Cava Group (CAVA): Evaluating Valuation Following Recent Share Price Decline

CAVA Group, Inc. CAVA | 81.01 | +0.14% |

CAVA Group (CAVA) has shown some dramatic shifts in recent trading, with the stock down almost 28% over the past 3 months. These moves have caught the attention of investors, who are now wondering what’s next for this fast-casual restaurant chain.

After a huge rally following its IPO, CAVA Group’s momentum has decidedly faded, with a 1-year total shareholder return of -53.6% highlighting broad investor caution around rising costs and sustaining growth. Still, the stock’s shorter-term price action tells a story of cautious optimism as buyers test the waters at current levels.

Interested in discovering what else is catching investors’ attention right now? This could be the perfect opportunity to broaden your search with fast growing stocks with high insider ownership

Given CAVA’s drop from its highs and the stock trading at a sizable discount to analyst targets, is the market overlooking future growth or is this a fair reflection of the company’s prospects? Is there a real buying opportunity, or has everything already been priced in?

Most Popular Narrative: 30.7% Undervalued

With CAVA Group’s fair value estimated at $90.73 by the most popular narrative, the last close of $62.86 points to a significant gap. This sets up a sharp contrast between where the market has landed and what analysts project, making the financial assumptions behind that estimate especially intriguing.

Rapid geographic expansion into new and underserved markets, supported by strong new unit performance and a robust target of at least 1,000 restaurants by 2032, is likely to accelerate systemwide sales and drive higher topline revenue growth. Growing consumer demand among younger demographics for healthy, flavorful, and customizable dining, especially Mediterranean cuisine, positions CAVA to benefit from increased customer traffic and enhanced brand equity, supporting both revenue and long-term pricing power.

Want to know what’s driving this bold fair value? Only one key variable is the linchpin for the narrative’s high upside. Guess which future financial milestone could push CAVA to a valuation that rivals sector leaders? Get the backstory and numbers that shape this call. There is more behind the scenes than meets the eye.

Result: Fair Value of $90.73 (UNDERVALUED)

However, heavy reliance on Mediterranean cuisine and rapid expansion could backfire if consumer tastes shift or new locations underperform. This may threaten future growth projections.

Another View: Multiples Suggest a Premium Price

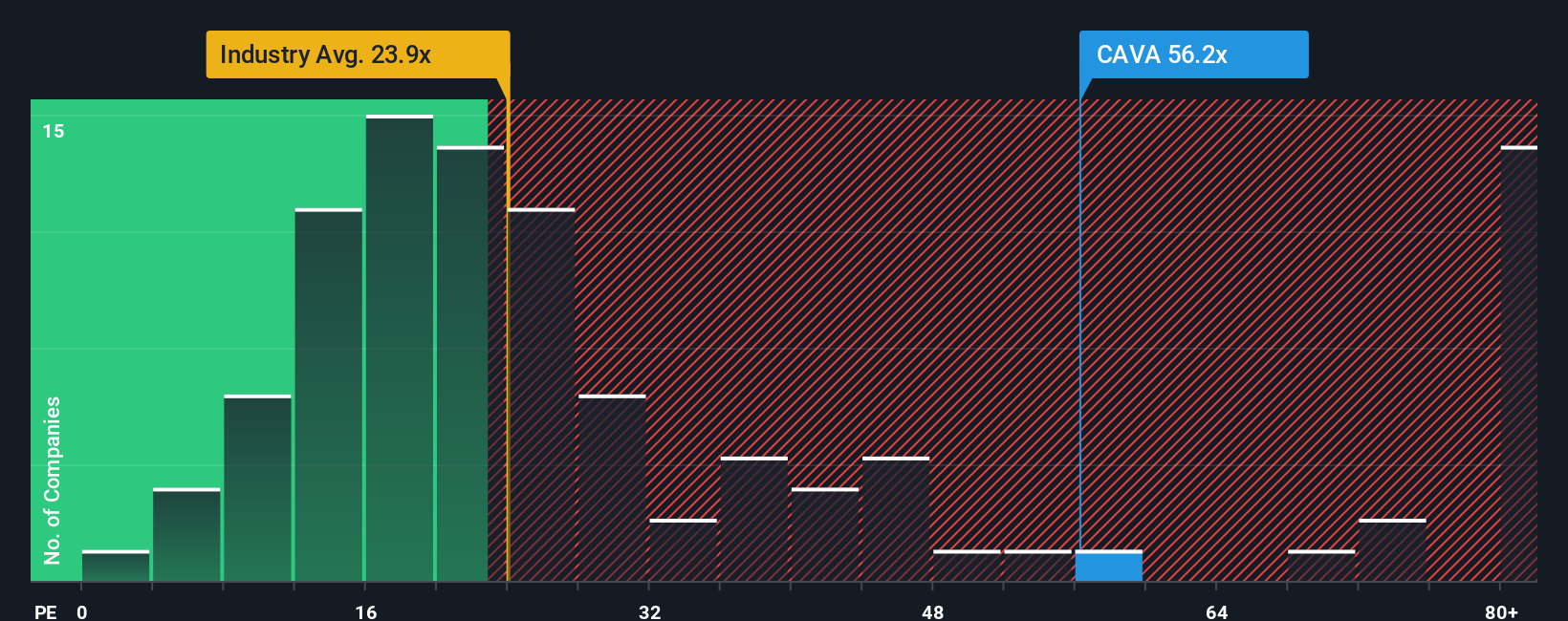

Looking at CAVA's valuation through the price-to-earnings lens tells a less optimistic story. The stock trades at 51.8 times earnings, which is well above the hospitality industry average of 23.5 times and even higher than the peer average of 51.4 times. The fair ratio, based on SWS’s analysis, is just 22.1 times. This gap means investors are paying a notable premium for the company’s growth story. Could this reflect upside potential, or is the bar set too high?

Build Your Own CAVA Group Narrative

If you want to look beyond the current story and test your own assumptions, it’s quick and easy to build a fresh perspective from the same numbers. Do it your way

A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Why settle for the usual picks when smarter, high-potential opportunities are right at your fingertips? Take the next step and boost your chances of finding tomorrow’s standout investments.

- Strengthen your portfolio with income strategies by locking in yields greater than 3% with these 18 dividend stocks with yields > 3%.

- Make your move into transformative tech by targeting growth potential in artificial intelligence using these 24 AI penny stocks.

- Capitalize on untapped value by pinpointing stocks trading below their cash flow potential through these 878 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.