Can Kontoor Brands (KTB) Still Justify A Discount To Fair Value?

Kontoor Brands, Inc. KTB | 0.00 |

Kontoor Brands has delivered a strong 129.4% share price gain over the past three years, yet its valuation checks and intrinsic value estimate still point to the stock trading at a discount to what the underlying cash flows suggest.

- Over the last three years, Kontoor Brands has returned 129.4%. This puts recent short term volatility into context and makes today’s valuation level especially important to assess.

- Recent revenue growth helped reset expectations for the business. The risk is that any stumble in execution or margins could challenge how much investors are willing to pay for those cash flows.

- On Simply Wall St’s broader valuation checks, Kontoor Brands screens as undervalued in 5 of 6 areas, and the Discounted Cash Flow (DCF) intrinsic value estimate suggests the shares trade at about a 24.5% discount to that assessment.

The issue now is whether that apparent discount still offers a comfortable margin of safety after the stock’s multi year run.

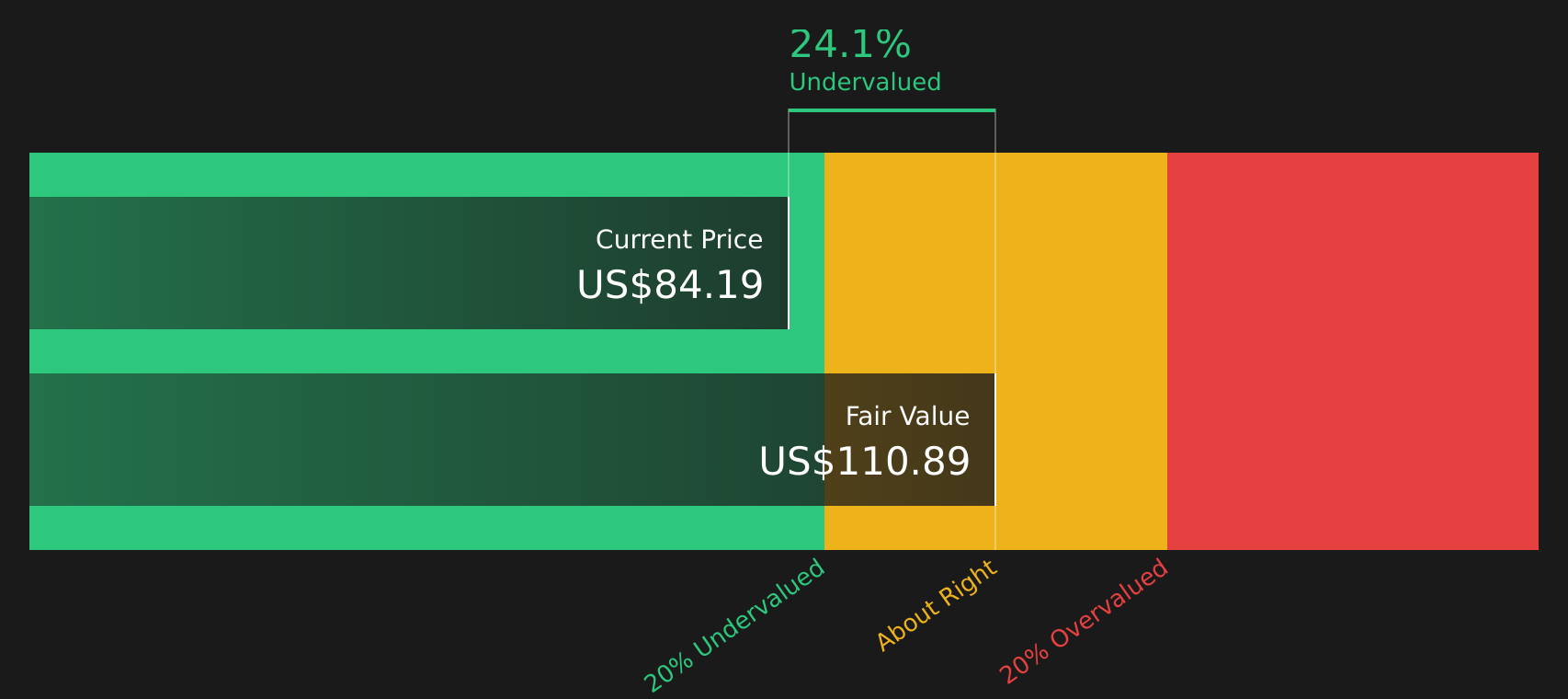

Does Kontoor Brands Look Undervalued on Cash Flow?

The Discounted Cash Flow (DCF) model values Kontoor Brands by projecting future cash the business can generate for shareholders and discounting it back to today. For Kontoor Brands, the latest twelve month free cash flow is about $392 million. The model assumes cash flows continue to grow from this level rather than move sharply higher or lower.

Based on these cash flow projections, the 2 Stage Free Cash Flow to Equity model arrives at an estimated intrinsic value of about $111 per share. This compares to a current market price that implies the stock trades at roughly a 24.5% discount to that DCF estimate. This suggests the market is pricing Kontoor Brands below what its cash flows indicate. Despite the recent Q1 revenue miss against analyst expectations, the stock price still sits below the model’s intrinsic value assessment, which helps explain why the valuation screens as attractive on a cash flow basis.

Overall, the DCF workup suggests Kontoor Brands currently appears undervalued relative to its assessed intrinsic value.

Our Discounted Cash Flow (DCF) analysis suggests Kontoor Brands is undervalued by 24.5%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Does Kontoor Brands Look Undervalued on Earnings?

P/E is a useful cross check for Kontoor Brands because the stock is covered by earnings estimates and investors often anchor on earnings-based metrics for apparel companies. Kontoor Brands currently trades at a P/E of about 16.7x, which sits below both the Luxury industry average of roughly 21.5x and the peer group average of about 24.5x.

The fair P/E multiple for Kontoor Brands, based on its profile relative to peers, is estimated at about 20.1x. Compared with the current 16.7x, the market is assigning a lower earnings multiple than this framework suggests. This implies the stock screens as undervalued on earnings despite its recent share price strength.

On balance, Kontoor Brands appears undervalued on its P/E multiple relative to both its fair ratio and sector benchmarks.

The Kontoor Brands Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Kontoor Brands valuation work leaves off by explaining which combinations of growth, margins and earnings would need to hold for the stock to be worth meaningfully more or less than today’s price. Each Narrative ties a fair value to a particular view of Kontoor Brands' potential catalysts and risks, so you can track over time which version of the story appears to be unfolding on the Community page.

Community views on Kontoor Brands are split, with one camp seeing a portfolio inflection and the other focused on demand and execution risks.

Bull case: 36% undervalued

"Kontoor's accelerated investments in digital transformation, including bespoke platforms, DTC expansion, and influencer-led digital campaigns, are fueling current double-digit digital revenue growth and are also shifting more sales to direct, high-margin channels..."

Bear case: 64% overvalued

"Demand for traditional denim and legacy brands may erode over time as younger consumers increasingly prioritize sustainability and circular fashion, challenging Kontoor's ability to grow core product revenue and maintain market share in the long term..."

Do you think there's more to the story for Kontoor Brands? Head over to our Community to see what others are saying!

The Bottom Line

Kontoor Brands screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and its earnings multiple, and those methods broadly agree that the current price embeds cautious expectations. The key question is whether Kontoor Brands can keep converting its brand strength into steady cash flows and earnings without slipping on execution or margins. If management delivers on that front, the current discount may eventually close, but if demand or profitability weakens, the lower valuation could reflect the market correctly pricing in those risks.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.