Beyond Meat Stock And 2 Protein Plays To Watch After Brazilian Beef Tariff Relief

Hormel Foods Corporation HRL | 0.00 |

Global protein markets are being shaken by the Trump administration’s decision to exempt Brazilian beef from proposed 25% tariffs, and that ripple is reaching well beyond ranches. For investors, this kind of trade shock can quickly reshuffle pricing power, costs and demand across traditional meat producers and consumer protein alternatives. This article breaks down three stocks exposed to the news, highlighting one that could see a potential tailwind from shifting consumer preferences and two that may face headwinds from import pressure and policy uncertainty, so you can decide how or whether they fit into your watchlist.

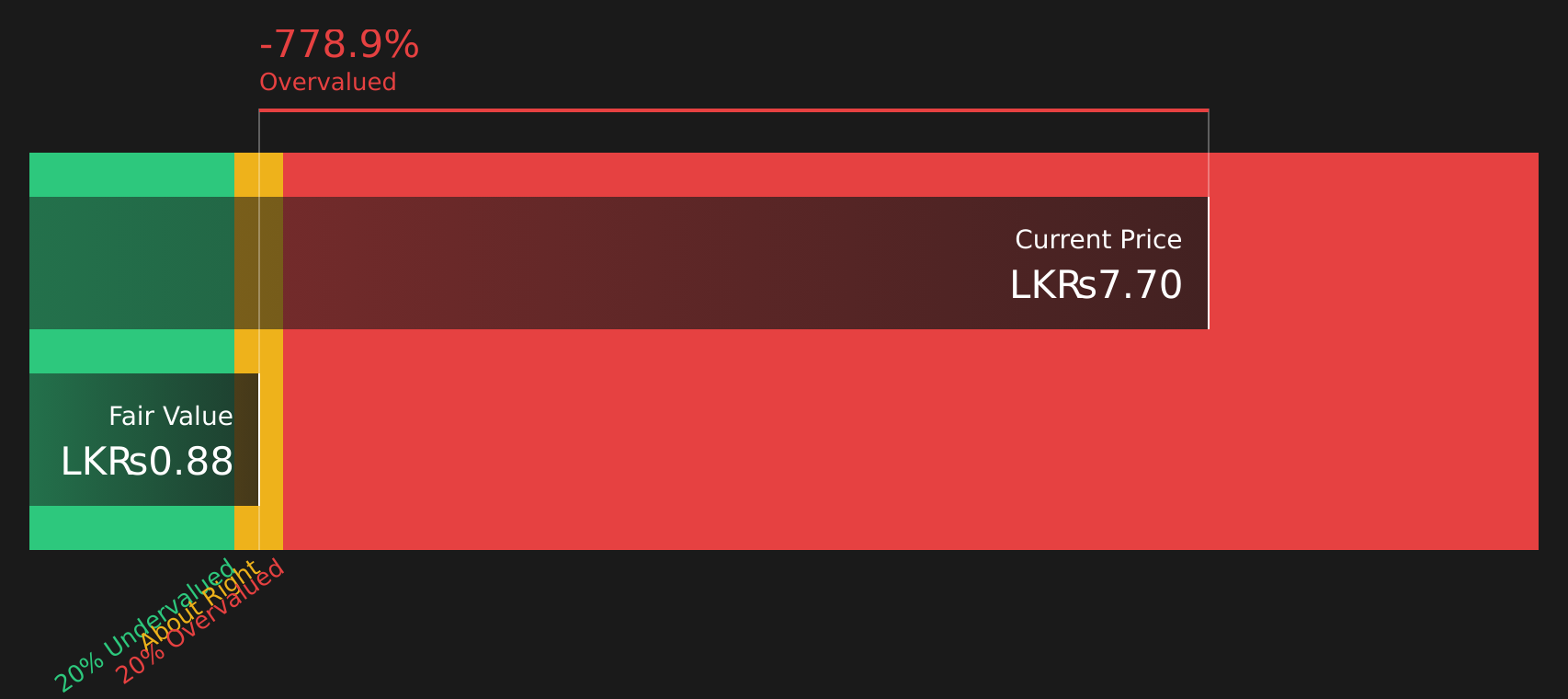

Cargills Bank (COSE:CBNK.N0000)

Overview: Cargills Bank PLC is a Sri Lankan commercial bank that serves individuals, small businesses and larger corporates with everyday accounts, savings products, loans, cards and digital banking, while also offering trade finance, treasury services and agri-business lending.

