Castle Biosciences (CSTL) Valuation After Upgraded Guidance And Higher Analyst Growth Expectations

Castle Biosciences CSTL | 24.84 | -0.84% |

Castle Biosciences (CSTL) kicked off 2026 with fresh guidance pointing to 2025 revenue above US$340 million, supported by double digit growth in core test volumes and closely watched by analysts.

The stock’s 90 day share price return of 84.06% and 1 year total shareholder return of 62.42% suggest momentum has been building, even though the 5 year total shareholder return of 49.49% is still negative.

If Castle Biosciences’ update has you thinking more broadly about health related trends, it could be a useful moment to scan through healthcare stocks for other potential ideas.

With the shares up sharply over the past year and analysts lifting their targets, the key question now is whether Castle Biosciences still trades at a discount or if the market is already pricing in future growth.

Most Popular Narrative: 4.1% Undervalued

The most followed narrative puts Castle Biosciences’ fair value at US$42.50, just above the last close of US$40.75, framing a relatively tight valuation gap.

The analysts have a consensus price target of $35.625 for Castle Biosciences based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $41.0, and the most bearish reporting a price target of just $30.0.

Curious how a company that is still loss making supports a premium future P/E multiple and higher assumed margins? The narrative leans on modest revenue growth, margin expansion and a valuation framework that stretches well beyond typical healthcare benchmarks.

Result: Fair Value of $42.50 (UNDERVALUED)

However, that premium narrative can quickly be challenged if reimbursement setbacks for DecisionDx-SCC persist, or if new tests fail to secure broad payer coverage and adoption.

Another View: Multiples Paint A Tougher Picture

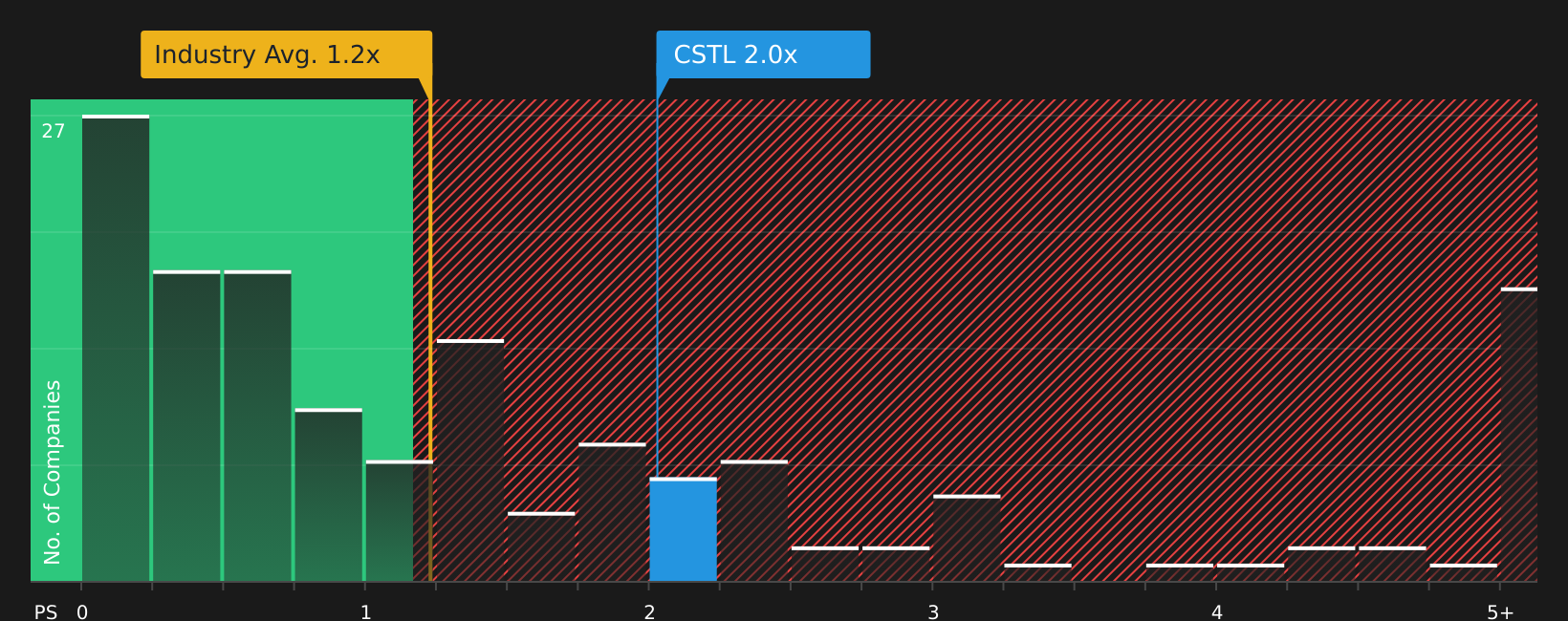

That 4.1% undervalued fair value narrative sits awkwardly beside how the market is pricing Castle Biosciences on sales. The shares trade on a P/S of 3.5x, compared with 1.3x for the US Healthcare industry, 2.1x for peers, and a fair ratio of 3.3x. This points to richer expectations and less cushion if sentiment cools.

Build Your Own Castle Biosciences Narrative

If you see the numbers differently or simply prefer to work through the assumptions yourself, you can rebuild the story in just a few minutes: Do it your way.

A great starting point for your Castle Biosciences research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you want to keep your edge, do not stop at a single stock. Use the Simply Wall St Screener to surface focused, data driven ideas fast.

- Target growth potential by scanning these 3539 penny stocks with strong financials that already show stronger financial foundations than many expect from low priced names.

- Ride transformative tech trends by checking out these 24 AI penny stocks that are linked to artificial intelligence themes across different parts of the market.

- Hunt for mispriced opportunities by reviewing these 867 undervalued stocks based on cash flows where current prices sit below what their cash flows might justify.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.