Avista (AVA) On Leadership Change And A Valuation Story Pulling Two Ways

Avista Corporation AVA | 0.00 |

Leadership change at Avista and what it might mean for investors

Avista (AVA) stock is in focus after the company announced that Jason R. Thackston, Senior Vice President of Growth, Energy Policy and External Relations, plans to retire on January 1, 2027 and move to Whitworth University.

For investors, this planned transition raises practical questions about how responsibilities around growth initiatives, energy policy and external relations may be reassigned over the coming months, and how that could influence views on Avista’s risk profile and long term direction.

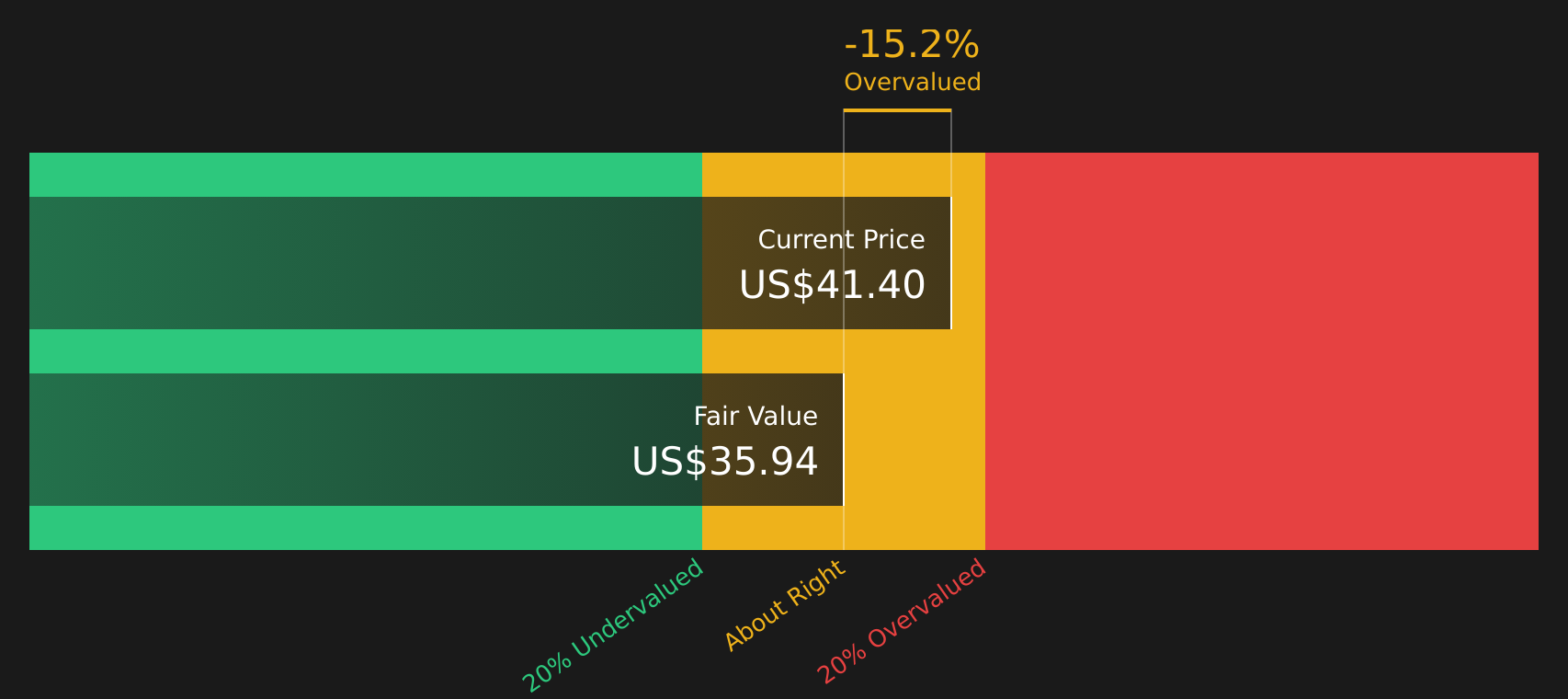

At a share price of $41.40, Avista has seen a 1-day share price return of 2.12%, while its year to date share price return of 6.92% sits alongside a 1-year total shareholder return of 13.34%. This suggests steady momentum supported by dividends over recent periods rather than a sharp rerating around this leadership update.

If this leadership transition has you thinking about where utilities fit within the broader energy system, it could be a useful moment to scan potential opportunities in 35 power grid technology and infrastructure stocks

With Avista trading close to its US$41.67 analyst price target and an intrinsic value estimate that sits around 15% above the current price, the key question is whether there is still a buying opportunity here or if the market is already pricing in future growth.

Most Popular Narrative: 3.3% Undervalued

Based on the most followed narrative, Avista's fair value of $42.80 sits modestly above the last close at $41.40, which frames this leadership update against a view of slight undervaluation grounded in long term earnings and revenue expectations.

The sharp rise in large industrial and commercial load inquiries, over 3,000 megawatts in the pipeline compared to a roughly 2,000-megawatt current peak load, signals accelerating electrification and potential for outsized rate base and revenue growth if even a fraction of these loads materialize over the next 3 to 5 years. Robust, multi-year capital investment plans approaching $3 billion (2025 to 2029), with additional upside from grid expansion projects and new generation needs tied to large load requests, position Avista to earn regulated returns and drive long-term earnings expansion.

Want the full story behind that fair value for Avista? The narrative leans on measured revenue growth, firmer margins, and a future earnings multiple that may surprise you. The real tension sits between those earnings assumptions and how regulators treat that multibillion dollar capital plan. The details sit in the projections, not the headline.

Result: Fair Value of $42.80 (UNDERVALUED)

However, Avista investors still need to watch for harsher regulatory outcomes or higher wildfire and grid resilience costs, which could pressure earnings and weaken the current fair value narrative.

Another View on Avista’s Value

While the fair value narrative places Avista close to $42.80, our DCF model suggests a different result with an estimate of $35.94, which would indicate that the stock is overvalued at the current $41.40. Which set of assumptions do you find more realistic for the next few years?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Avista for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across Avista's narratives, now is a good time to inspect the underlying data, stress test assumptions, and weigh both sides of the story with 4 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Avista?

If Avista has you thinking more broadly about your portfolio, this is the moment to widen the lens and line up your next set of candidates.

- Target reliability with 74 resilient stocks with low risk scores that aim to help keep portfolio swings in check while still giving you meaningful exposure to the market.

- Hunt for quality at a discount through screener containing 18 high quality undiscovered gems before the crowd starts paying closer attention.

- Position yourself for stronger balance sheet strength using the solid balance sheet and fundamentals stocks screener (47 results) so weaker companies are not quietly dragging on your results.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.