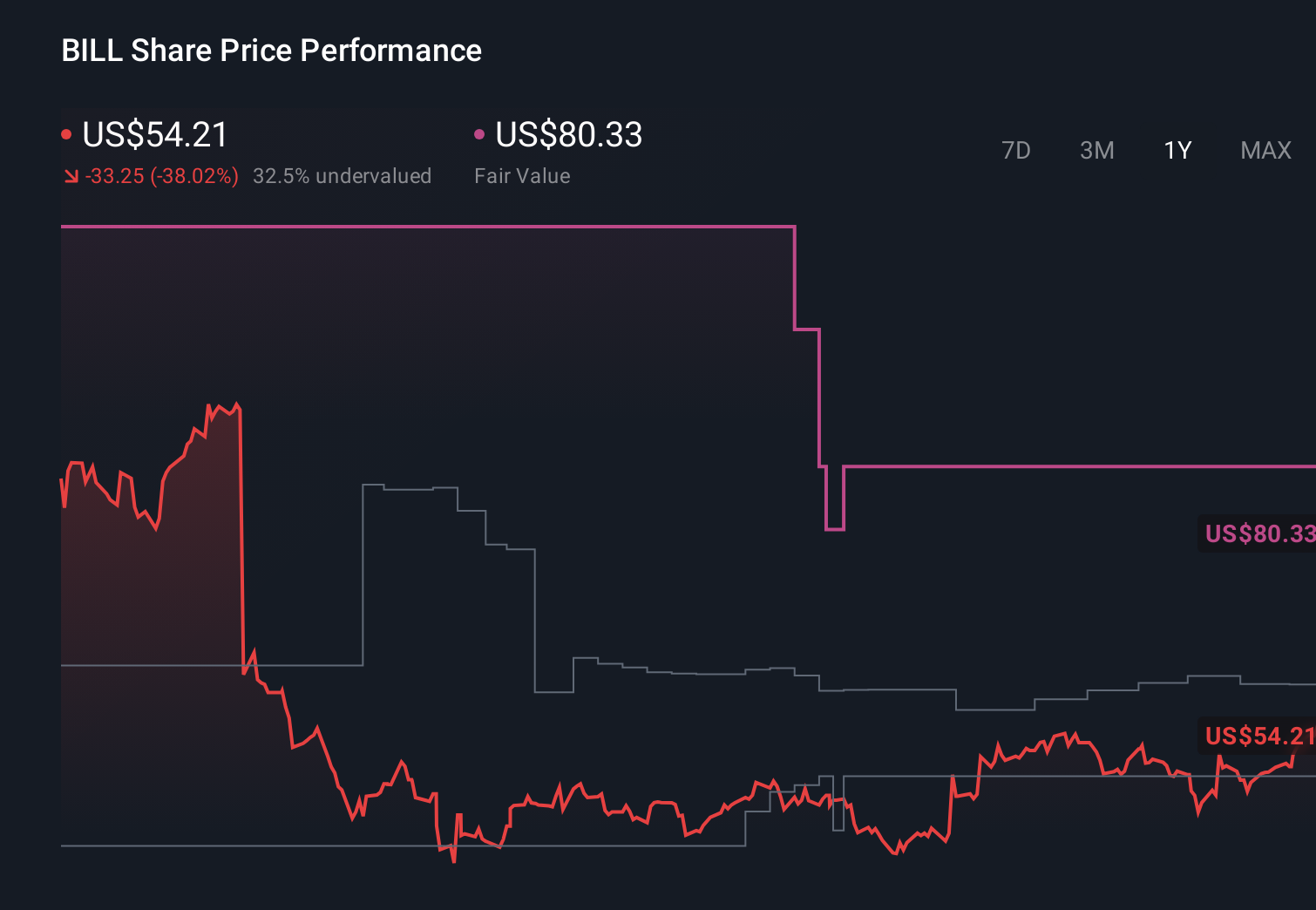

BILL Holdings (BILL) Is Down 7.8% After Analyst Downgrade And Insider Selling Questions Growth Durability

BILL Holdings BILL | 0.00 |

- Earlier this week, Truist Securities downgraded BILL Holdings from Buy to Hold, citing concerns about slowing revenue growth, rising competition, and recent insider share sales totaling US$1.2 million.

- This combination of a more cautious analyst stance and insider selling raises fresh questions about how durable BILL Holdings' growth and competitive position may be.

- Next, we’ll examine how Truist’s downgrade and its concerns about revenue momentum intersect with BILL Holdings’ existing investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 30 best rare earth metal stocks of the very few that mine this essential strategic resource.

BILL Holdings Investment Narrative Recap

To own BILL Holdings, you need to believe its SMB finance platform, AI initiatives, and embedded payments can keep driving healthy transaction growth and monetization. Right now, the key near term catalyst is whether recent product launches and AI features can sustain revenue momentum. Truist’s downgrade, combined with weak technical signals and insider selling, directly challenges that momentum and reinforces the biggest current risk: intensifying competition potentially slowing growth and pressuring margins.

In this context, BILL’s recent US$1.0 billion share repurchase authorization stands out. While it does not directly address Truist’s concerns about revenue growth or competition, it underlines that the company is committing significant capital to its own shares even as external signals turn more cautious. For investors, this sits alongside product launches like Supplier Payments Plus and Bill Travel as they weigh whether near term sentiment headwinds could affect the timing and strength of these growth drivers.

Yet against all of this, the competitive risk around pricing power and customer churn is something investors should be aware of, because...

BILL Holdings' narrative projects $2.6 billion revenue and $316.6 million earnings by 2029.

Uncover how BILL Holdings' forecasts yield a $54.62 fair value, a 65% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts offer a much more cautious view, assuming only about US$2.2 billion of revenue and roughly US$29 million of earnings by 2029, so Truist’s downgrade and recent AI driven short signals could push those already pessimistic expectations even lower and it is worth considering how your own outlook compares.

Explore 4 other fair value estimates on BILL Holdings - why the stock might be worth just $42.00!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your BILL Holdings research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free BILL Holdings research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate BILL Holdings' overall financial health at a glance.

Searching For A Fresh Perspective?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- Uncover the next big thing with 24 elite penny stocks that balance risk and reward.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.