Corteva (CTVA) Valuation In Focus After PFAS Class Action Ruling Keeps Legal Risks In Play

Corteva Inc CTVA | 85.46 | +1.97% |

A recent Montana court decision has pushed a PFAS class action further along, keeping Corteva (CTVA) in the spotlight as investors weigh potential legal exposure alongside the company’s broader agriculture and crop input business.

The recent PFAS ruling arrives after a period where Corteva’s share price has shown positive momentum, including a 13.42% 90 day share price return and a 12.89% 1 year total shareholder return. The Etlas biofuels joint venture with bp adds a different kind of headline risk and opportunity for investors to weigh alongside ongoing legal exposure.

If this mix of legal and growth themes has you thinking more broadly about the sector, it could be a good moment to scan other agriculture and inputs names through healthcare stocks as potential complements or contrasts to Corteva.

With Corteva shares at $69.64, recent returns in the double digits, and the stock trading at a discount to the average analyst price target, investors may ask whether there is still upside potential or if future growth is already reflected in the current price.

Most Popular Narrative: 10.7% Undervalued

The most followed valuation narrative for Corteva pegs fair value at about US$77.95 per share, above the last close of US$69.64. This frames the current price against a detailed long term earnings path.

Expanding market penetration in high-growth regions, particularly Latin America and Asia-Pacific, with notable volume gains in Crop Protection and Seeds and anticipated gains from robust order books, supports above-market sales growth and more predictable long-term revenue and earnings trajectories.

Curious how steady revenue growth, rising margins and a richer product mix combine to justify that fair value? The narrative leans heavily on future earnings power and a premium earnings multiple. Want to see the full set of assumptions behind that view?

Result: Fair Value of $77.95 (UNDERVALUED)

However, this upbeat story could be tested if pricing pressure in Crop Protection or tighter environmental rules squeeze margins and challenge those long term profit assumptions.

Another Take: Multiples Paint A Richer Picture

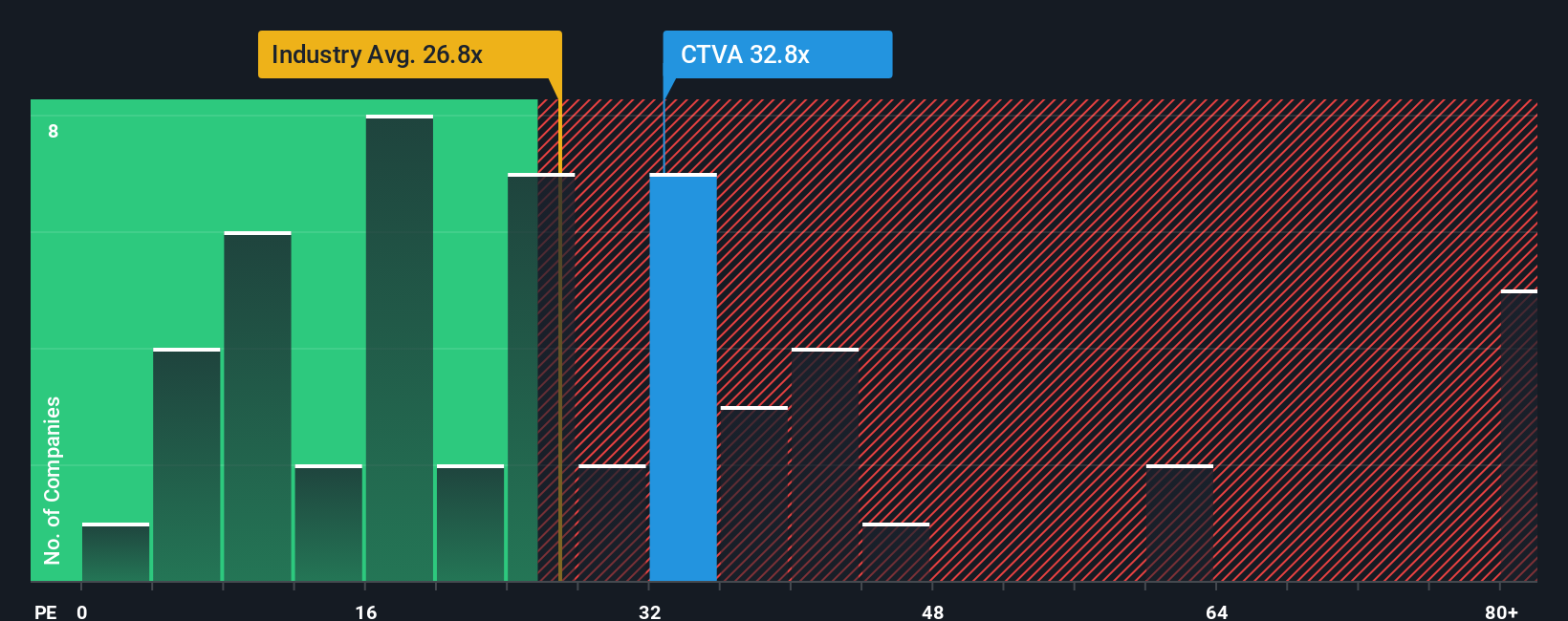

The popular undervaluation story sits uneasily next to Corteva’s current P/E of 28x. This screens as expensive versus the US Chemicals industry at 23.8x, peers at 15.2x, and even the fair ratio of 25.4x. If earnings do not keep pace with that premium, where does that leave the upside case?

Build Your Own Corteva Narrative

If you are not convinced by these narratives or prefer to weigh the numbers yourself, you can build a custom view in just a few minutes: Do it your way

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Corteva.

Looking for more investment ideas?

If Corteva has sharpened your interest, do not stop here. The Simply Wall St screener can quickly surface other opportunities that might fit your style and goals.

- Spot early stage potential by scanning these 3531 penny stocks with strong financials that pair small market caps with more established financial footing.

- Explore long term technology themes by checking these 24 AI penny stocks focused on artificial intelligence tied to real business models, not just hype.

- Look for potentially mispriced names using these 863 undervalued stocks based on cash flows, where valuations sit below cash flow based estimates, so you can decide which gaps look compelling.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.