Chubb (CB) Valuation Check As Investor Interest Builds Without A Single Driving Headline

Chubb Limited CB | 0.00 |

Recent performance snapshot for Chubb (CB)

Without a clear single news headline driving attention, Chubb (CB) has still been on many investors' radar, with recent returns and current pricing offering a fresh snapshot of how the stock is trading.

Chubb’s recent share price has eased back from shorter term highs, with a 1 day share price return showing a 2.03% decline and a 90 day share price return of 8.38%. The 1 year total shareholder return of 18.36% and 5 year total shareholder return of 104.99% reflect stronger longer term momentum.

If you are comparing Chubb with other financially resilient names, this is a good moment to broaden your search and check out the solid balance sheet and fundamentals stocks screener (42 results)

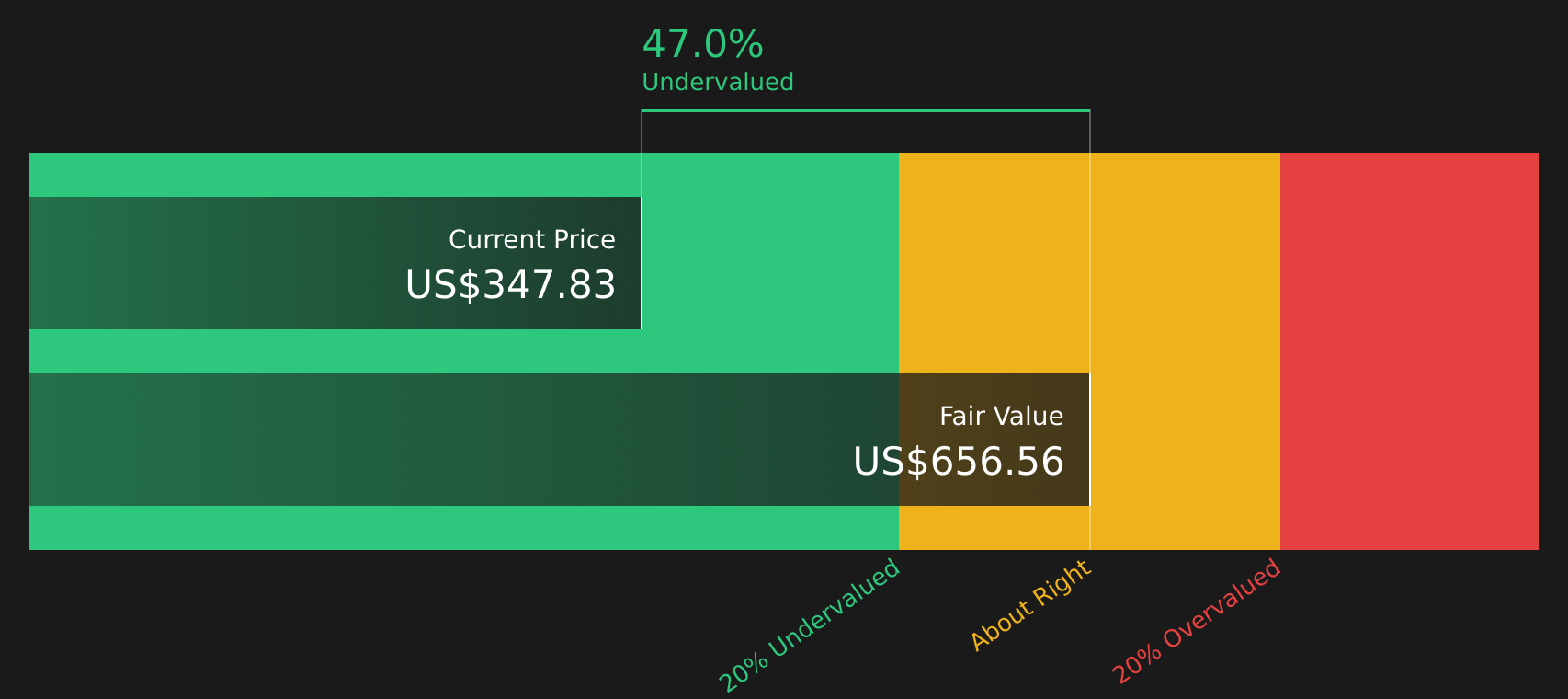

With Chubb trading at $326.12 and sitting at a sizeable intrinsic discount, the key question is whether the current valuation signals underappreciated earnings power or whether the market is already pricing in the company’s future growth.

Most Popular Narrative: 32% Overvalued

According to iStock, the most followed narrative pegs Chubb’s fair value at $247.08, which sits well below the last close of $326.12, creating a clear valuation gap in the model.

Chubb Limited’s future growth prospects are influenced by several strategic initiatives, market trends, and external factors. Here is an analysis of the factors that are likely to drive Chubb’s growth in the coming years:

Want to see what underpins that lower fair value? The narrative focuses on specific revenue trajectories, margin assumptions, and earnings paths that differ from current pricing. The contrast between these inputs and today’s share price is where the story becomes more detailed.

Result: Fair Value of $247.08 (OVERVALUED)

However, this view could shift quickly if Chubb’s annual revenue and net income growth remain weak, or if sector competition pressures the 17.92% profit margin.

Another angle on valuation

The iStock narrative points to Chubb being 32% overvalued at $326.12 versus a $247.08 fair value, yet our SWS DCF model suggests something very different, with an estimated future cash flow value of $672.27. When two models disagree this much, which set of assumptions do you trust more?

Next Steps

If this mix of risks and potential rewards feels finely balanced, move quickly, review the underlying data for yourself, then weigh up the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If you are weighing up what to do next, now is a smart time to widen your search and line up a few well curated alternatives to Chubb.

- Target potential mispricing by scanning 56 high quality undervalued stocks that pair quality fundamentals with prices that may not fully reflect their underlying cash flows.

- Strengthen your income focus by reviewing 13 dividend fortresses built around companies offering higher yields with an emphasis on resilience.

- Prioritise capital preservation by checking 72 resilient stocks with low risk scores where lower risk scores sit alongside steadier financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.