Clearway Energy (CWEN.A) Valuation Check After Strong One Year Shareholder Return

Clearway Energy, Inc. Class A CWEN.A | 40.21 | +1.16% |

Clearway Energy (CWEN.A) has drawn investor interest with a recent share price near $37.33, along with a mix of revenue and net income trends that invites a closer look at how the business is currently positioned.

At a share price of $37.33, Clearway Energy has seen firm short term momentum, with a 20.77% 1 month share price return and a 16.22% year to date share price return contributing to a 61.10% 1 year total shareholder return. This indicates that sentiment has been strengthening recently.

If this clean energy story has caught your attention, it could be a good moment to widen your watchlist with our screener of 24 power grid technology and infrastructure stocks as another way to find potential opportunities tied to grid reliability and energy transition themes.

With the shares sitting close to analysts’ price target yet showing a very large intrinsic value gap, the key question is whether Clearway is still underpriced or if the market is already factoring in future growth.

Most Popular Narrative: 1.8% Undervalued

Clearway Energy's most followed narrative currently anchors fair value at $38, only slightly above the $37.33 share price, which keeps expectations finely balanced.

The analysts have a consensus price target of $36.111 for Clearway Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $40.0, and the most bearish reporting a price target of just $34.0.

Read the complete narrative. Read the complete narrative.

Curious how a fair value of $38 emerges with only a small gap to today's price? Revenue assumptions, margin shifts, and a higher future earnings multiple all carry real weight here. The full narrative walks through those levers in detail so you can judge whether the implied path feels realistic or stretched.

Result: Fair Value of $38 (UNDERVALUED)

However, this hinges on financing remaining accessible and contract terms staying favorable, so tighter credit or weaker PPA pricing could quickly challenge that underpriced label.

Another View: Earnings Multiple Sends a Different Signal

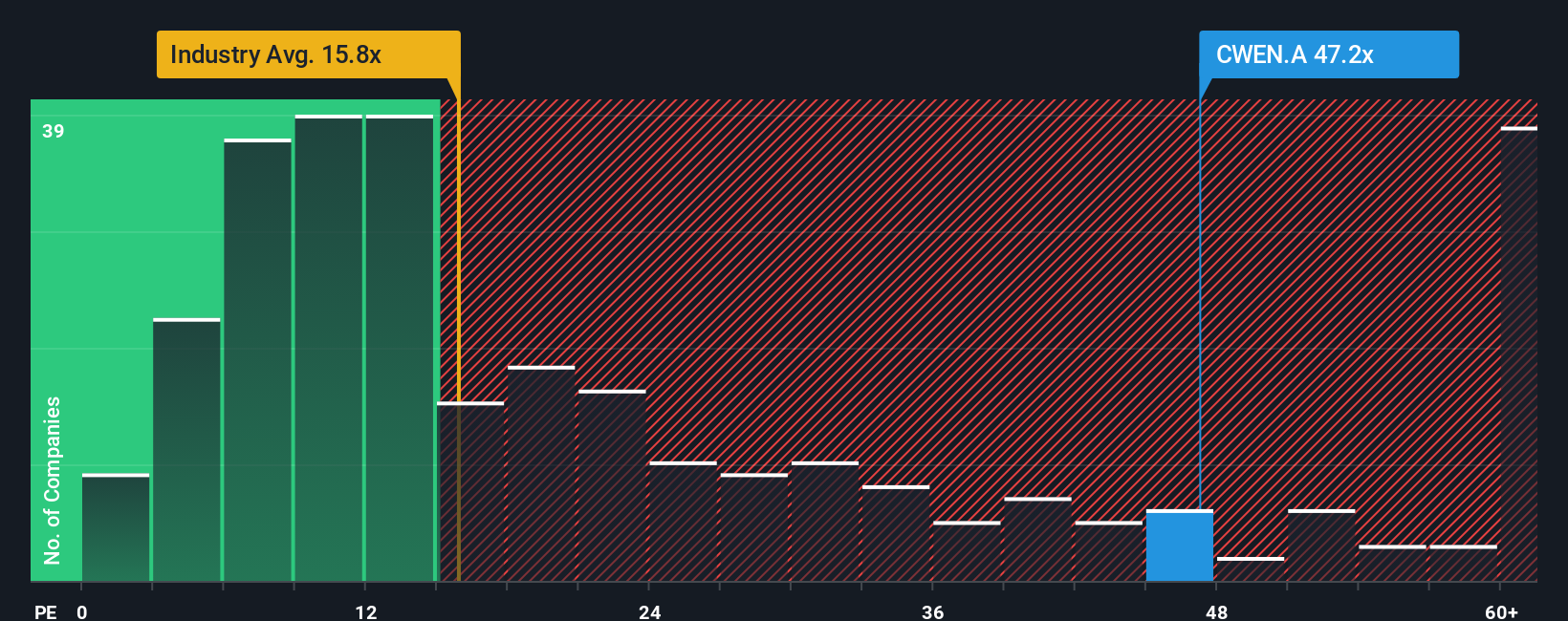

While the SWS DCF model points to a large gap to fair value, the current P/E of 16.2x tells a more cautious story. It is close to the global renewable energy average of 16.3x, below the peer average of 27.8x, yet above the fair ratio of 9.9x. That mix raises a simple question for you: is this a margin of safety or a valuation risk if sentiment cools?

Build Your Own Clearway Energy Narrative

If you look at the numbers and reach a different conclusion, or simply prefer building your own thesis step by step, you can spin up a tailored Clearway view in just a few minutes: Do it your way.

A great starting point for your Clearway Energy research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Clearway Energy is on your radar, do not stop there. The screener can quickly surface other focused ideas that fit the way you like to invest.

- Target reliable cash flows by scanning companies that feature 13 dividend fortresses that might appeal if income stability is high on your checklist.

- Hunt for quality at a sensible price with our list of 51 high quality undervalued stocks that pair fundamentals with what some investors may see as room for upside.

- Prioritise resilience by reviewing 85 resilient stocks with low risk scores that some investors use when they want fewer surprises and steadier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.