Blue Creek Completion and Supply Constraints Could Be A Game Changer For Warrior Met Coal (HCC)

Warrior Met Coal, Inc. HCC | 0.00 |

- In the second quarter of 2026, Black Bear Value Partners discussed Warrior Met Coal after the company completed its Blue Creek development project, which positions it as one of the lowest-cost metallurgical coal producers globally.

- The investor letter also underscored how limited global investment in new metallurgical coal capacity could tighten future supply, potentially enhancing Warrior Met Coal’s competitive position as steel demand evolves.

- We’ll now examine how the completion of Blue Creek and these emerging supply constraints may reshape Warrior Met Coal’s broader investment narrative.

AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Warrior Met Coal Investment Narrative Recap

To own Warrior Met Coal, you need to believe that premium metallurgical coal will remain essential for steel, and that Blue Creek’s low-cost tons can offset pricing and demand pressure. The key short term catalyst is Blue Creek’s successful ramp from development into cash-generating production, which this completion milestone directly supports. The biggest current risk is that global steel demand and coal prices stay weak, limiting the benefit of new capacity despite Warrior’s lower cost position.

Among recent announcements, the Q1 2026 results are particularly relevant. Revenue rose to US$458.59 million with net income of US$72.34 million, reflecting Warrior’s pivot from heavy Blue Creek spending toward higher production and earnings. Combined with the Blue Creek completion, this moves the story from “can they build it on time and budget?” to “can they sell higher volumes at attractive prices in a volatile export market?”

Yet, even with Blue Creek online, investors should be aware of how prolonged steel weakness and tariff risks could...

Warrior Met Coal's narrative projects $2.5 billion revenue and $543.8 million earnings by 2029. This requires 19.5% yearly revenue growth and a $406.3 million earnings increase from $137.5 million today.

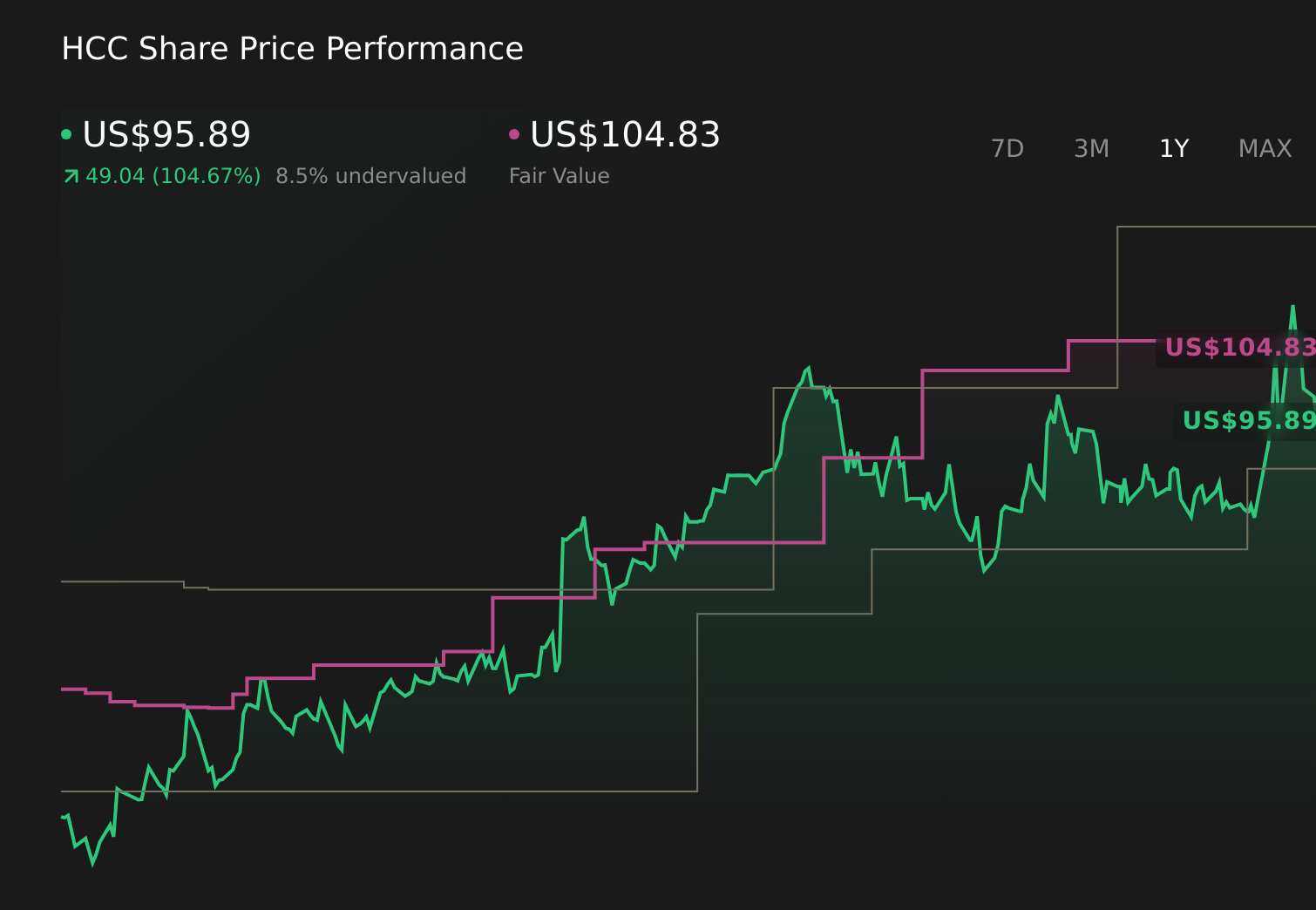

Uncover how Warrior Met Coal's forecasts yield a $104.83 fair value, a 31% upside to its current price.

Exploring Other Perspectives

The most optimistic analysts already expected revenue near US$2.7 billion and earnings above US$820 million, so if Blue Creek shifts market share or pricing, those views on decarbonization risk could change sharply.

Explore 3 other fair value estimates on Warrior Met Coal - why the stock might be worth over 2x more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Warrior Met Coal research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Warrior Met Coal research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Warrior Met Coal's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.