Could Newmark Group’s (NMRK) RealFoundations Deal Mark a Turning Point in Recurring Revenues?

Newmark Group, Inc. Class A NMRK | 14.63 | -1.75% |

- Earlier this month, Newmark announced the acquisition of Dallas-based RealFoundations, a real estate consulting and managed services firm serving around 500 companies globally, expanding Newmark's Investor Solutions and Managed Services platform with advanced technology and workflow systems.

- This move, together with Newmark's advisory role in a US$4 billion AI data center joint venture and team expansions in European finance and data centers, highlights a concerted push into technology infrastructure and recurring revenue streams across major international markets.

- We'll explore how the RealFoundations acquisition sharpens Newmark's investment narrative, particularly its ambitions in recurring managed services revenue.

Find companies with promising cash flow potential yet trading below their fair value.

Newmark Group Investment Narrative Recap

To be a shareholder in Newmark Group, one needs to believe in the company's potential for sustained revenue and earnings growth through expansion into managed services, technology infrastructure, and global capital markets. The acquisition of RealFoundations supports this long-term recurring revenue focus but is not likely to materially impact the most important near-term catalyst: the ability to profitably scale new platforms. The main risk remains elevated costs and operational challenges tied to rapid global expansion, which could weigh on margins if integration targets are missed.

The recent strengthening of Newmark’s European debt, equity, and structured finance team is closely tied to the company’s ambitions around expanding cross-border deal flow and capturing growth in alternative asset classes, particularly in sectors like data centers. This hiring initiative directly supports the key catalyst of global platform buildout, which is meant to unlock further multi-year revenue and EBITDA growth potential. Yet the pace and complexity of integration remains...

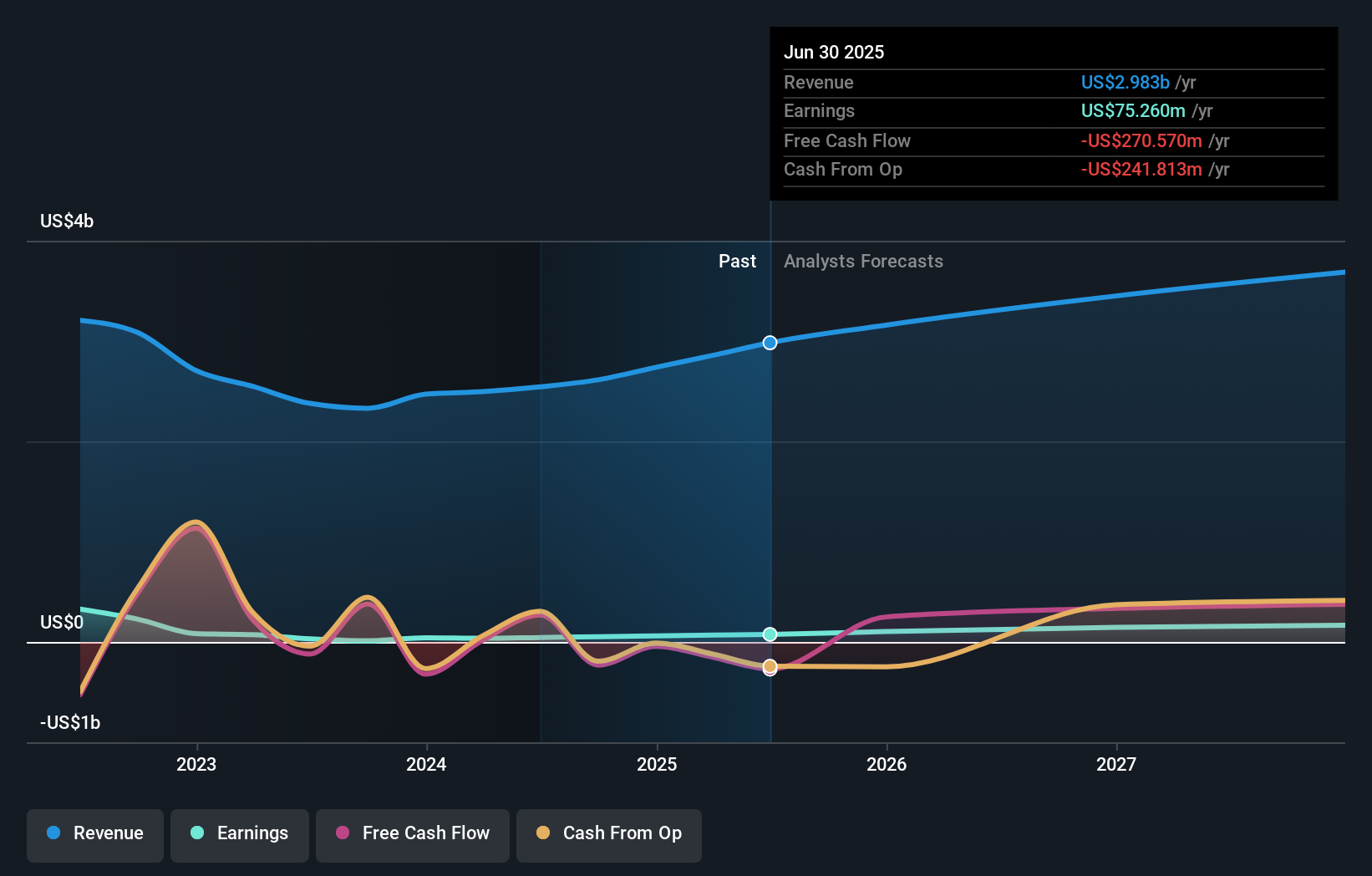

Newmark Group's narrative projects $3.8 billion in revenue and $201.7 million in earnings by 2028. This requires 8.2% yearly revenue growth and a $126.4 million earnings increase from current earnings of $75.3 million.

Uncover how Newmark Group's forecasts yield a $19.05 fair value, a 12% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community contributors currently value Newmark Group between US$11.81 and US$25.03, based on three independent analyses. With heightened integration risks from ongoing global expansion, your views on growth potential and profitability may differ sharply from others’, see how your thesis compares.

Explore 3 other fair value estimates on Newmark Group - why the stock might be worth 30% less than the current price!

Build Your Own Newmark Group Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Newmark Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Newmark Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Newmark Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Our top stock finds are flying under the radar-for now. Get in early:

- The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- These 10 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.