Babcock And Wilcox Enterprises (BW) Stock Could Be 21.5% Undervalued After TerraSpark Deal

Babcock & Wilcox Enterprises Inc BW | 0.00 |

Babcock & Wilcox Enterprises (BW) has drawn fresh attention after announcing a collaboration with TerraSpark on the TerraSpark Energy Campus in West Virginia, a large coal-fired power and rare earth extraction project backed by a U.S. Department of Energy grant.

Alongside the TerraSpark announcement and a new preferred dividend, Babcock & Wilcox Enterprises has seen strong momentum, with the share price delivering a 173.7% year to date return and a very large 1 year total shareholder return that is above 17x. The 30 day share price return is down 8.7%, hinting at some cooling after a sharp run.

If this kind of energy infrastructure story has your attention, it may be a useful moment to see how other grid related opportunities compare through the 34 power grid technology and infrastructure stocks

After a surge that has taken Babcock & Wilcox Enterprises to a market value of about US$2.6b, with the stock trading at US$17.38 and screens suggesting a possible discount, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 108.6% Overvalued

The most followed narrative for Babcock & Wilcox Enterprises sees fair value at $8.33, which is well below the last close at $17.38, creating a wide gap between price and narrative assumptions.

Rising North American electricity demand tied to AI data center growth is feeding into record bookings, revenue and gross profit in Global Parts & Services, which directly supports future revenue and gross margin resilience in the core business.

Curious what kind of revenue path, margin shift and long term earnings profile are baked into that fair value, and how much depends on AI power demand staying strong.

Result: Fair Value of $8.33 (OVERVALUED)

However, the Babcock & Wilcox Enterprises story still leans heavily on AI driven power demand and the successful delivery of large projects. Any setback in these areas could quickly reshape that overvaluation narrative.

Another View on Babcock & Wilcox Enterprises Valuation

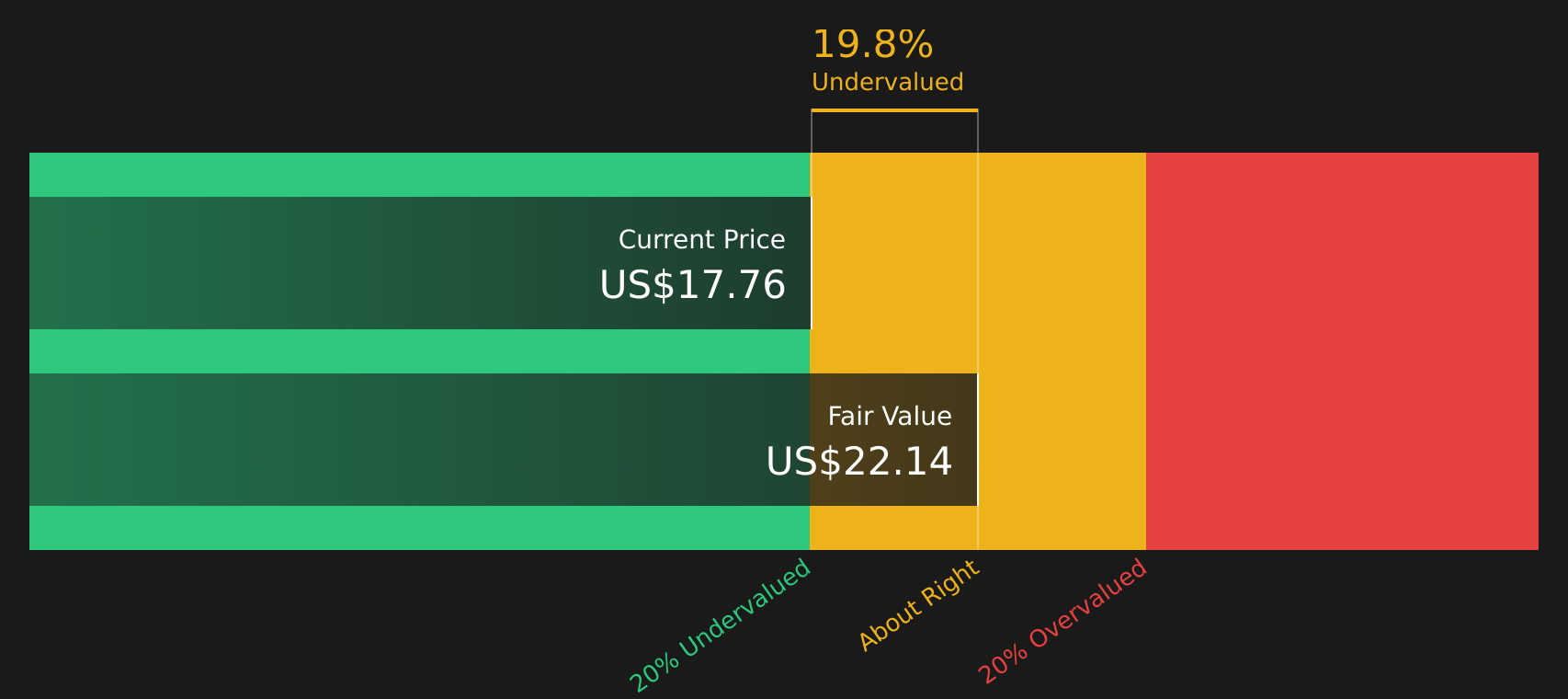

While the most popular narrative pegs Babcock & Wilcox Enterprises at a fair value of $8.33 and labels the stock overvalued, Simply Wall St's DCF model points in the opposite direction, indicating the shares are trading about 21.5% below its estimate of future cash flow value at $22.14. Which set of assumptions do you find more realistic?

Our DCF model does not rely on a single earnings multiple. It can help you stress test different cash flow paths and discount rates before deciding how comfortable you are with the current price relative to that $22.14 figure, especially given the AI related project pipeline and balance sheet considerations, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Babcock & Wilcox Enterprises for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With Babcock & Wilcox Enterprises pulled between risk-focused and reward-focused narratives, do not wait for consensus to form. Instead, assess the trade-off yourself by reviewing the 3 key rewards and 3 important warning signs.

Looking for more investment ideas beyond Babcock & Wilcox Enterprises?

If you are weighing the Babcock & Wilcox Enterprises story, this is also a good time to scan other opportunities and see how they line up on quality and risk.

Use the Simply Wall St Screener to quickly surface fresh ideas that match your style, so you are not relying on a single stock or narrative.

- Target potential upside with companies that combine strong fundamentals and attractive pricing by running a search through the 45 high quality undervalued stocks.

- Prioritise resilience by focusing on businesses with cleaner finances and sturdier profiles using the 66 resilient stocks with low risk scores.

- Hunt for potential future standouts before the crowd by scanning the screener containing 19 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.