Can Inspire Medical Systems (INSP) Convert Revenue Beats Into Sustainable Earnings Strength?

Inspire Medical Systems, Inc. INSP | 0.00 |

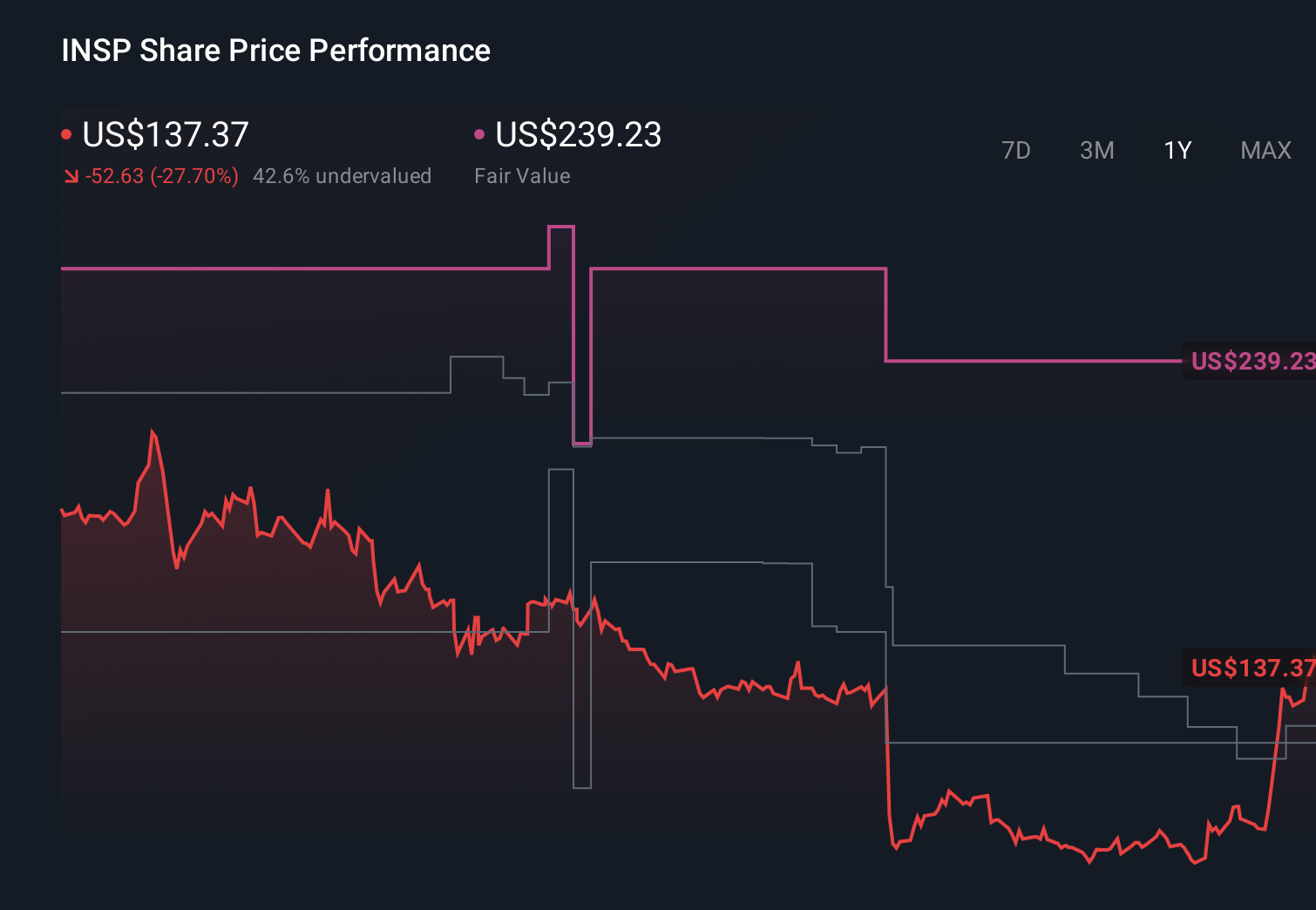

- Inspire Medical Systems recently reported quarterly results showing revenue up 1.6% year on year and ahead of analyst expectations, while missing full-year EPS guidance estimates.

- This mix of stronger-than-expected sales, weaker earnings outlook, and management’s emphasis on improved adjusted operating income and cash flow creates a more nuanced picture of the company’s progress.

- Next, we’ll examine how beating revenue expectations but missing full-year EPS guidance could shape Inspire Medical Systems’ broader investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Inspire Medical Systems Investment Narrative Recap

To own Inspire Medical Systems, you need to believe its implantable sleep apnea therapy can defend and grow its niche despite slower growth and reimbursement pressures. The latest quarter, with slightly higher revenue but weaker EPS guidance, reinforces that the near term catalyst is execution on Inspire V adoption and reimbursement clarity, while the biggest risk remains that higher costs and coding changes keep squeezing profitability. This news does not fundamentally change those short term priorities.

One recent development that ties directly into this is the sharp reset in 2026 revenue and EPS guidance to US$825 million to US$875 million and US$0.07 to US$0.62 per share, down from February’s higher outlook. That shift, coming alongside modest Q1 revenue growth, underlines how reimbursement and cost inflation can quickly pressure earnings, even when procedure volumes are holding up, and keeps the focus squarely on whether Inspire can restore operating leverage as Inspire V rollout issues are addressed.

Yet, in contrast, investors should be aware that reimbursement and coding changes could still pressure margins if volume growth or cost control falls short of expectations...

Inspire Medical Systems' narrative projects $1.1 billion revenue and $97.5 million earnings by 2029.

Uncover how Inspire Medical Systems' forecasts yield a $79.42 fair value, a 92% upside to its current price.

Exploring Other Perspectives

Before this reset, the most optimistic analysts were modeling roughly 16.8 percent annual revenue growth and about US$157.1 million of earnings by 2028, so the latest softer EPS outlook and ongoing reimbursement uncertainty could prompt them to revisit those assumptions, while you weigh how much faith to place in faster adoption and expanding clinical evidence versus the real risk that reimbursement and cost trends prove tougher than expected.

Explore 9 other fair value estimates on Inspire Medical Systems - why the stock might be worth just $45.00!

Form Your Own Verdict

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Inspire Medical Systems research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Inspire Medical Systems research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Inspire Medical Systems' overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find 46 companies with promising cash flow potential yet trading below their fair value.

- Explore 29 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Outshine the giants: these 12 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.