Corteva (CTVA) Valuation Check As Strong Q1 Results And Planned Split Draw Investor Interest

Corteva Inc CTVA | 0.00 |

Corteva (CTVA) has investors’ attention after reporting first quarter 2026 results, reaffirming its full year outlook and outlining progress on its planned split into two independent agriculture focused companies.

The Q1 report, reaffirmed 2026 outlook and ongoing buybacks appear to be feeding into improving sentiment. The share price is US$82.83, with a year to date share price return of 22.24% and a 1 year total shareholder return of 23.08%, indicating solid recent momentum built on a stronger 90 day share price return of 11.60%.

If Corteva’s recent move has you thinking about where else growth and cash generation could show up in the market, it may be worth scanning 19 top founder-led companies

With the stock up strongly over the past year, trading at US$82.83 and sitting at a roughly 24% discount to one intrinsic value estimate and about 7% below analyst targets, is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 3.7% Undervalued

Against Corteva’s last close of $82.83, the most followed fair value narrative sits at $86.05, implying a modest gap that hinges on future execution.

Advancements in Corteva's innovation pipeline including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Want to see what sits behind that earnings ramp and margin lift, and how long it is expected to last? The narrative leans on steady top line expansion, widening profitability, and a richer mix of higher value products, all filtered through a specific discount rate and future earnings multiple that do a lot of work in the model.

The fair value estimate of $86.05 uses a 7.35% discount rate and assumes Corteva can compound revenue and profit margins over time, while the market currently prices the stock slightly below that narrative. The tension for investors is whether current cash generation, the crop protection cycle, and the planned separation of SpinCo will track closely enough to those revenue, earnings and valuation multiple assumptions to close the gap or widen it.

Result: Fair Value of $86.05 (UNDERVALUED)

However, the story can change quickly if crop protection pricing pressure persists or if currency swings in key markets continue to weigh on revenue and earnings expectations.

Another Angle on Valuation

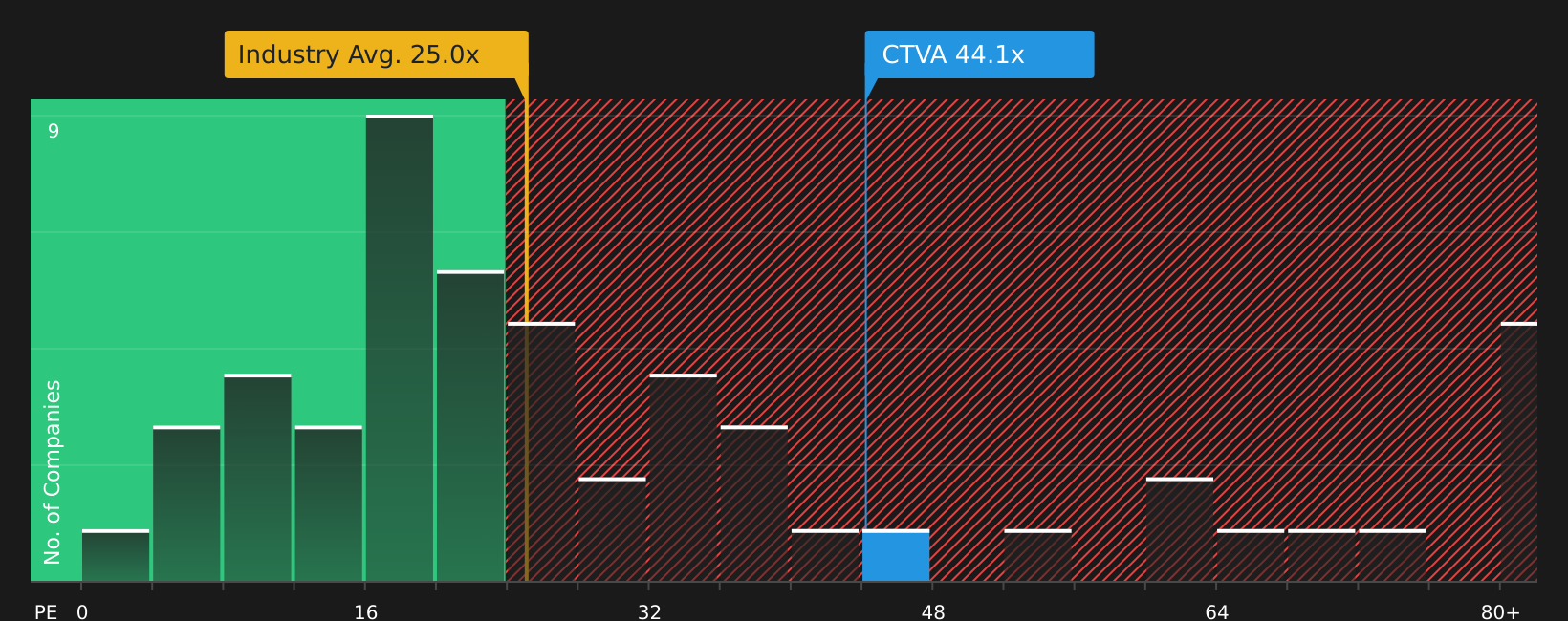

The fair value narrative points to a modest 3.7% upside, but the market is paying a much richer price on earnings today. Corteva trades on a P/E of 44.2x, compared with 24x for the US Chemicals industry and a 19.4x peer average, while its fair ratio sits at 26.2x.

That gap suggests investors are already paying a heavy premium for future progress. This raises the question: does this premium offer room for upside, or does it mostly add valuation risk if expectations slip?

Next Steps

Given the mixed signals on value, risk and recent momentum, it may be useful to act promptly and assess the narrative against the underlying data yourself. To see how the positives and pressure points compare side by side, take a close look at the 3 key rewards and 1 important warning sign

Looking for more investment ideas?

If Corteva has sharpened your focus, now is the moment to broaden your watchlist and line up a few more candidates before the crowd gets there.

- Target potential value opportunities by scanning 47 high quality undervalued stocks and see which stocks currently line up with stronger fundamentals and pricing support.

- Strengthen your downside protection by checking 70 resilient stocks with low risk scores so you are not missing companies with resilient business profiles and lower risk scores.

- Get ahead of the crowd by tracking screener containing 21 high quality undiscovered gems that combine quality metrics with less attention from the broader market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.