Bank of America (BAC) Is Up 5.1% After Analyst Upgrades Spotlight Capital Strength And Payouts – Has The Bull Case Changed?

Bank of America Corp BAC | 51.88 | +3.18% |

- In recent days, Bank of America has been in focus after positive analyst coverage, including upgrades highlighting its capital strength, disciplined credit risk management, and ongoing dividend increases and share repurchases ahead of earnings season.

- These endorsements, combined with expectations for continued earnings consistency, have drawn attention to how Bank of America’s balance sheet discipline and capital return policies may influence investor conviction about its longer-term profitability.

- We’ll now examine how this renewed analyst confidence in Bank of America’s capital return strategy and earnings potential affects the existing investment narrative.

AI is about to change healthcare. These 36 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Bank of America Investment Narrative Recap

To own Bank of America, you need to believe its scale, diversified banking model, and disciplined balance sheet can support steady earnings and ongoing capital returns despite macro uncertainty and regulatory scrutiny. The recent analyst upgrades reinforce that view, but they do not materially change the near term catalyst around earnings resilience or the key risk that market and economic volatility could pressure credit quality, funding costs, and litigation related expenses.

Among recent developments, the launch of the Royal ONE and Royal ONE Plus co branded credit cards with Royal Caribbean stands out as a practical example of Bank of America leaning into fee based, loyalty driven consumer spending. While small next to its core lending and deposit franchise, partnerships like this tie into the broader catalyst of using digital engagement and product ecosystems to deepen relationships and support future revenue growth.

Yet even with these positives, investors should not overlook how rising litigation costs could weigh on margins and capital flexibility over time...

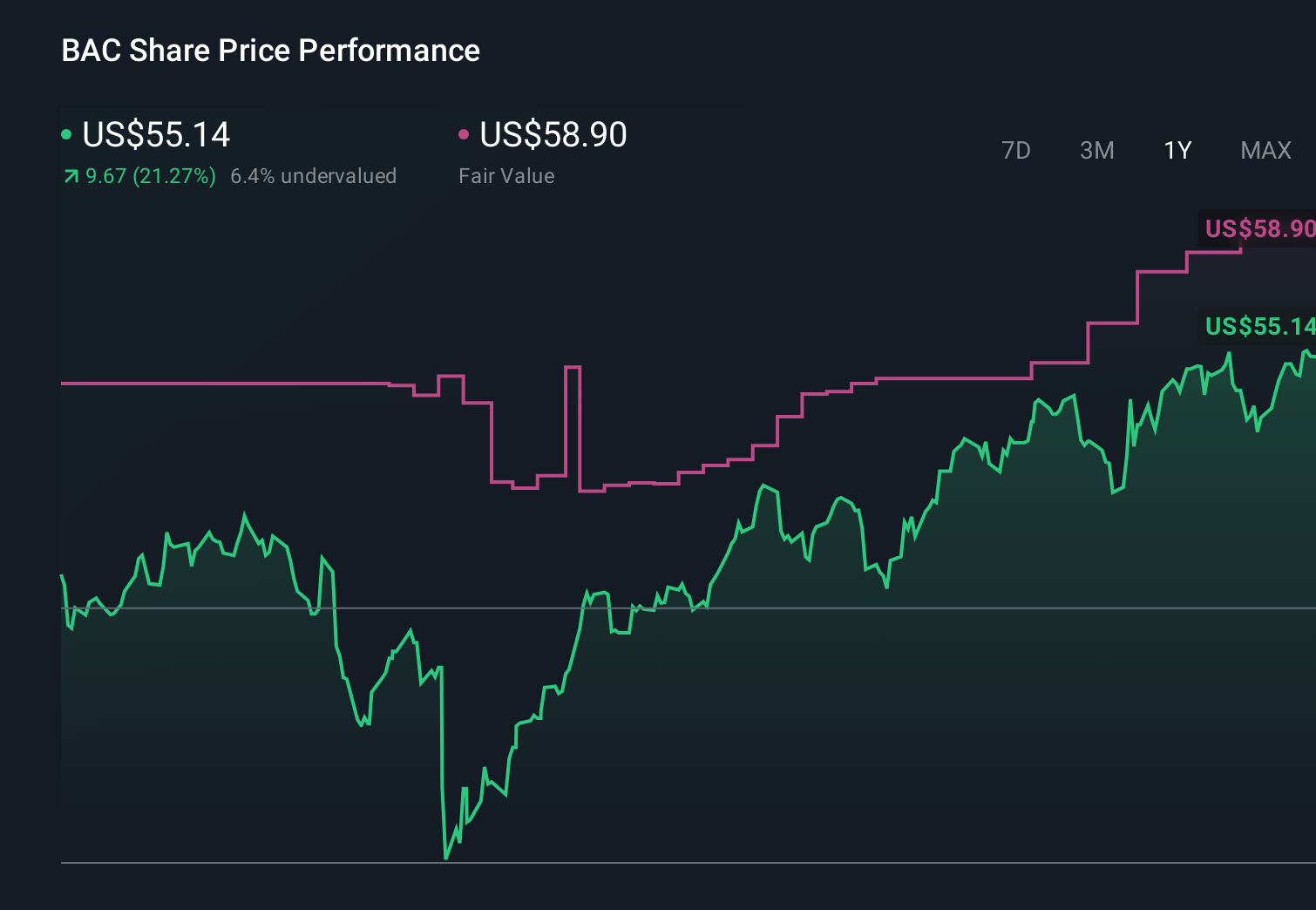

Bank of America's narrative projects $130.6 billion revenue and $36.5 billion earnings by 2029. This requires 6.7% yearly revenue growth and about a $7.4 billion earnings increase from $29.1 billion today.

Uncover how Bank of America's forecasts yield a $61.77 fair value, a 25% upside to its current price.

Exploring Other Perspectives

Thirteen members of the Simply Wall St Community currently see Bank of America’s fair value between US$50.21 and US$80.63, underlining how far opinions can stretch. When you weigh that against the catalyst of ongoing buybacks supported by strong capital levels, it is worth comparing several viewpoints before deciding how this could shape the bank’s future performance.

Explore 13 other fair value estimates on Bank of America - why the stock might be worth just $50.21!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank of America research is our analysis highlighting 5 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bank of America research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank of America's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Uncover the next big thing with 33 elite penny stocks that balance risk and reward.

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- Capitalize on the AI infrastructure supercycle with our selection of the 36 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.