Carvana’s Same-Day Push Tests How Far Its Logistics Edge Can Stretch Profitability (CVNA)

Carvana CVNA | 0.00 |

- Carvana recently expanded its same-day vehicle delivery and pickup service to the greater Milwaukee area, leveraging its e-commerce platform, first-party logistics network, and nearby Inspection and Reconditioning Centers to speed up both purchases and vehicle sales for local customers.

- This expansion, alongside new reconditioning capacity added at its ADESA Sarasota facility in Florida, highlights how Carvana is increasingly using integrated logistics and processing hubs to tighten fulfillment times and support operational efficiency.

- We’ll now examine how Carvana’s same-day delivery expansion and logistics build-out influences the company’s broader investment narrative and execution outlook.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

Carvana Investment Narrative Recap

To own Carvana, you need to believe that a scaled, online used car model with tightly integrated logistics can keep improving efficiency while maintaining customer appeal. In the near term, the key catalyst is whether same-day delivery and ADESA integrations translate into better operating leverage without eroding per-unit profitability. The Milwaukee same-day launch and added Sarasota reconditioning capacity support that execution story, but they also increase the risk of underutilized assets and higher per-unit costs if volume lags.

The most relevant recent announcement here is the plan to bring Inspection and Reconditioning Center capabilities to Carvana’s ADESA Sarasota site. Together with ADESA Chicago, this deepens the logistics backbone behind same-day delivery, including Milwaukee. For investors focused on catalysts, these hubs are critical enablers of faster fulfillment and lower shipping expenses, but they also interact directly with the central risk that expansion outpaces efficient utilization and puts pressure on margins and earnings quality.

Yet behind faster delivery and new facilities, there is a growing risk that higher fixed costs and underused logistics capacity could quietly weigh on results that investors should be aware of...

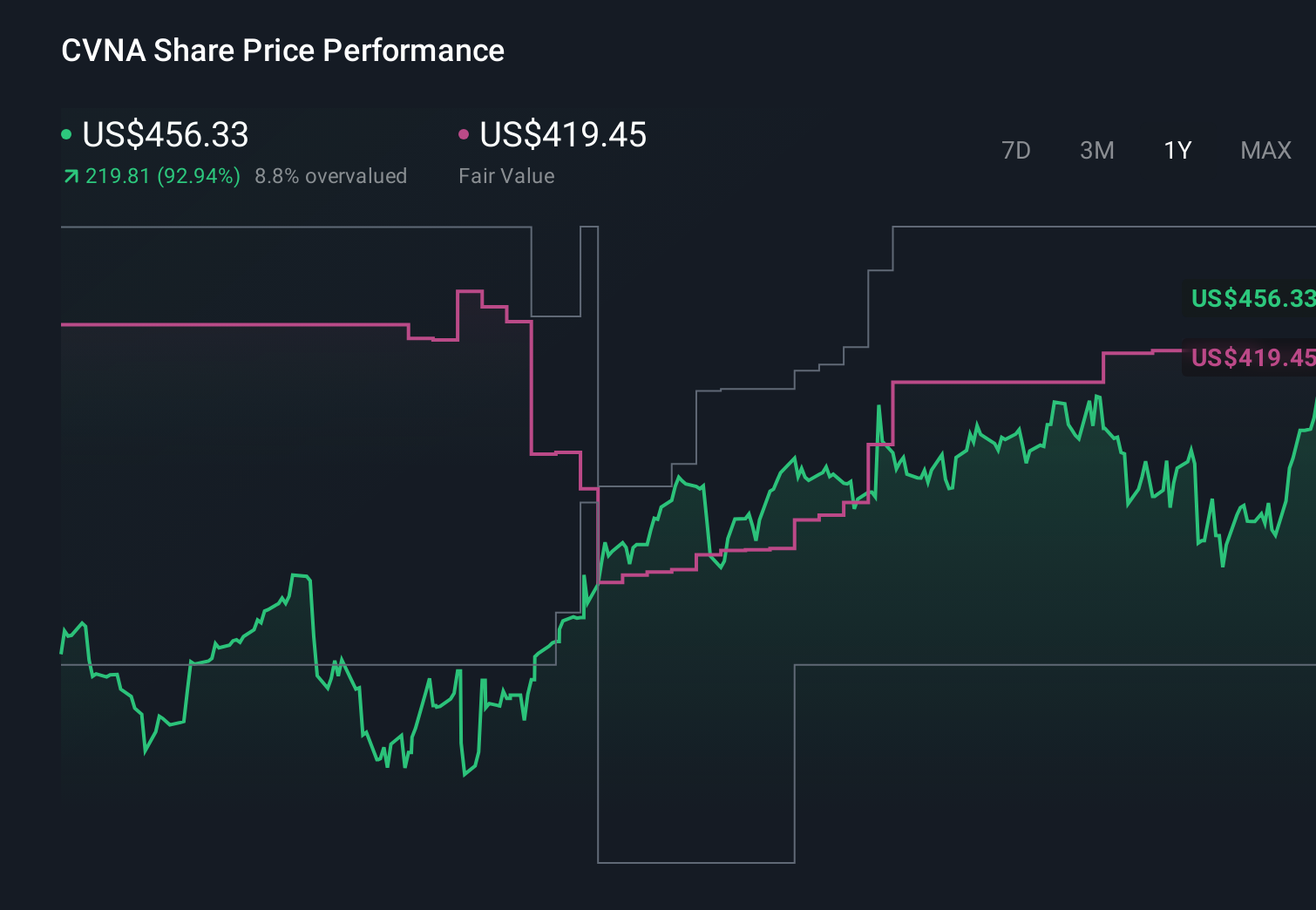

Carvana's narrative projects $44.2 billion revenue and $3.0 billion earnings by 2029.

Uncover how Carvana's forecasts yield a $92.10 fair value, a 40% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view that logistics expansion can gradually improve margins, the most bearish analysts assume Carvana’s profit margin slips from 6.4% to 4.4% by 2029, even as revenue climbs toward about US$39.5 billion, reminding you that expectations for the same news can differ sharply and may shift again as the impact of same day delivery rollouts becomes clearer.

Explore 7 other fair value estimates on Carvana - why the stock might be worth less than half the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Carvana research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Ready For A Different Approach?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 41 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.