Clover Health Investments (CLOV) Q1 Beat And Guidance Raise Put Valuation Back In Focus

Clover Health CLOV | 0.00 |

Clover Health Investments (CLOV) is back in focus after Q1 results that beat revenue expectations, came with higher full year EBITDA guidance, strong customer additions, and a higher Medicare star rating following a favorable court ruling.

Clover Health Investments has seen sharp share price swings, with a 30 day share price return of 31.83% and a 90 day share price return of 205.81%, while the 1 year total shareholder return of 105.47% points to strong recent momentum despite a 5 year total shareholder return that is still down 43.26%.

Those moves have been closely tied to the recent Q1 earnings beat, higher full year EBITDA guidance, and upgraded Medicare star rating. Mandated insider share sales linked to equity compensation may have briefly cooled sentiment without signaling a change in the underlying business story.

If Clover Health Investments has caught your attention, it can be useful to see how other healthcare focused AI stocks are trading, starting with the 40 healthcare AI stocks.

After a very strong Q1, Clover Health Investments now trades well above analysts’ average price target but at a sizeable discount to some intrinsic value estimates, raising a key question for investors: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 27% Overvalued

The most followed narrative sets a fair value for Clover Health Investments at $4.15, compared with the latest close at $5.26, and anchors that view in detailed growth, margin, and valuation assumptions.

The analysts have a consensus price target of $4.15 for Clover Health Investments based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $4.75, and the most bearish reporting a price target of just $3.5.

Want to see what makes this narrative tick? It leans on rapid revenue expansion, a swing into profitability, and a future earnings multiple that stands well above sector norms.

Result: Fair Value of $4.15 (OVERVALUED)

However, this Clover Health Investments narrative could be knocked off course if higher medical and pharmacy utilization keeps pressure on margins, or if Medicare Advantage reimbursement rules turn less favorable.

Another View: Multiples Point To A Different Story

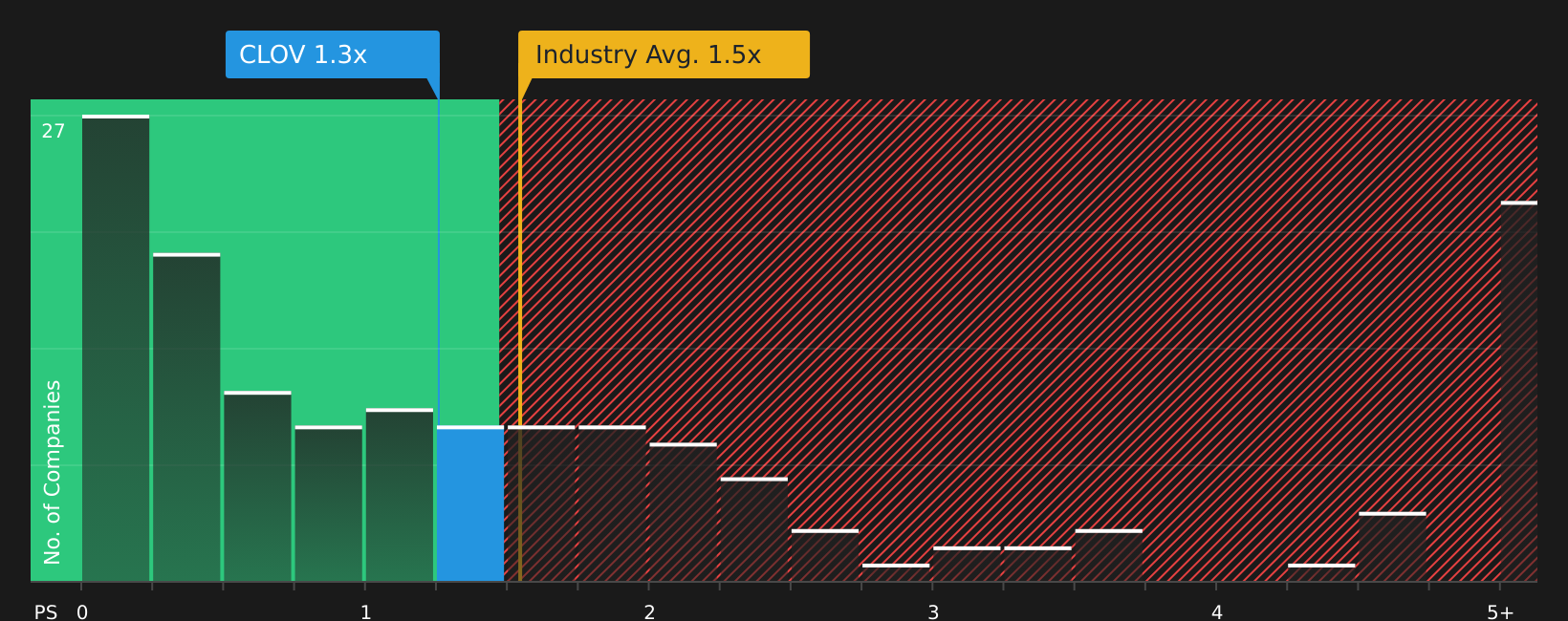

While the most popular narrative pegs Clover Health Investments at $4.15 and labels the stock 27% overvalued, the current market pricing hints at something more complicated. On a P/S of 1.3x, Clover trades below the US Healthcare industry at 1.5x and below peer averages of 2.3x, and in line with a fair ratio of 1.3x, which suggests the market already prices in some caution but not clear excess. For investors, the real question is whether that gap signals valuation risk if expectations fade, or room for upside if the story continues to improve.

Next Steps

Curious whether the recent excitement around Clover Health Investments lines up with the underlying risks and rewards investors are watching? To pressure test the story yourself and see both sides of the argument, start with the breakdown of 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Clover Health Investments?

If Clover Health Investments has sharpened your focus on quality opportunities, do not stop here. Broaden your watchlist now using carefully built screeners across the market.

- Target potential mispricing by checking companies that combine solid fundamentals with attractive valuations using the 44 high quality undervalued stocks.

- Strengthen your downside protection by focusing on companies with healthier finances and sturdier profiles through the solid balance sheet and fundamentals stocks screener (47 results).

- Spot under-the-radar opportunities early by reviewing the screener containing 18 high quality undiscovered gems before they attract wider attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.