Bank OZK’s Higher Dividend Amid Margin Questions Might Change The Case For Investing In OZK

Bank OZK OZK | 0.00 |

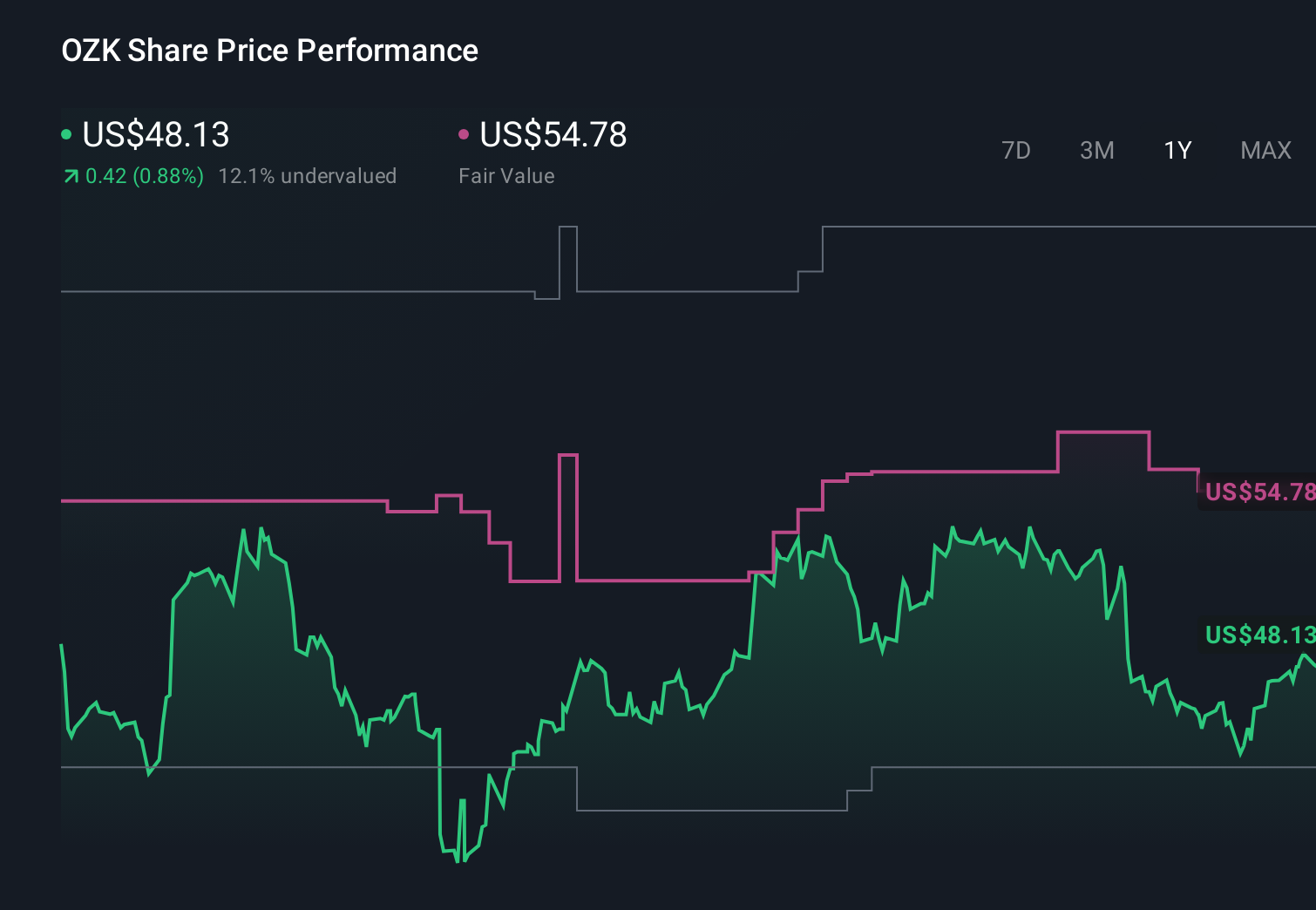

- In the recent past, Bank OZK reported first-quarter results showing higher net interest income but a small decline in earnings per share, while still increasing its common dividend despite persistent questions around margin pressure and credit quality.

- This combination of firmer interest income, softer per-share earnings, and a higher dividend sharpened investor focus on how Bank OZK balances loan growth with potential credit and funding cost risks.

- Next, we’ll examine how Bank OZK’s dividend increase amid margin and credit concerns may influence its existing investment narrative.

Explore 27 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Bank OZK Investment Narrative Recap

To own Bank OZK, you have to be comfortable with a story built around disciplined real estate lending, measured expansion in growth markets, and consistent capital returns. The latest quarter, with higher net interest income but slightly softer EPS, does not appear to fundamentally alter the near term focus on funding costs as the key catalyst and commercial real estate credit as the central risk.

The most relevant recent announcement here is the April 2026 dividend increase to US$0.47 per share, continuing OZK’s long streak of quarterly raises. In the context of firmer net interest income but modest earnings pressure, that higher payout keeps attention on whether the bank’s credit quality and margin performance can support ongoing dividend growth while it leans into its core lending franchises.

Yet beneath the steady dividend increases, investors should be aware of how concentrated commercial real estate exposure could...

Bank OZK’s narrative projects $2.1 billion revenue and $727.8 million earnings by 2029. This requires 9.8% yearly revenue growth and about a $37.1 million earnings increase from $690.7 million today.

Uncover how Bank OZK's forecasts yield a $52.33 fair value, a 8% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were expecting revenue of about US$2.1 billion and earnings near US$796 million, assuming CIB outperformance, which is a much more upbeat view than the baseline. Your take on whether this quarter’s softer EPS and higher net interest income alter that faster growth and margin story will shape how you weigh these competing perspectives.

Explore 3 other fair value estimates on Bank OZK - why the stock might be worth over 2x more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Bank OZK research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Bank OZK research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bank OZK's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Capitalize on the AI infrastructure supercycle with our selection of the 40 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.