Carvana (CVNA) Could Be 26% Undervalued Following Its Index Reshuffle

Carvana CVNA | 0.00 |

Index reshuffle puts Carvana stock in a new peer group

Carvana (CVNA) has just been dropped from the Russell Midcap and Russell Midcap Growth benchmarks while joining the Russell Top 200 and Russell Top 200 Growth indexes, shifting its index fund investor base.

This index reshuffle changes which passive funds track Carvana, potentially affecting trading volumes and how investors compare the stock against larger and faster growing US companies rather than midcap peers.

Carvana's share price has been volatile, with a 10.02% 7 day share price return and 8.25% 90 day share price return, but a year to date share price decline of 14.30%. The 3 year total shareholder return is very large, signalling momentum that has cooled recently as investors reassess growth, competition and valuation risks.

If Carvana's index move has you thinking about where else capital is flowing, it can be useful to scan beyond autos and look at emerging leaders in other themes such as 20 top founder-led companies

With Carvana now included in large cap growth indexes, a very large 3-year total shareholder return, and the stock trading at $68.60 versus an average analyst target of $92.10, is there still upside, or is the market already pricing in future growth?

Most Popular Narrative: 25.5% Undervalued

The most followed Carvana narrative pegs fair value at $92.10, well above the last close at $68.60, framing the stock as materially discounted on those assumptions.

The company's scaled logistics and reconditioning infrastructure, bolstered by the integration of ADESA locations, is driving lower delivery and inbound transport costs. As utilization rises, these investments are expected to further enhance operating leverage, improving gross margins and profitability.

Curious what powers that $92.10 fair value for Carvana? The narrative leans on faster revenue growth, thicker margins, and a richer future earnings multiple. Want to see how those moving parts fit together in the full set of projections and timing assumptions?

Result: Fair Value of $92.10 (UNDERVALUED)

However, this Carvana narrative could be challenged if ADESA site utilization stays inefficient or if competitive pressure in used and new vehicles squeezes margins and growth assumptions.

Another View: Market Pricing for Carvana Looks Full

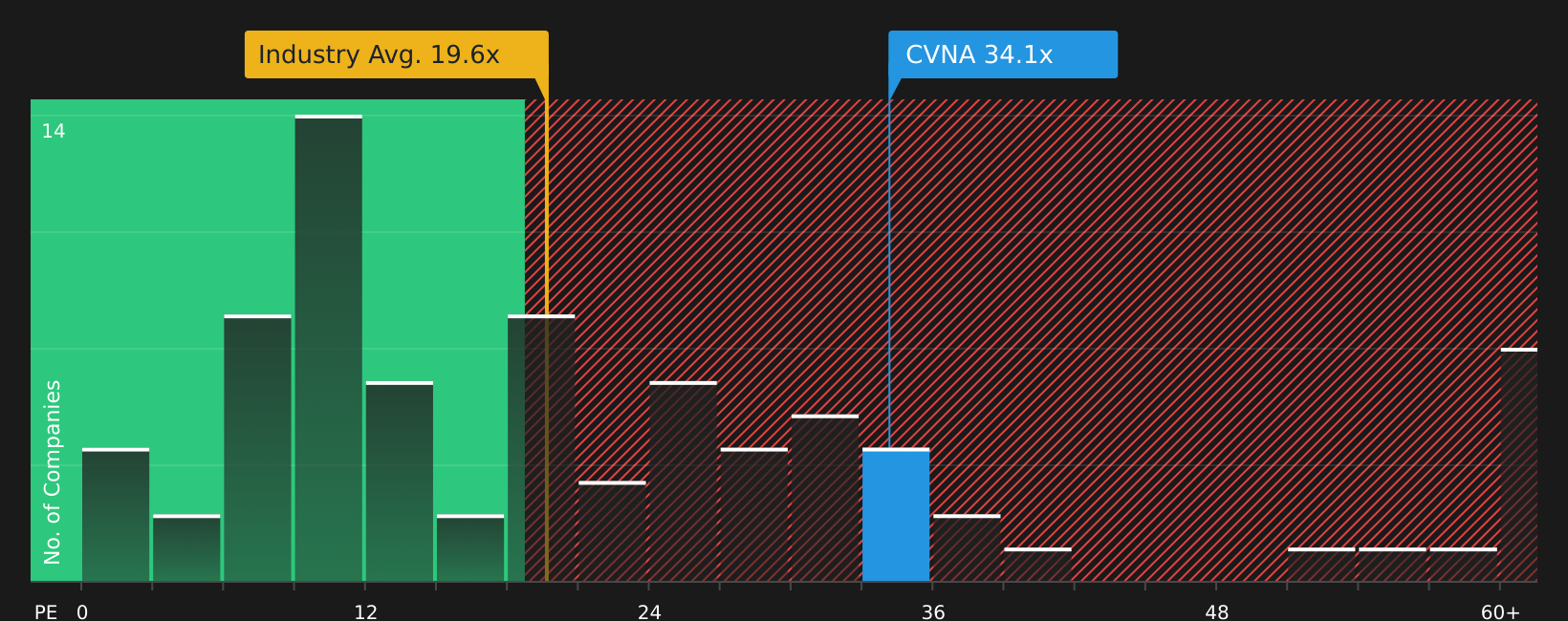

While the analyst narrative frames Carvana as 25.5% undervalued relative to a $92.10 fair value, the current P/E of 34.1x tells a different story. That is materially above the US Specialty Retail industry at 19.6x, the peer average at 18.1x, and even the 29.6x fair ratio that our model suggests the market could move toward. For investors, that gap points to valuation risk if sentiment cools, rather than an obvious cushion if expectations tighten.

To see how these valuation gaps show up in the numbers, and what they could mean if Carvana trades closer to that fair ratio over time, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on Carvana split between rich valuation signals and a popular undervalued narrative, now is the time to look through the data yourself and decide where you stand. To weigh those concerns against the potential upside in one place, start with the 3 key rewards and 2 important warning signs.

Looking for more Carvana investment ideas?

If you find Carvana interesting but do not want your portfolio leaning on a single story, use the Simply Wall St Screener to compare fresh ideas side by side.

- Spot opportunities where quality and attractive pricing line up by checking companies that pass the 44 high quality undervalued stocks.

- Strengthen the foundation of your portfolio by focusing on businesses highlighted in the solid balance sheet and fundamentals stocks screener (47 results).

- Aim to stay ahead of the crowd by reviewing companies surfaced in the screener containing 18 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.