Camtek (CAMT) Is Up 7.2% After $31M AI OSAT Order Boosts Advanced Packaging Narrative

Camtek Ltd CAMT | 173.09 | -0.82% |

- In late March 2026, Camtek Ltd. announced a multi-system order worth US$31,000,000 from an outsourced semiconductor assembly and test (OSAT) customer for CoWoS-like packaging tools supporting AI applications, contributing to more than US$90,000,000 in OSAT orders booked in the first quarter.

- This concentration of AI-focused advanced packaging demand from OSATs highlights how central Camtek’s inspection and metrology systems have become in high-performance semiconductor manufacturing workflows.

- We’ll now examine how this large AI-oriented OSAT order shapes Camtek’s investment narrative, particularly its advanced packaging growth thesis.

We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Camtek Investment Narrative Recap

To own Camtek, you have to believe its tools will remain essential in advanced packaging for AI and high‑performance computing, and that it can defend margins against larger rivals. The US$31,000,000 AI‑oriented OSAT order strengthens the near‑term growth catalyst of advanced packaging demand, but it also deepens exposure to cyclical OSAT capex and a concentrated HPC customer base, which remains the key risk.

The February 2026 guidance calling for around US$120,000,000 in Q1 revenue and double‑digit growth for 2026 provides useful context for this new US$90,000,000‑plus OSAT order flow, suggesting that AI‑linked packaging demand was already baked into expectations. The earlier US$25,000,000 Hawk order from a tier‑1 IDM for AI applications ties this together, underscoring how much of Camtek’s current narrative leans on AI‑driven advanced packaging uptake.

Yet behind this strong AI story, investors should still be aware of how exposed Camtek is if HPC demand or OSAT spending were to...

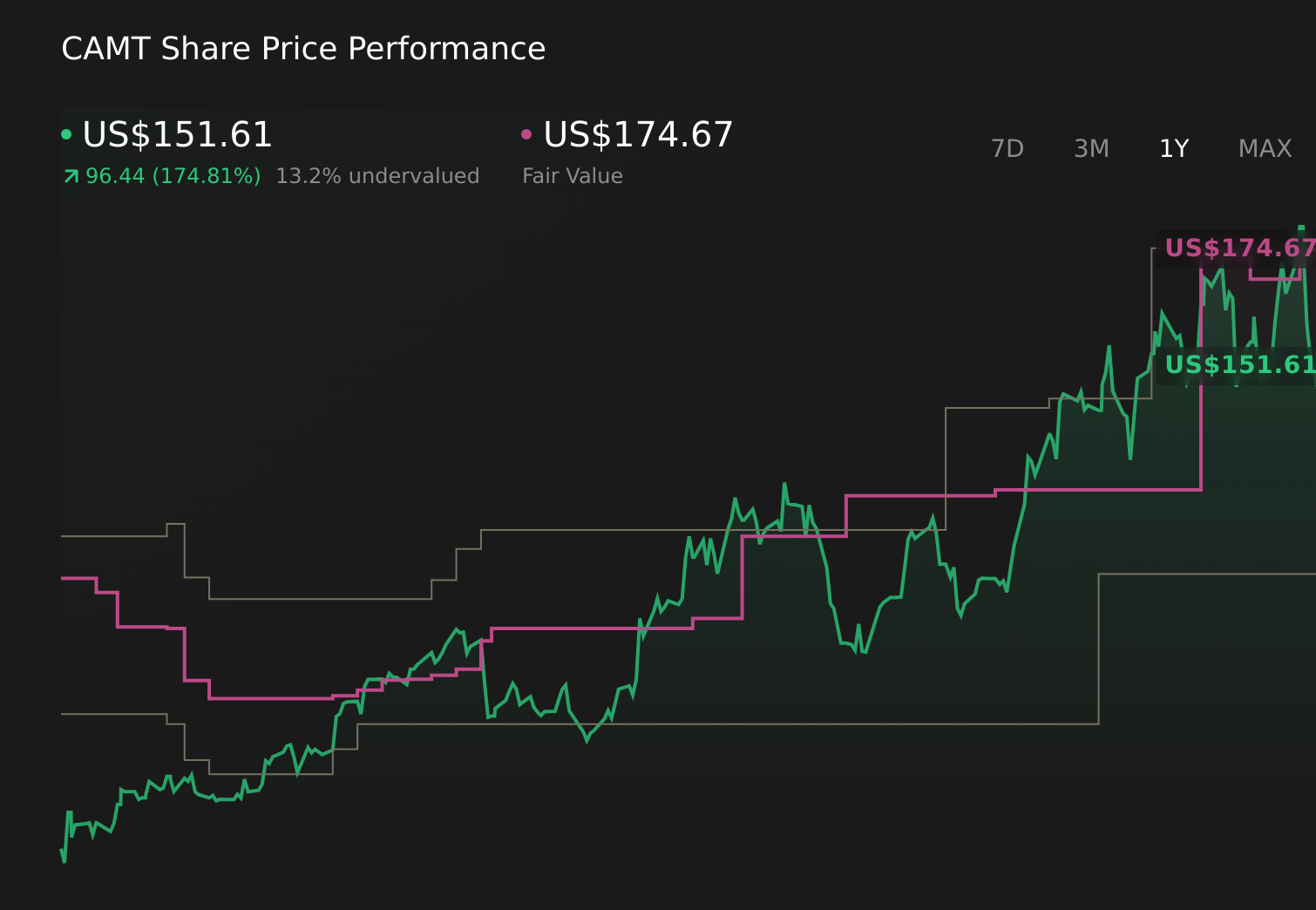

Camtek's narrative projects $786.7 million revenue and $314.9 million earnings by 2029. This requires 16.6% yearly revenue growth and about a $264.2 million earnings increase from $50.7 million today.

Uncover how Camtek's forecasts yield a $174.67 fair value, a 3% upside to its current price.

Exploring Other Perspectives

Before this news, the most bullish analysts were already assuming Camtek could reach about US$906,700,000 in revenue and US$342,400,000 in earnings by 2029, which is a far more optimistic path than the baseline view and relies heavily on ongoing AI packaging strength and resilience to advanced packaging slowdowns, so it is worth comparing how your own expectations stack up against both narratives.

Explore 3 other fair value estimates on Camtek - why the stock might be worth less than half the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Camtek research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

- Our free Camtek research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Camtek's overall financial health at a glance.

Interested In Other Possibilities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 23 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Find 64 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.