Operations: Cargills Bank generates virtually all of its LKR 5,202.6 million in revenue in Sri Lanka, primarily from Banking at LKR 4,504.4 million and Treasury/Investments at LKR 693.0 million.

Market Cap: LKR 9.79b

Cargills Bank might catch your eye as a consumer facing lender, but the numbers raise difficult questions. Earnings fell 36.9% over the past year, net profit margin slid from 14.4% to 9.3% and ROE is 3.3%. Together, these figures suggest the bank is finding it difficult to convert its balance sheet into strong returns. Asset quality is another consideration, with bad loans at 7.6% and provisioning just under 100%, which leaves limited room for further stress. In addition, the stock trades on a P/E of 20.2x and above one DCF estimate of intrinsic value. This points to a valuation that appears expensive relative to a bank that has underperformed both the Sri Lankan banking sector and the wider market.

Cargills Bank’s weak earnings, thinner margins and elevated bad loans may indicate deeper balance sheet stress that headline ratios may not fully show. Before assuming this is just a temporary blip, review the Cargills Bank financial health report

Hormel Foods (HRL)

Overview: Hormel Foods is a global packaged food company that produces and sells a wide range of meat, nut and refrigerated and shelf stable products, from SPAM, bacon and deli meats to SKIPPY peanut butter and Planters snacks, across retail, foodservice and international channels.

Operations: Hormel Foods generates about US$7.4b from Retail, US$4.1b from Foodservice and US$0.7b from International operations.

Market Cap: US$13.36b

Hormel Foods might look like a dependable protein and packaged food stock, but the backdrop is tougher than it appears. Earnings have fallen sharply, net margin is just 3.8% and return on equity is low, while a large US$186.9m one off loss and a dividend that is not well covered by earnings raise questions about how resilient the current payout really is. On top of that, Hormel trades on a rich P/E of 29.1x. Revenue growth expectations are only 1.9% a year and earnings growth is described as moderate, which leaves little room for disappointment if cost pressures, weaker demand or intensifying competition from cheaper Brazilian beef keep squeezing margins.

Hormel’s rich 29.1x P/E, thin 3.8% margin and a dividend not well covered by earnings suggest something in the story is stalling. The full risk picture may only be clear in the analysis report for Hormel Foods

Beyond Meat (BYND)

Overview: Beyond Meat is a plant based meat company that develops, produces and sells plant based alternatives that aim to replicate the taste and texture of beef, pork and poultry, supplying supermarkets, club stores and natural food retailers as well as restaurants, foodservice outlets and schools in the U.S. and abroad.

Operations: Beyond Meat generates about US$265.0m in revenue from plant based meat products, split between roughly US$155.8m in the U.S. and US$109.1m from international markets.

Market Cap: US$378.5m

Beyond Meat sits at the center of rising concern over beef imports and deforestation. This could push more flexitarian consumers to consider plant based options just as the company is rolling out cleaner label products like Beyond Steak Filet, Beyond Chicken Pieces, breakfast sausages and its new Beyond Immerse beverage line. At the same time, the business carries heavy debt, recurring losses and a recent equity raise that diluted shareholders. Management is working to cut costs and rebuild retail distribution after volume declines. For investors, the tension between a low P/E multiple, category headwinds and a potential demand boost from beef market disruption makes Beyond Meat a stock that calls for closer scrutiny rather than a quick conclusion.

Beyond Meat’s low P/E and fresh product lineup may reflect a risk-reward profile that differs from what headlines suggest. Get the full story in the 2 key rewards and 6 important warning signs (6 are major!)

Take Control of Your Investment Journey

If Cargills Bank or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before The Crowd Moves?

Fresh stock ideas do not stay under the radar for long. Before the next breakout gains momentum or quality drops from view, scan these curated lists and get in early.

- Spot cash rich businesses that could keep compounding by running the 212 high quality undervalued stocks while it still focuses on companies the crowd has not fully priced in.

- Catch early leaders in automation and factory efficiency by using the 29 robotics and automation stocks before industrial spending momentum pulls more investors into the same small group of stocks.

- Track the companies wiring tomorrow’s electrification by checking the 35 power grid technology and infrastructure stocks while infrastructure momentum is building and valuations still reflect incomplete attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.