Can Cimpress (CMPR) Turn Strong Free Cash Flow Into Sustainable Long-Term Growth?

Cimpress Plc CMPR | 0.00 |

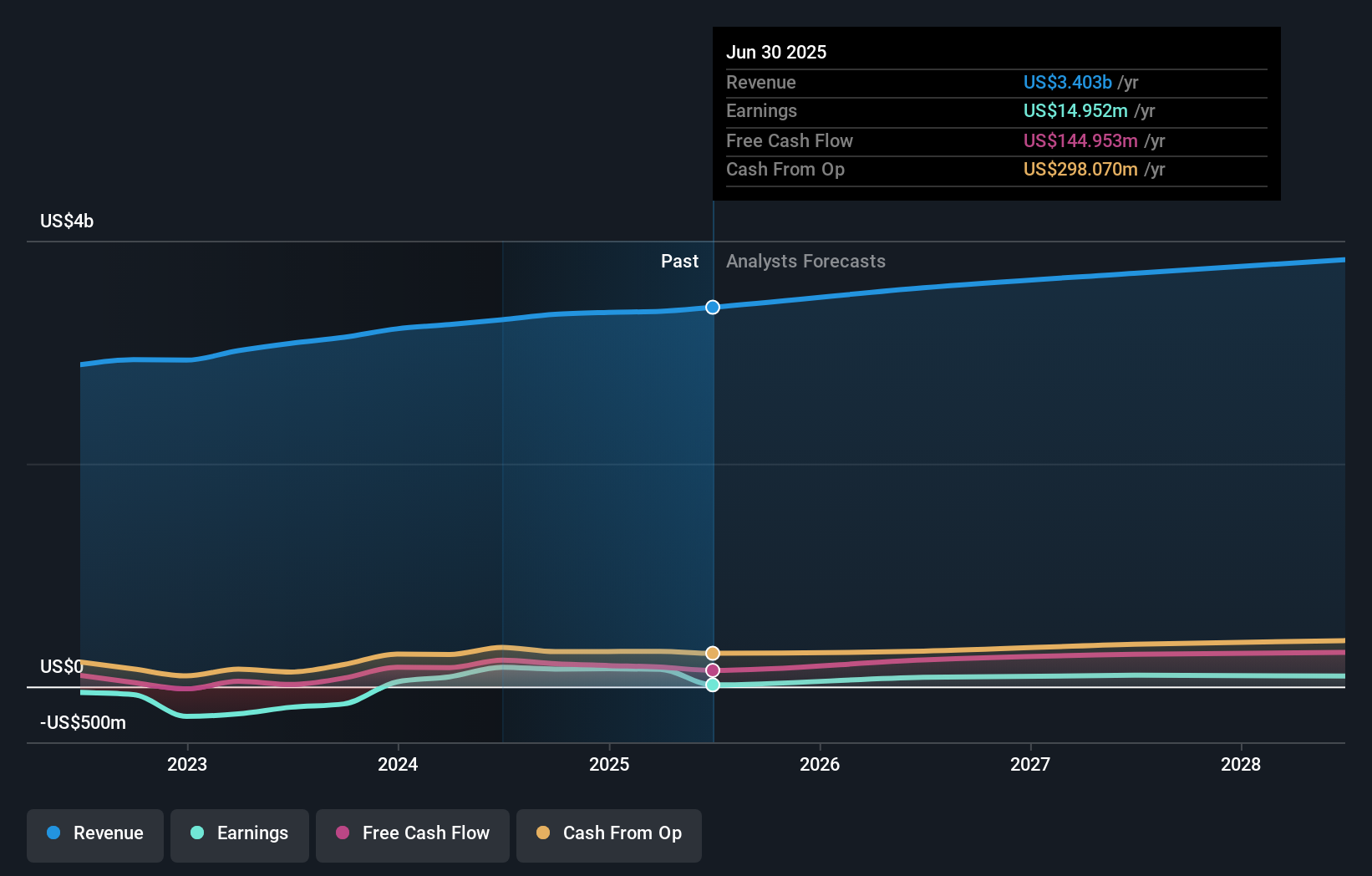

- Last week, Cimpress plc released a softer-than-expected earnings report, but its accrual ratio of 0.16 revealed strong free cash flow despite the decline from the prior year.

- This gap between statutory profit and implied earnings strength has sparked investor interest, even as future profitability concerns remain due to reduced free cash flow.

- We'll explore how Cimpress's robust free cash flow, despite softer earnings, could impact its investment narrative and future outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Cimpress Investment Narrative Recap

To be a Cimpress shareholder right now, you need to believe that the company’s strategy to shift from legacy print products to higher-value segments can offset current profit pressures and sluggish legacy demand. Cimpress’s recent softer earnings and reduced free cash flow draw attention to liquidity and profitability concerns, but the strong accrual ratio and resilient share price suggest the latest news doesn’t fundamentally shift the most important short-term catalyst, sustaining and growing free cash flow, nor does it intensify the biggest risk of high capital spending impacting returns any further than already flagged. Among recent company developments, the fiscal 2026 guidance stood out: Cimpress projected revenue growing 5 to 6 percent with at least US$72 million in net income. This announcement directly frames both the catalyst and risk highlighted by the earnings report, as the credibility of these targets will be tested by the ongoing need for substantial investment to support growth, while free cash flow remains a key metric to monitor. Yet investors should keep in mind, amid optimism about the transition to higher-value products, the continued risk that new segments may not grow fast or profitably enough to counteract losses in legacy categories...

Cimpress' narrative projects $3.8 billion revenue and $94.7 million earnings by 2028. This requires 4.0% yearly revenue growth and an increase of about $79.7 million in earnings from the current $15.0 million.

Uncover how Cimpress' forecasts yield a $72.00 fair value, a 15% upside to its current price.

Exploring Other Perspectives

Three Community estimates of Cimpress’s fair value range widely, from US$72 to US$3,107.51, showing extreme differences in expectations. The company’s gradual revenue expansion but falling margins highlight why opinions differ and why you should compare several viewpoints when forming your own perspective.

Explore 3 other fair value estimates on Cimpress - why the stock might be worth just $72.00!

Build Your Own Cimpress Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cimpress research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Cimpress research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cimpress' overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 21 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 20 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.