Can American Electric Power Company (AEP) Justify Its Valuation After Q1 Earnings And Dividend Lift?

American Electric Power Company, Inc. AEP | 0.00 |

American Electric Power Company (AEP) recently reported Q1 2026 operating earnings of $1.64 per share, alongside a higher quarterly dividend of $0.95, while reaffirming full-year guidance.

At a share price of $134.94, American Electric Power Company has seen its 30 day share price return rise 4.42% and its year to date share price return reach 16.52%, while the 1 year total shareholder return stands at 33.35%. This suggests recent momentum building on a longer period of compounding returns.

If AEP's earnings and dividend story has your attention, this is also a useful moment to look across the grid and check out 34 power grid technology and infrastructure stocks

American Electric Power Company’s share price is now relatively close to the average analyst target yet sits at a discount to some intrinsic value estimates, so where might fair value really lie after this latest move?

Most Popular Narrative: 19.4% Overvalued

According to the most followed narrative, American Electric Power Company’s fair value of $113 sits below the recent close at $134.94, framing AEP as priced above this narrative’s estimate of intrinsic worth.

The most compelling driver is the unprecedented surge in data center load commitments. AEP’s incremental load pipeline has skyrocketed to 56 GW, a staggering 100% increase from just six months ago. This visibility into the next decade of demand allows AEP to expand its $72B+ capital plan with greater confidence, turning "projected growth" into a clearer path toward rate-base expansion.

Want to see what kind of revenue lift and earnings profile that 56 GW pipeline is designed to support? The narrative connects that capital plan, profitability assumptions and valuation into a tight, numbers-driven case that investors are using as a benchmark.

Result: Fair Value of $113 (OVERVALUED)

However, American Electric Power Company’s growth-heavy narrative faces real pressure if data center demand commitments slow or if regulators push back on the scale and timing of grid investments.

Another View on American Electric Power Company’s Valuation

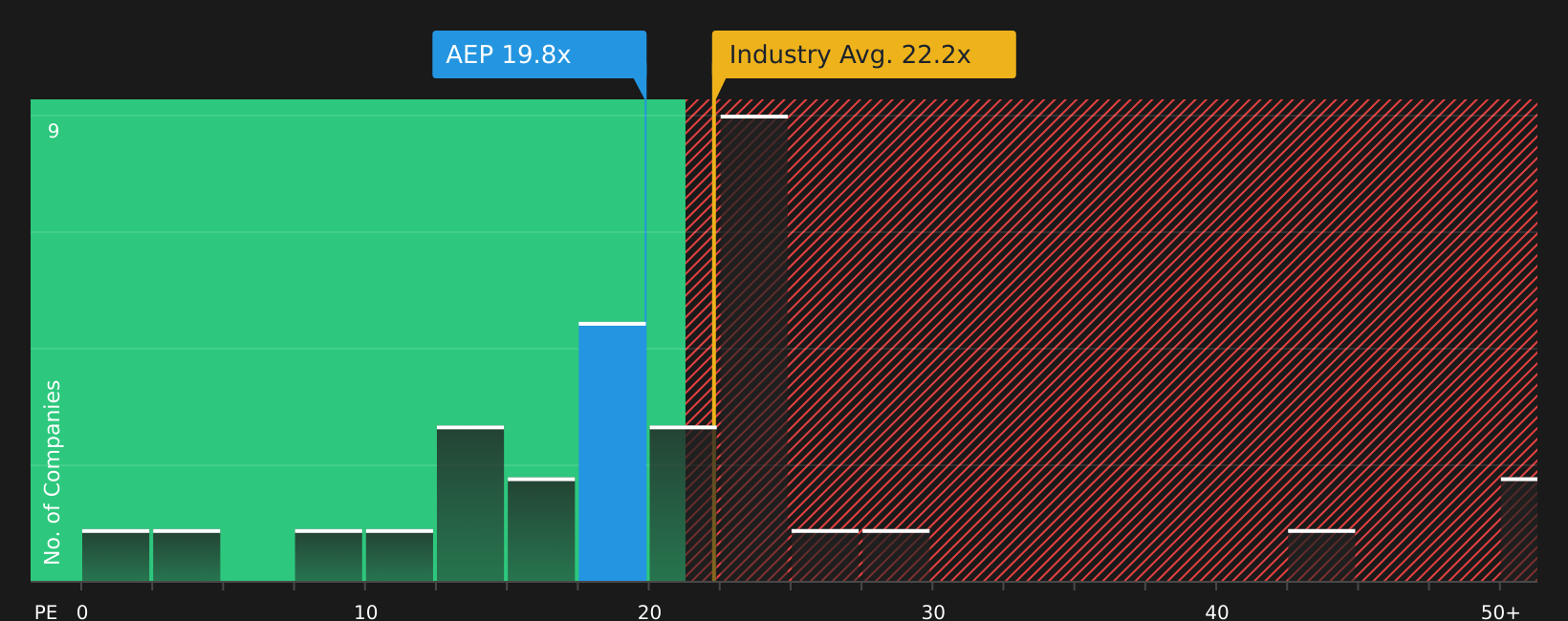

The user narrative leans on a fair value of $113, yet the current P/E of 20.1x tells a different story. American Electric Power Company trades below the US Electric Utilities industry at 22.5x and below peers at 24.5x, while the fair ratio is 24.1x. This points to a valuation gap some investors might see as a cushion rather than a warning sign, so which signal do you trust more right now?

Next Steps

With sentiment split between overvaluation worries and a supportive P/E backdrop, this is a useful moment to move quickly and test the data yourself against 4 key rewards and 2 important warning signs

Looking for more American Electric Power Company investment ideas?

Before you move on, you can line up a few more high quality ideas alongside American Electric Power Company using the Simply Wall Street Screener.

- Target steadier potential returns by reviewing companies screened as 79 resilient stocks with low risk scores that may better match your comfort with volatility.

- Hunt for stronger balance sheets by checking the solid balance sheet and fundamentals stocks screener (48 results) and compare how these stocks handle debt and liquidity.

- Spot potential bargains early by scanning the screener containing 20 high quality undiscovered gems before the crowd starts paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.