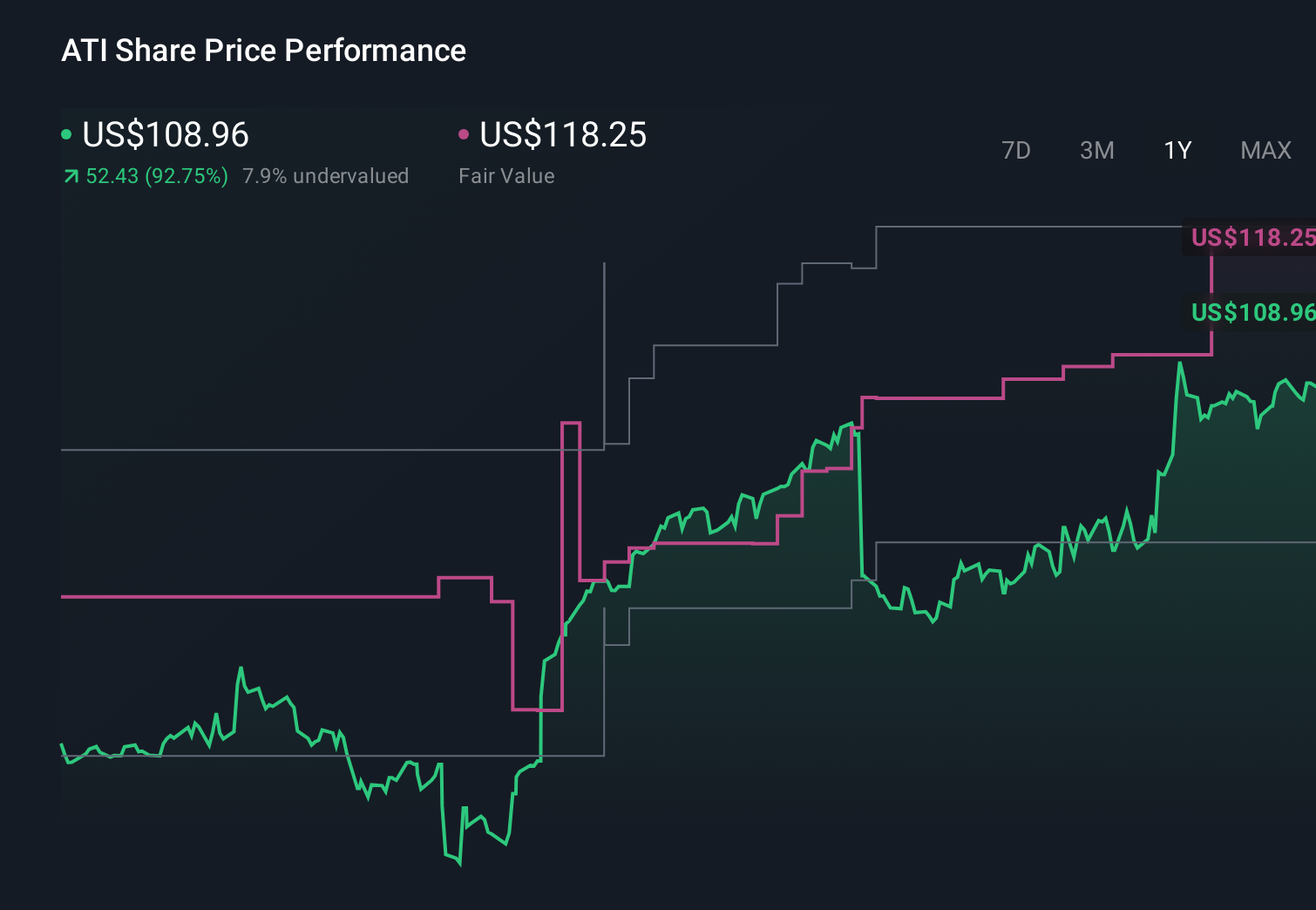

- On 27 June 2026, ATI Inc. (NYSE: ATI) was removed from multiple Russell value indices and simultaneously added to several Russell growth benchmarks, reflecting a reclassification of the stock within these widely followed index families.

- This shift into growth-focused indices coincides with improving analyst sentiment, multi-year revenue expansion, and stronger free cash flow margins that portray ATI as increasingly aligned with growth-oriented investors.

- We’ll now examine how ATI’s move from value to growth benchmarks reshapes its existing investment narrative and risk-reward profile.

The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

ATI Investment Narrative Recap

To own ATI today, you have to believe its aerospace and high-performance materials franchises can keep translating into rising earnings and cash generation, even as industrial and medical markets remain uneven. The shift into Russell growth indices mainly affects who owns the stock, not what drives the business. It does not materially change the near term focus on execution against long term Boeing and Airbus contracts or the key risk around capital intensity and customer concentration.

In my view, the most relevant recent development alongside this index move is ATI’s ongoing share repurchase program, with US$655.12 million spent to retire about 6.35% of shares so far. That capital return sits against catalysts like expanding jet engine content and defense demand, but also amplifies exposure if growth expectations embedded in a 60.3x P/E and ATI’s reliance on a few major aerospace OEMs prove too optimistic.

Yet behind the appealing growth label, ATI’s heavy dependence on a concentrated aerospace customer base is a risk investors should be aware of...

ATI's narrative projects $5.9 billion revenue and $862.2 million earnings by 2029.

Uncover how ATI's forecasts yield a $178.67 fair value, a 5% downside to its current price.

Exploring Other Perspectives

The most optimistic analysts were already counting on ATI to lift revenue to about US$6.1 billion and earnings to roughly US$932.8 million, so this shift into growth indices could either strengthen their case or expose how different your view might be from theirs.

Explore 6 other fair value estimates on ATI - why the stock might be worth less than half the current price!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your ATI research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free ATI research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate ATI's overall financial health at a glance.

No Opportunity In ATI?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Find 43 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 29 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.