Centene (CNC) Is Up 9.7% After EPS Upgrade, Debt Cut and Analyst Boost - What's Changed

Centene Corporation CNC | 0.00 |

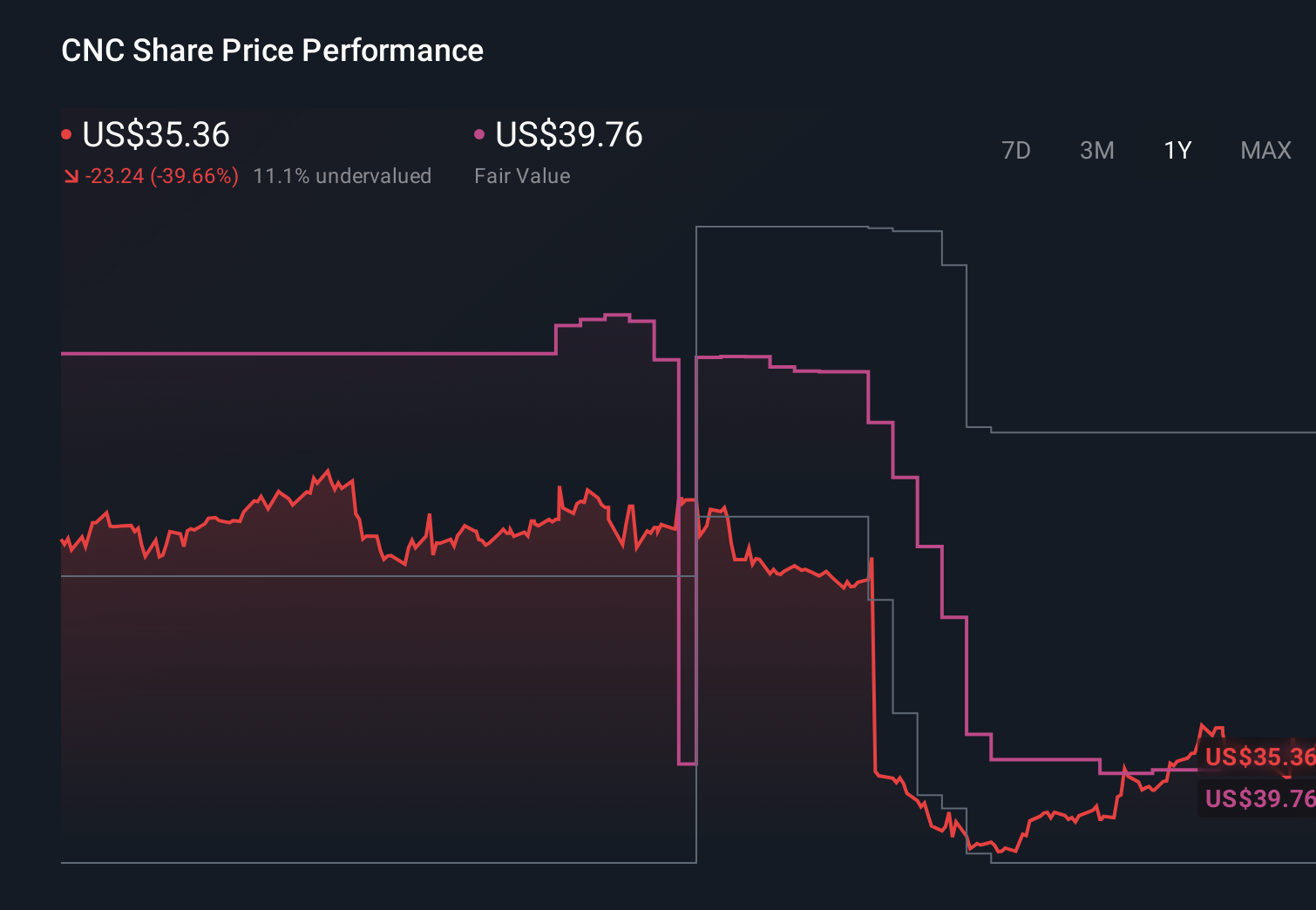

- In recent days, Centene reported strong Q1 2026 results, raised its full‑year adjusted diluted EPS guidance, and cut its debt by US$1.00 billion, while also earning a place on Bank of America’s US 1 List and renewed support from other major analysts.

- This combination of better‑than‑planned earnings, balance sheet strengthening, and heightened institutional attention reinforces Centene’s position as a key player in government‑sponsored healthcare and managed care.

- Now we’ll examine how Centene’s upgraded earnings guidance and debt reduction may influence its existing investment narrative and risk‑reward profile.

Capitalize on the AI infrastructure supercycle with our selection of the 48 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Centene Investment Narrative Recap

To own Centene, you need to believe in the durability of government sponsored healthcare and the company’s ability to restore and protect margins in Medicaid, Medicare, and Commercial plans. The Q1 2026 earnings beat, higher EPS guidance, and US$1.0 billion debt reduction appear supportive of that margin recovery story, while the biggest near term risk still centers on policy and rate decisions that may not keep pace with rising medical and drug costs.

Among the recent announcements, the raised full year adjusted diluted EPS guidance above US$3.40 stands out as most relevant. It directly connects to the key catalyst of margin repair across Medicaid and Medicare, following prior pressure from flu related costs, specialty drugs, and rate adequacy debates. Stronger guidance does not remove those risks, but it gives investors more concrete numbers to compare against their expectations for how quickly Centene can stabilize earnings.

Yet against this improving picture, the possibility of tighter reimbursement or slower rate updates remains a risk investors should be aware of if...

Centene's narrative projects $199.9 billion revenue and $2.7 billion earnings by 2029. This requires 3.9% yearly revenue growth and an $9.1 billion earnings increase from -$6.4 billion today.

Uncover how Centene's forecasts yield a $54.94 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were already assuming Centene could lift revenue to about US$205.6 billion and earnings to roughly US$3.0 billion by 2029, which is far more ambitious than consensus. In light of the latest results and guidance, you may find that your own view on Medicaid margin recovery or digital cost savings sits closer to these higher expectations or remains more cautious, so it can help to compare several viewpoints before deciding what you believe.

Explore 15 other fair value estimates on Centene - why the stock might be worth 46% less than the current price!

The Verdict Is Yours

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Centene research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Centene research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Centene's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 26 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.