Calumet (CLMT) Valuation Check As MaxSAF 150 Expansion And EPA Tailwinds Draw Investor Focus

Calumet, Inc. CLMT | 0.00 |

Calumet (CLMT) has drawn fresh attention after completing the MaxSAF 150 expansion at its Montana Renewables segment, securing premium sustainable aviation fuel contracts and gaining from recent EPA clarity, despite disruption at its Shreveport facility.

The recent MaxSAF 150 ramp up, premium sustainable aviation fuel contracts and a series of investor conferences have coincided with firm share price momentum, with a 90 day share price return of 23.16% and a very large 5 year total shareholder return of 495.87%.

If this kind of momentum in renewables has your attention, it could be a good moment to scan for other potential opportunities with our 33 power grid technology and infrastructure stocks

With Calumet shares up strongly over the past year and trading only slightly below the average analyst price target of US$37, the key question is simple: is there still mispricing here, or is future growth already reflected in the price?

Most Popular Narrative: 54% Overvalued

Calumet's most followed valuation narrative pegs fair value at $23.45 per share, well below the last close of $36.11, which sets up a cautious stance on the current price.

Fair Value has moved from $22.65 to $23.45, indicating a modest upward adjustment in the estimated equity value per share. Discount Rate has shifted from 7.90% to about 7.62%, a small reduction in the rate used to discount future cash flows.

Want to see what justifies a fair value well under the current share price? The narrative leans heavily on specific revenue growth, margin improvement and future earnings assumptions, all filtered through that discount rate and a richer future earnings multiple.

Result: Fair Value of $23.45 (OVERVALUED)

However, this depends on supportive regulation and effective management of a sizeable debt load, and setbacks on either front could quickly challenge the current overvaluation story.

Another Angle on Value

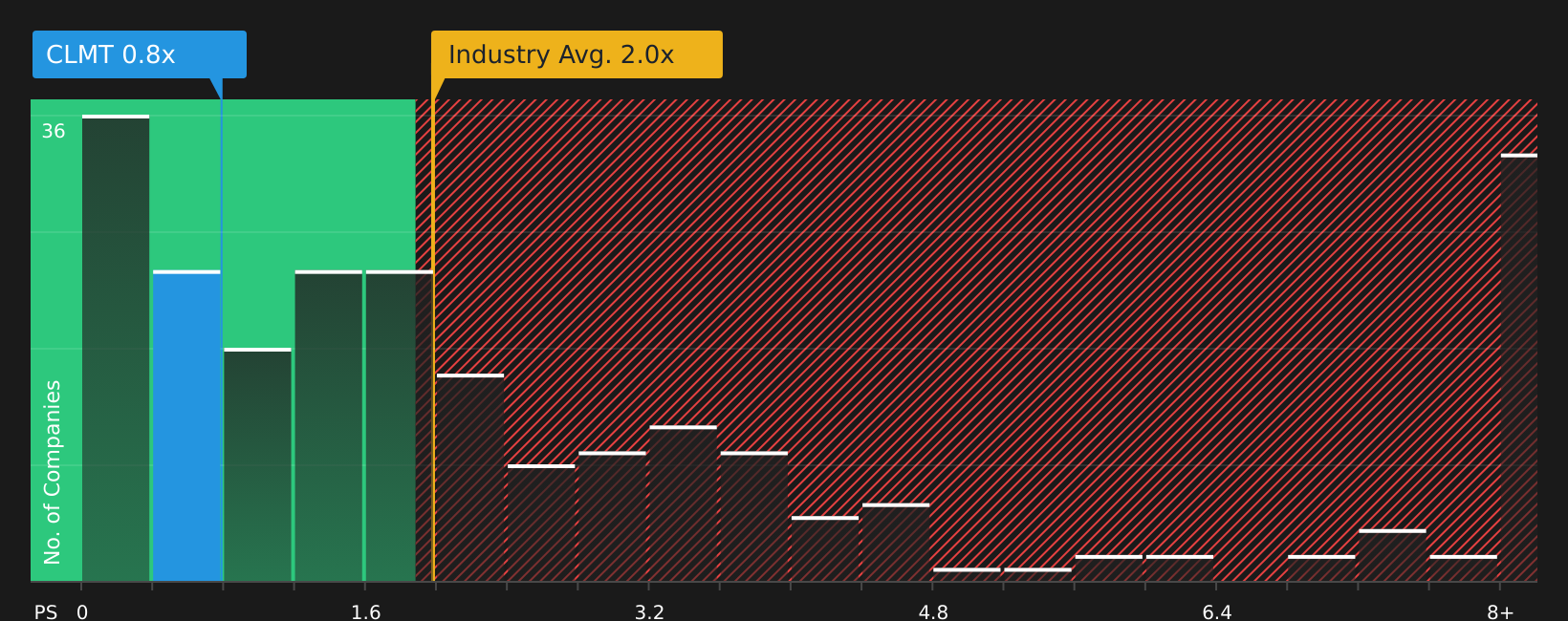

The fair value narrative presents Calumet as 54% overvalued at $23.45 versus a $36.11 share price, yet the revenue multiple tells a different story. Calumet trades at a P/S of 0.8x, lower than the broader US Oil and Gas industry at 2x, but higher than its peer average of 0.2x and above an estimated fair ratio of 0.6x. That combination suggests both a relative discount to the sector and a premium to closer comparables, so which side of that gap appears more persuasive to you?

Next Steps

With mixed signals on valuation, sentiment and fundamentals, this is the kind of setup where you benefit from seeing the detail for yourself and acting while the data is fresh. Start with the 1 key reward and 2 important warning signs.

Looking for more investment ideas?

If you are serious about improving your portfolio, do not stop at a single stock; use focused stock lists to spot opportunities others overlook.

- Target potential upside by scanning 46 high quality undervalued stocks that combine appealing prices with solid underlying businesses.

- Strengthen your income stream by reviewing 11 dividend fortresses offering higher yields that may suit a long term cash flow focus.

- Reduce potential portfolio stress by checking 63 resilient stocks with low risk scores that score well on resilience and stability factors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.