Carrier (CARR) Stock May Be 35% Undervalued Despite Its Riello Sale

Carrier Global Corp. CARR | 0.00 |

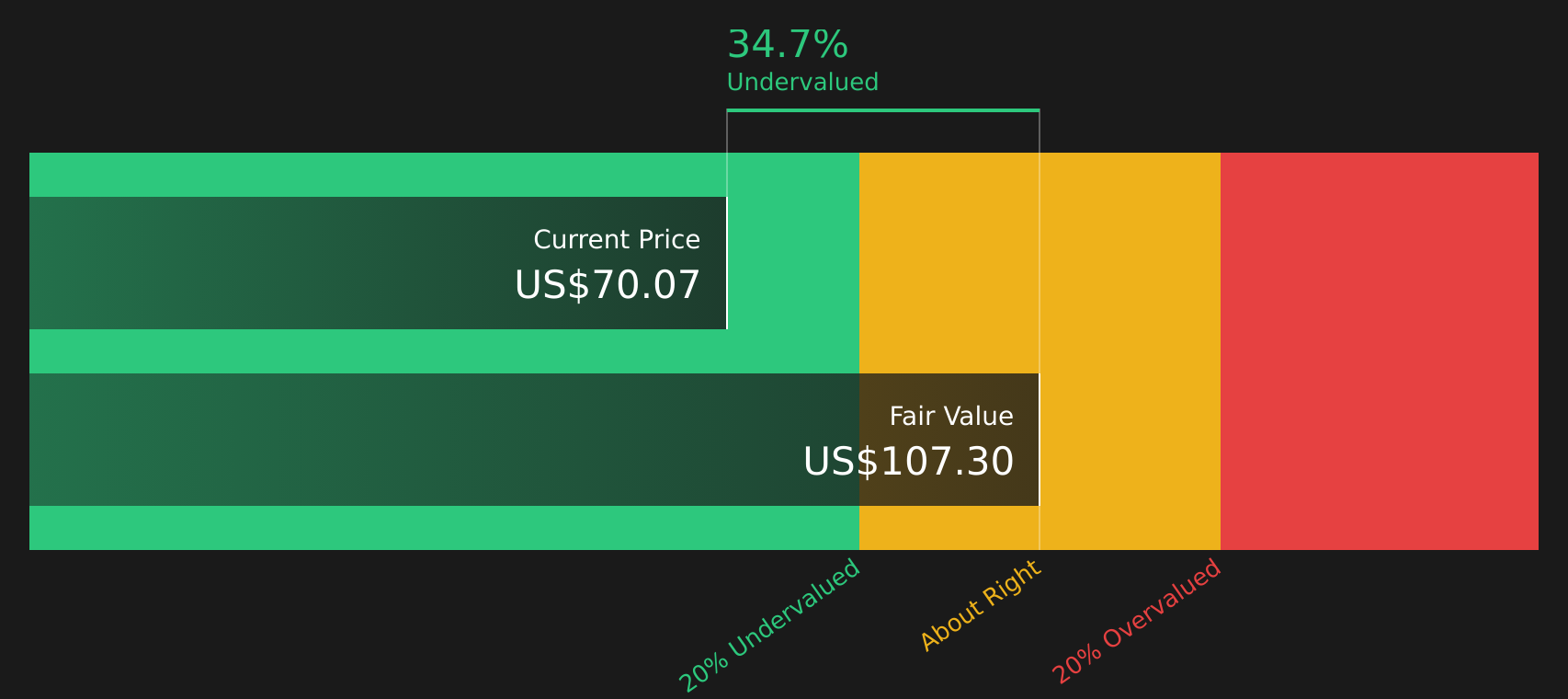

Carrier Global stock has delivered a 55.3% gain over the past five years, yet today's $70.07 share price sits in the middle of a valuation split, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to meaningful upside while market multiples paint a richer picture.

- Over five years, Carrier Global has returned 55.3%, which puts recent short term weakness into the context of a longer, positive compounding story for shareholders.

- The recent $440 million sale of the Riello business can support valuation if the proceeds are reinvested into higher return climate and energy solutions. At the same time, execution risk around capital allocation and portfolio reshaping may weigh on how much value the market assigns to these moves.

- The stock screens as undervalued under the Discounted Cash Flow (DCF) approach by about 34.7%, but with a mixed valuation score, where Carrier Global passes 3 of 6 checks, the broader picture is that it is neither a clear bargain nor clearly overpriced on all measures.

For investors, the debate is whether the intrinsic value signal or the richer earnings multiple will prove to be the better guide to where Carrier Global's valuation settles.

Is Carrier Global a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) method estimates what Carrier Global is worth today based on the cash it is projected to generate in the future. Carrier Global is currently producing latest twelve month free cash flow of about $1.63b, and the model assumes this cash flow grows over time rather than shrinking, which is consistent with a business investing behind its core climate and energy solutions.

Under these assumptions, the DCF points to an estimated intrinsic value of about $107 per share, compared with the recent $70.07 share price, suggesting the stock appears undervalued by roughly 34.7%. The recent $440 million Riello sale is described as a way to refocus on higher return areas, which provides context for why the cash flow based value is higher than the price at which the market is currently valuing Carrier Global.

On a cash flow basis, Carrier Global appears undervalued relative to the current market price.

Our Discounted Cash Flow (DCF) analysis suggests Carrier Global is undervalued by 34.7%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Has Carrier Global Run Too Far on Earnings?

