Camtek (CAMT) Is Up 10.6% After Issuing Bold Second-Half 2026 Revenue Guidance - Has The Bull Case Changed?

Camtek Ltd CAMT | 0.00 |

- In May 2026, Camtek Ltd. reported first-quarter 2026 results showing sales of US$121.66 million versus US$118.64 million a year earlier, while net income eased to US$31.65 million from US$34.31 million.

- The company coupled this mixed earnings picture with ambitious guidance, forecasting second-quarter revenues of US$129–US$131 million and expecting second-half 2026 revenues to be more than 25% higher than the first half.

- Next, we'll examine how Camtek's expectation of a significant second-half 2026 revenue increase affects its existing investment narrative and risk balance.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Camtek Investment Narrative Recap

To own Camtek, you need to believe in a long-term buildout of inspection and metrology for AI and high-performance computing packaging, especially at OSATs. The latest results showed modest sales growth but softer earnings, while management’s guidance for a more than 25% revenue lift in the second half of 2026 keeps the near term growth catalyst intact. The biggest near term risk around customer concentration and semiconductor spending cycles does not appear materially changed by this update.

The most relevant recent announcement here is Camtek’s May 2026 guidance that second quarter revenue should reach US$129–US$131 million and that second half 2026 revenue will be over 25% higher than the first half. This outlook sits on top of sizeable recent AI related orders from OSATs and an IDM, and it directly ties into the key catalyst of increased demand for advanced packaging inspection tied to AI and high performance computing workloads.

Yet investors should also be aware of how heavily this outlook leans on AI driven advanced packaging demand and a concentrated customer base in Asia, because...

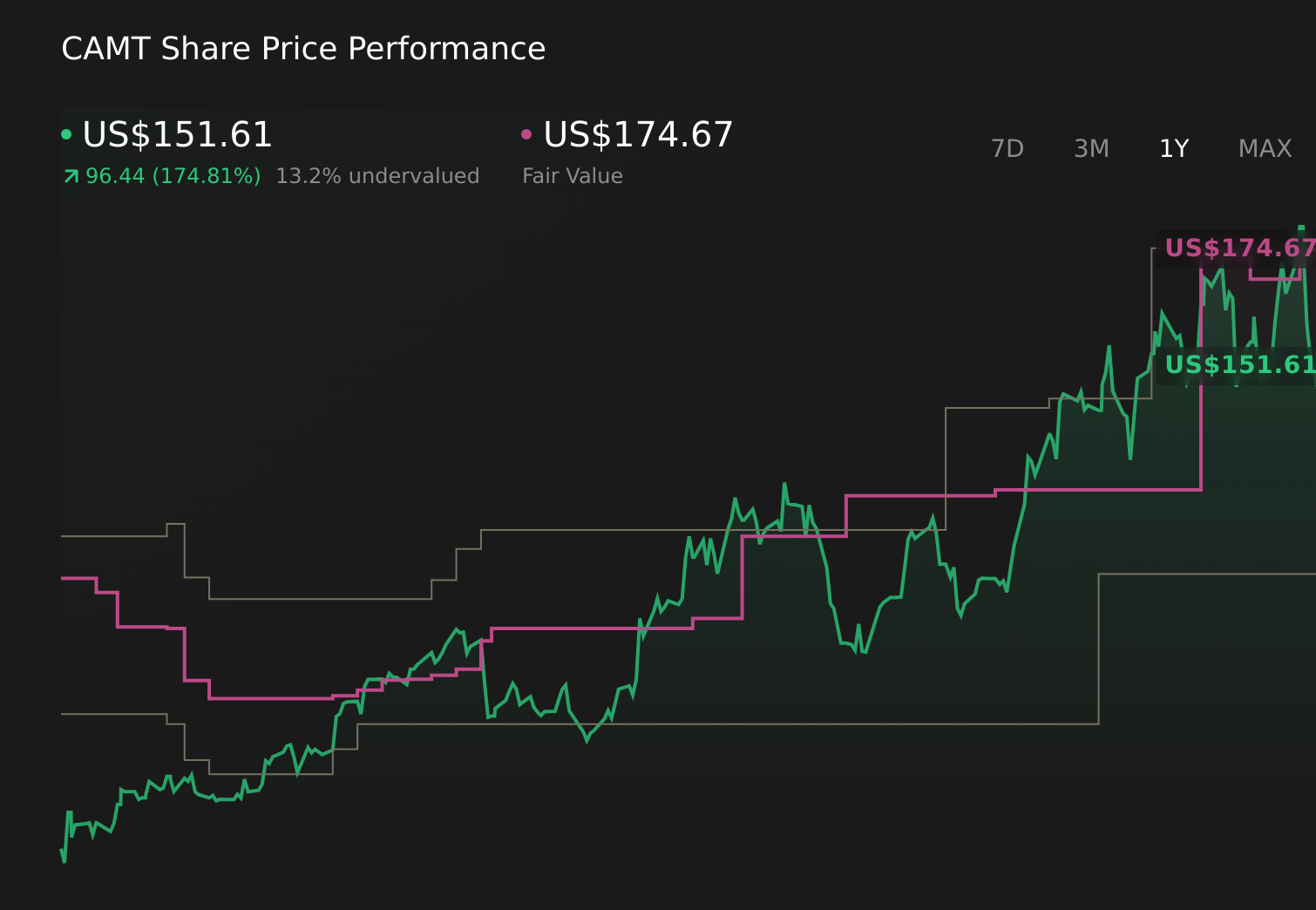

Camtek's narrative projects $786.7 million revenue and $314.9 million earnings by 2029.

Uncover how Camtek's forecasts yield a $174.67 fair value, a 4% upside to its current price.

Exploring Other Perspectives

Some of the lowest analysts were already cautious, assuming revenue of about US$714.4 million and earnings of roughly US$347.8 million by 2029, so you may find their more pessimistic take on HPC dependence and China exposure particularly important to reconsider in light of Camtek’s new H2 2026 guidance.

Explore 3 other fair value estimates on Camtek - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Camtek research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Camtek research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Camtek's overall financial health at a glance.

Looking For Alternative Opportunities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 27 companies in the world exploring or producing it. Find the list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 15 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.