Babcock And Wilcox (BW) Stock Looks Undervalued On Sales But Stretched After Big Gains

Babcock & Wilcox Enterprises Inc BW | 0.00 |

Babcock & Wilcox Enterprises has delivered a very large 1 year gain, yet the stock still screens as undervalued on Simply Wall St’s broader checks, which sets up a clear question over how much of that rerating is already reflected in today’s US$10.73 share price.

- Over the past 1 year, Babcock & Wilcox Enterprises has returned about 9x an initial investment. This means even small changes in expectations can now have a bigger impact on valuation.

- The new alliance with TerraSpark Energy Campus for a West Virginia project can support expectations for future project revenue, while execution and capital needs on large energy infrastructure work may weigh on how much value investors are willing to pay for ahead of time.

- The stock is assessed as undervalued across 6 of 6 valuation checks, so the broader signals lean cheap rather than fully pricing in recent momentum.

The issue now is whether Babcock & Wilcox Enterprises’ recent surge has already pulled the stock close to fair value, or if the current price still leaves a margin that looks attractive on the available checks.

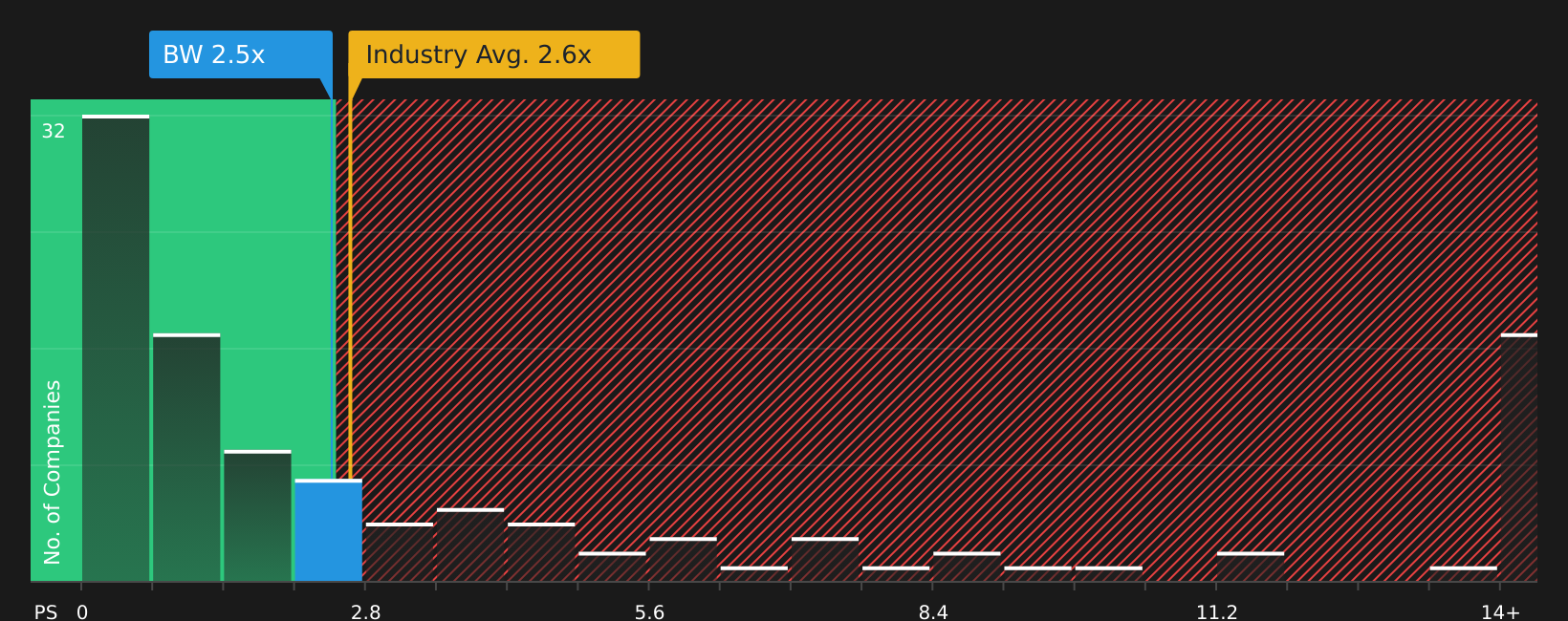

Is Babcock & Wilcox Enterprises Still Cheap on Sales?

P/S is a useful lens for Babcock & Wilcox Enterprises because revenue is often the cleaner yardstick for project focused industrial businesses that can swing between profits and losses.

At around 2.4x sales, Babcock & Wilcox Enterprises is trading very close to the Electrical industry average P/S of 2.5x, yet well below the peer group average of about 12.0x. The more tailored fair P/S ratio from Simply Wall St’s model sits at roughly 6.8x, which is materially higher than the current multiple and indicates the stock is priced at a discount to what that framework would expect given its characteristics.

Because the recent TerraSpark Energy Campus alliance and index inclusions have already drawn attention to Babcock & Wilcox Enterprises, the fact that the P/S ratio still sits below this fair multiple suggests that sentiment has not fully aligned with the revenue valuation yet.

On this P/S yardstick, Babcock & Wilcox Enterprises stock appears undervalued relative to both its modelled fair ratio and many peers.

The Babcock & Wilcox Enterprises Narrative: What Would Justify Today's Price?

For Babcock & Wilcox Enterprises, Simply Wall St Narratives pick up where the valuation puzzle leaves off by explaining which combinations of future growth, margins and earnings would need to hold for the stock to be worth significantly more or less than today’s price. Each narrative sets out a fair value as a thesis about the business that can be revisited over time, rather than as a one-off snapshot, on Simply Wall St’s Community page.

Community narratives on Babcock & Wilcox Enterprises sit far apart, with one side arguing the stock is materially undervalued and the other seeing it as stretched.

Bull case: 53% undervalued

"Analysts have raised their fair value estimate for Babcock & Wilcox Enterprises from $6.00 to $23.00, citing updated assumptions around future revenue growth, profit margins, discount rate, and P/E expectations as key factors behind the new price target range…"

Bear case: 29% overvalued

"The company is tying a large part of its long term story to AI data center power demand, including a US$1.5b Applied Digital project and a US$3b to US$5b AI opportunity pipeline…"

Do you think there's more to the story for Babcock & Wilcox Enterprises? Head over to our Community to see what others are saying!

The Bottom Line

For Babcock & Wilcox Enterprises, the valuation work points to a stock that still screens as undervalued on market multiples, even after a very sharp 1 year move. The key question is whether the current discount to the tailored P/S ratio reflects lingering caution about execution and capital demands on large energy and data center projects, or if the market is simply slow to reprice the revenue profile. From here, the crux of the bull versus bear debate is whether Babcock & Wilcox Enterprises can convert its project pipeline into reliable, higher quality revenue without eroding margins or overstretching its balance sheet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.