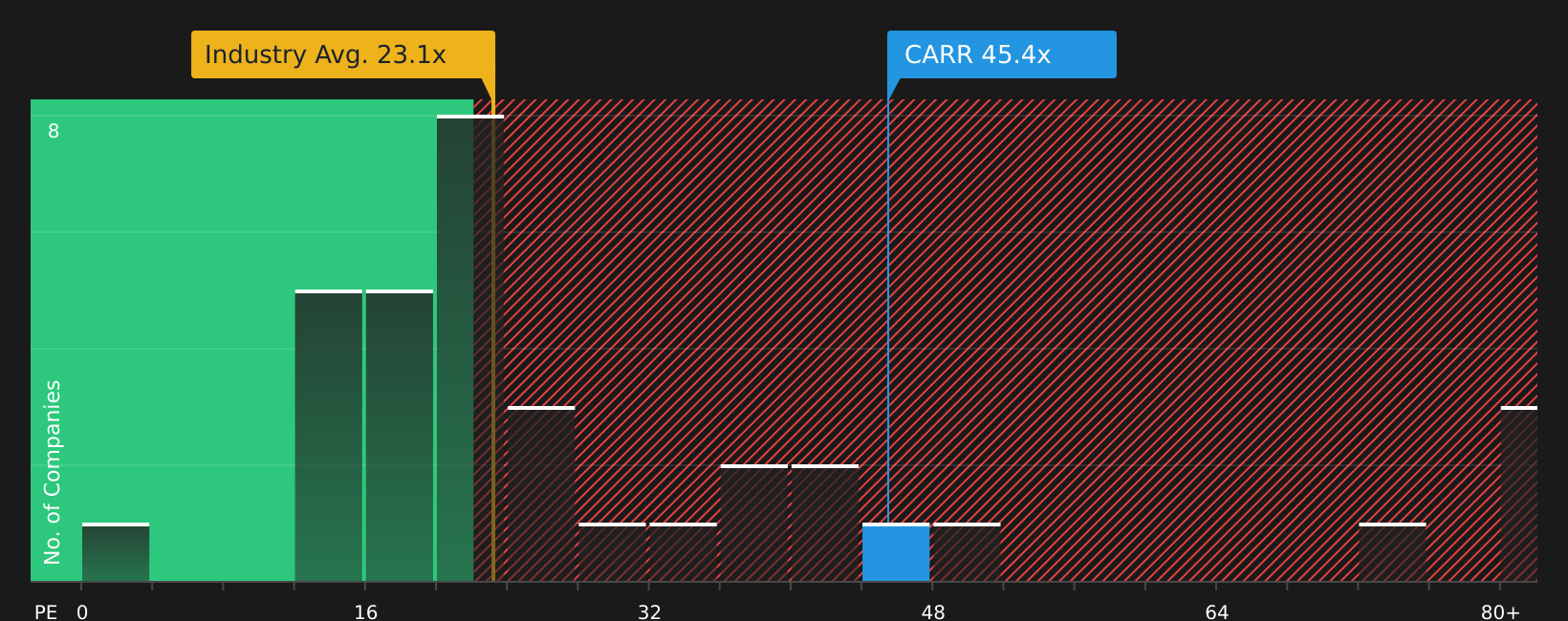

The P/E ratio is a useful way to judge what you are paying for each dollar of Carrier Global earnings. Carrier Global currently trades on a P/E of about 45.4x, which is roughly double the Building industry average of 23.1x and below the peer group average of about 74.6x.

A tailored fair P/E ratio for Carrier Global, which blends its sector, size and risk profile, sits nearer 39.8x. Set against the current 45.4x, that indicates investors are paying a premium to what this framework suggests, even though the stock does not appear as stretched as some peers. This richer P/E contrasts with the DCF signal that points to value based on cash flows, giving readers a mixed picture depending on which metric they prefer.

On earnings, Carrier Global stock currently screens as overvalued relative to the fair P/E multiple suggested by its fundamentals and industry context.

The Carrier Global Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Carrier Global sit between the DCF signal and the richer P/E multiple by spelling out which paths for Carrier Global's growth, margins and earnings would line up with a higher or lower share price than today. Instead of just giving you a single figure from a ratio or model, they unpack the future that figure depends on, so you can watch over time whether those underlying assumptions still make sense.

Community views on Carrier Global sit far apart, with some investors leaning into the long term climate and data center story while others see current expectations as already full.

Bull case: 8% undervalued

"Carrier's strategic expansion into the data center cooling market, including the development of integrated quantum leap cooling systems, sets the stage for substantial future earnings growth through an increase in market share and capitalizing on the high-demand sector..."

Bear case: 13% overvalued

"Although data center cooling orders and backlog extend into 2028 and management targets about US$1b of related sales this year, growth here is increasingly concentrated in a few large hyperscalers and colocation customers..."

Do you think there's more to the story for Carrier Global? Head over to our Community to see what others are saying!

The Bottom Line

For Carrier Global, the Discounted Cash Flow (DCF) view suggests meaningful upside based on projected cash generation, while the richer P/E multiple points to the stock being priced for strong growth and favorable sentiment already. That split, alongside a mixed broader valuation score, leaves the real question around whether cash flows grow into the current multiple or the multiple eventually settles closer to the intrinsic value estimate. The pivot away from Riello into higher return climate and energy solutions is central here, as the crux for investors is whether management turns those proceeds and future spending into durable cash flow without the market reassessing the premium multiple.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.