Cheniere Energy Partners (CQP) Prices $2b Notes, Is The Current Valuation Fully Valued?

Cheniere Energy Partners, L.P. CQP | 0.00 |

Cheniere Energy Partners (CQP) recently priced a $2 billion senior notes offering in two long-dated tranches, with proceeds earmarked for debt refinancing, capital expenditures, and its Sabine Pass LNG expansion contract with Bechtel.

At a share price of $61.93, Cheniere Energy Partners has seen a 1-day share price return of 0.96% and a year to date share price return of 14.69%. Its 1-year total shareholder return of 18.40% and 5-year total shareholder return of 93.45% point to momentum that has built over time, despite a 90-day share price return that is down 6.10%. This sets the context for how investors may read this new $2 billion notes issue and the Sabine Pass expansion contract.

If this type of LNG infrastructure story interests you, it could be a good moment to broaden your watchlist with 89 nuclear energy infrastructure stocks

Cheniere Energy Partners appears to be a solid LNG infrastructure business, backed by a large, contracted asset at Sabine Pass and fresh long term funding in place. The key question for investors now is how the current unit price compares with that reality.

Price-to-Earnings of 14.5x: Is it justified?

On a P/E of 14.5x, Cheniere Energy Partners screens as cheaper than the broader US market but slightly more expensive than its own Oil and Gas industry, which gives investors a mixed valuation signal at a last close of $61.93.

The P/E ratio compares the current unit price with earnings per unit, so it reflects what investors are currently paying for each dollar of Cheniere Energy Partners' earnings. For a mature, infrastructure heavy LNG exporter with a large contracted asset base and 5 year earnings growth of 13.6% per year, this is a central yardstick many investors use to frame expectations.

Against that backdrop, the stock looks inexpensive when set beside both the US market P/E of 19.2x and the estimated "fair" P/E of 18.4x. That suggests the current market pricing is below the level our fair ratio work indicates could be justified if earnings and business quality track recent trends.

The picture shifts when you compare Cheniere Energy Partners to the US Oil and Gas industry average P/E of 13x, where CQP trades at a premium. Here, investors are paying more than the sector average for each dollar of earnings, and that higher tag likely reflects the market's view of its specific LNG infrastructure position and earnings profile rather than a blanket sector read across.

Result: Price-to-Earnings of 14.5x (ABOUT RIGHT)

However, Cheniere Energy Partners still faces risks, including potential project execution issues at Sabine Pass and any shift in LNG demand that affects long term contracts.

Another View: What the SWS DCF Model Says About Cheniere Energy Partners

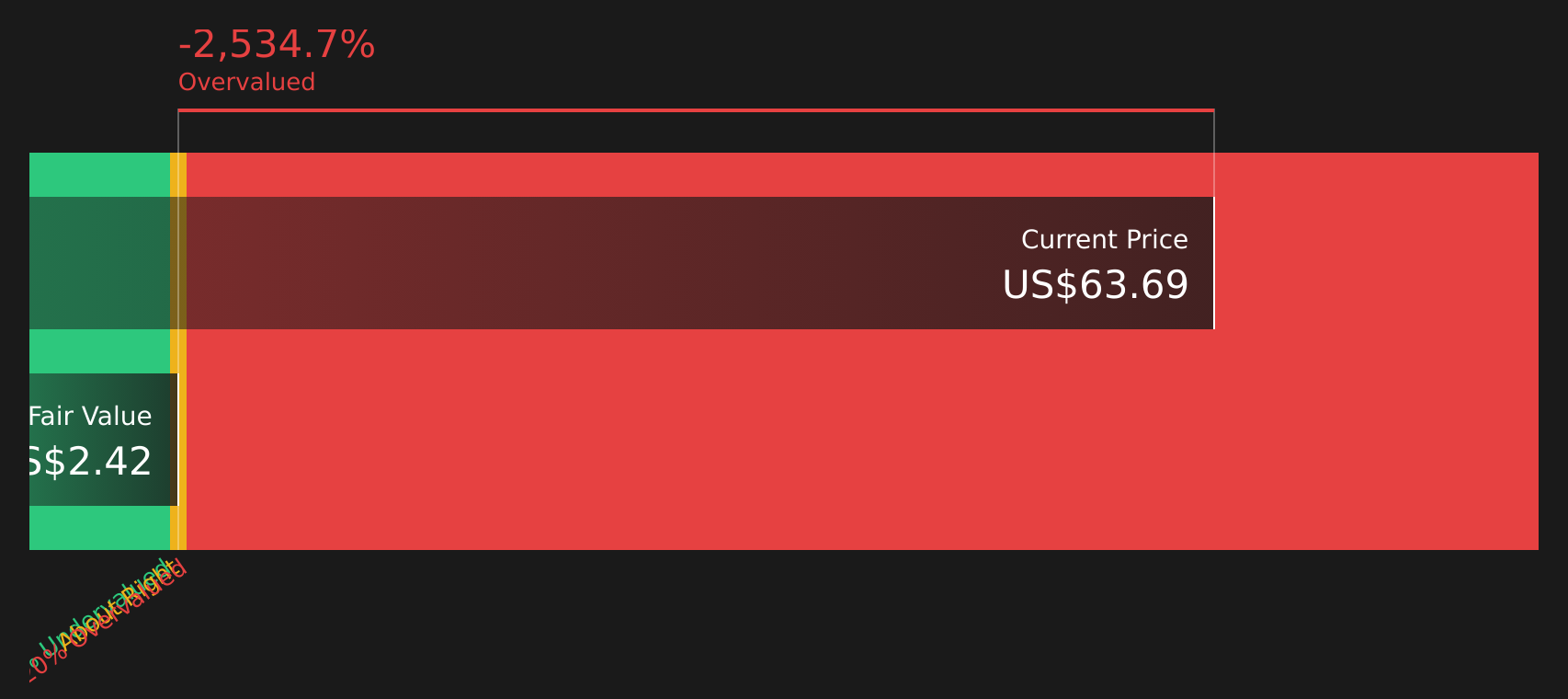

While the P/E of 14.5x puts Cheniere Energy Partners in the “about right” bucket, the SWS DCF model tells a very different story. With the unit price at $61.93 versus an estimated future cash flow value of $2.42, this approach points to a stock that screens as heavily overvalued. Which lens do you trust more when cash flow and earnings are so far apart?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cheniere Energy Partners for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 41 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mixed signals around Cheniere Energy Partners leave you unsure, treat that as your cue to check the numbers yourself and weigh both sides of the story. To see the balance of concerns and upside that others are focusing on, start with the 2 key rewards and 2 important warning signs.

Looking for more investment ideas beyond Cheniere Energy Partners?

If you want a broader view than Cheniere Energy Partners alone, the Simply Wall Street Screener can help you quickly spot other opportunities that fit your style.

- Zero in on potential value opportunities by reviewing 41 high quality undervalued stocks that combine attractive prices with solid fundamentals.

- Build a steadier income stream by checking out 8 dividend fortresses with higher yields that may complement your existing holdings.

- Strengthen the core of your portfolio by focusing on solid balance sheet and fundamentals stocks screener (47 results) that can help you stay comfortable through different market conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.