Can Bilibili’s (BILI) Investment in User Growth Justify Ongoing Margin Pressures?

BILIBILI INC. BILI | 22.56 23.27 | +4.01% +3.15% Pre |

- In the past week, Bilibili Inc. reported solid revenue growth but highlighted increased operating expenses and shrinking profit margins that have drawn investor attention. These developments underscore a broader pattern among Asian digital commerce firms, where cost-heavy expansion is resulting in near-term margin pressures despite robust user engagement.

- This event spotlights the tension between Bilibili's continued investment in growth initiatives and the near-term strain on profitability that investors are weighing.

- We'll explore how the spotlight on rising costs and tighter margins impacts Bilibili’s long-term investment narrative.

AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Bilibili Investment Narrative Recap

To own Bilibili shares, an investor must trust in the long-term potential of China’s youth-focused digital entertainment market and the company’s ability to translate record user engagement into profitable growth. This week’s drop in share price, following news of rising costs and margin pressure, does not materially alter the fact that near-term profitability remains the most important catalyst, while persistent escalation in content spending is the current top risk for Bilibili’s business model. The immediate focus for the market is whether operational efficiency and margin recovery, potentially aided by AI-driven advertising, can keep pace with these expense trends.

Among recent developments, Bilibili’s Q2 2025 earnings report was especially relevant: the company posted meaningful year-over-year revenue growth and its first semiannual net profit, highlighting a significant step towards profitability. This financial progress underscores what is at stake as investors balance enthusiasm for user metrics with mounting concerns over the sustainability of profit margins.

But in contrast, investors should be aware that ongoing increases in content and creator-related costs may continue to strain margin recovery and ...

Bilibili's outlook forecasts CN¥38.4 billion in revenue and CN¥3.4 billion in earnings by 2028. Achieving this would require 9.3% annual revenue growth and an earnings increase of about CN¥3.18 billion from the current CN¥220.3 million.

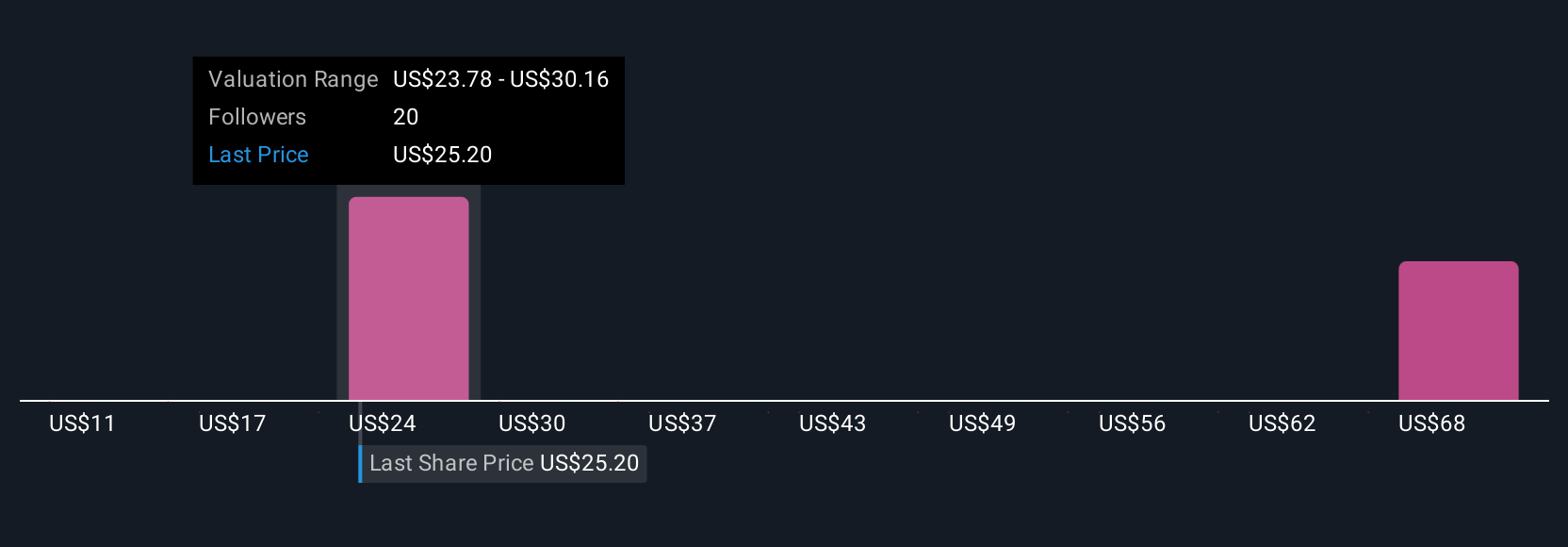

Uncover how Bilibili's forecasts yield a $28.51 fair value, a 6% downside to its current price.

Exploring Other Perspectives

Fair value estimates from six Simply Wall St Community members span CNY 22.18 to CNY 35.09 per share. Against this diversity of views, the continued climb in operating expenses remains a central concern shaping expectations for future earnings growth.

Explore 6 other fair value estimates on Bilibili - why the stock might be worth 27% less than the current price!

Build Your Own Bilibili Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Bilibili research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Bilibili research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Bilibili's overall financial health at a glance.

Searching For A Fresh Perspective?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- Outshine the giants: these 27 early-stage AI stocks could fund your retirement.

- This technology could replace computers: discover 28 stocks that are working to make quantum computing a reality.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.