Bandwidth (BAND) Is Up 8.2% After Salesforce Agentforce Win And Guidance Hike Has The Bull Case Changed?

Bandwidth Inc. Class A BAND | 0.00 |

- In the past quarter, Bandwidth reported stronger-than-expected Q1 2026 results and raised its full-year guidance, while being chosen to power Salesforce’s new Agentforce Contact Center platform for AI-driven enterprise communications.

- At the same time, several senior executives sold shares near recent highs, highlighting a contrast between upbeat operational momentum in AI infrastructure and insider equity trimming.

- Next, we’ll explore how the Salesforce Agentforce partnership may influence Bandwidth’s pre-existing investment narrative around AI-enabled communications growth.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Bandwidth Investment Narrative Recap

To own Bandwidth, you generally have to believe its pivot toward AI voice and orchestration (via Maestro and Communications Cloud) can offset pressures in commoditized CPaaS. The Salesforce Agentforce win and raised 2026 guidance reinforce AI as the key near term catalyst, while significant insider selling and a volatile share price keep execution risk and sentiment risk front and center. So far, the latest results and announcements appear to support, rather than alter, that core narrative.

The Salesforce Agentforce Contact Center partnership is the announcement that most directly ties into this quarter’s news. It puts Bandwidth’s AI-ready infrastructure at the core of a CRM-native, AI contact center, which many investors may view as real world validation of its platform story. At the same time, the busy insider selling tape around a steep share price run invites closer scrutiny of how sustainable these AI driven wins could prove to be.

Yet against this upbeat AI story, the pattern of insider selling is a reminder that investors should be aware of...

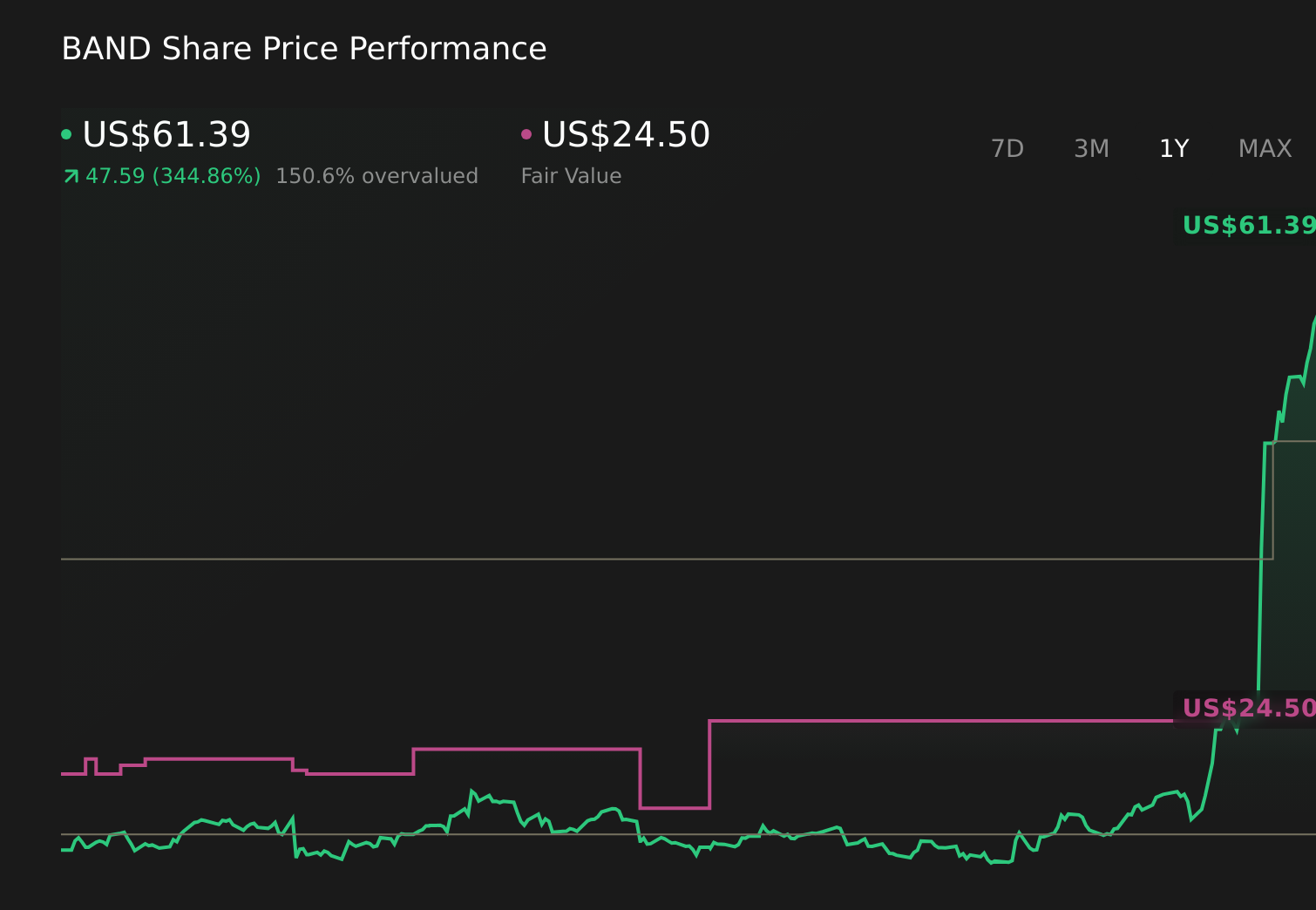

Bandwidth's narrative projects $987.7 million revenue and $17.8 million earnings by 2028.

Uncover how Bandwidth's forecasts yield a $24.50 fair value, a 55% downside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were assuming only about 7.8 percent annual revenue growth to roughly US$950.2 million and modest margin gains by 2028, so compared with the recent Salesforce driven optimism and raised guidance, their view looks much more cautious. As you think about this new AI contract and the broader shift toward Maestro, it is worth asking where you personally sit between those more pessimistic forecasts and the stronger narrative implied by recent results.

Explore 3 other fair value estimates on Bandwidth - why the stock might be worth over 2x more than the current price!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bandwidth research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Bandwidth research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bandwidth's overall financial health at a glance.

Seeking Other Investments?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- The future of work is here. Discover the 34 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 27 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.