Cracker Barrel (CBRL) Stock Valuation After Surprise Q3 2026 Profit And Raised Guidance

Cracker Barrel Old Country Store, Inc. CBRL | 0.00 |

Cracker Barrel Old Country Store (CBRL) stock jumped after the company posted a surprise third quarter 2026 profit, raised its full year guidance, and pointed to improving guest satisfaction and cost control.

The strong Q3 surprise and raised guidance have arrived after a sharp share price rebound, with a 30 day share price return of 61.28% and a year to date share price return of 73.89%, even though the 1 year total shareholder return has declined 8.02%.

If Cracker Barrel's turnaround has your attention, it could be a good moment to broaden your watchlist and check out 20 top founder-led companies

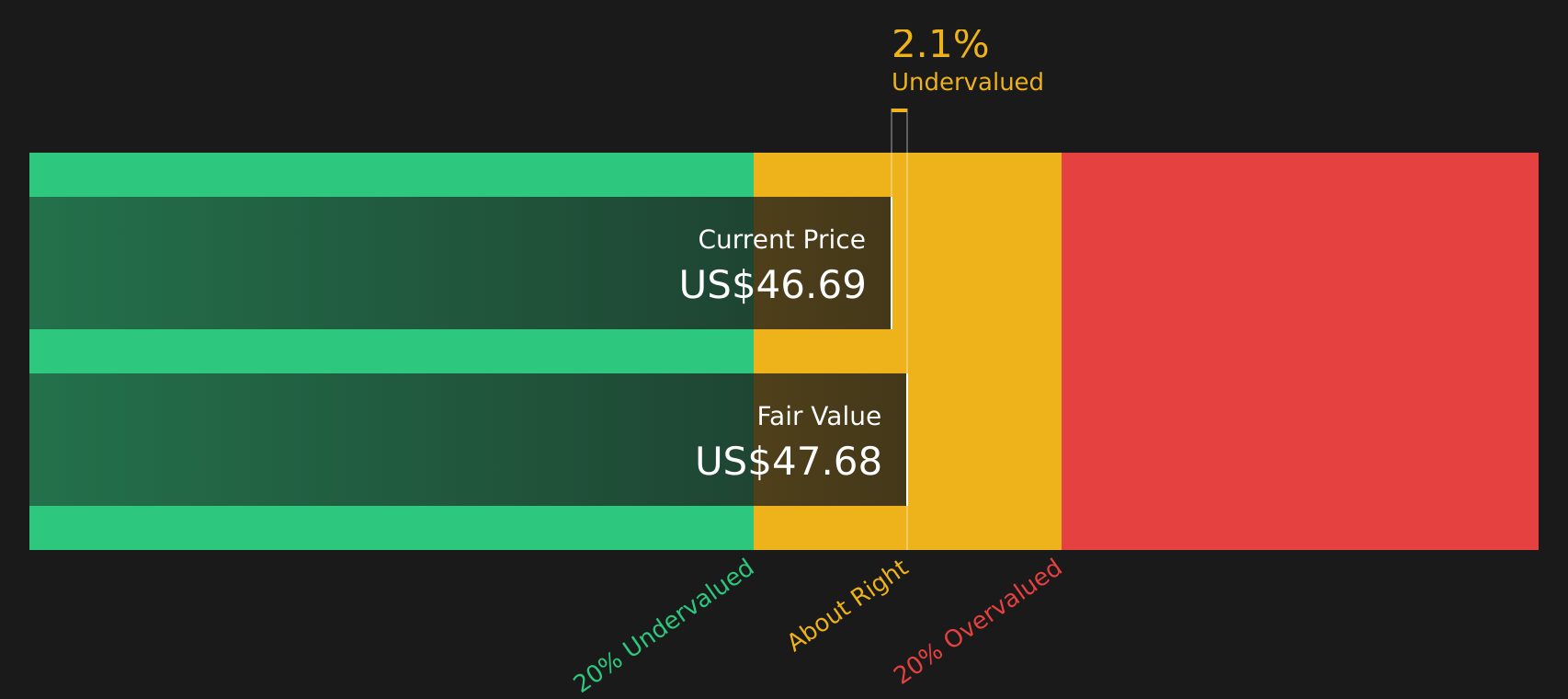

After a jump like that, you need to ask whether Cracker Barrel at about US$46.69 is now stretched, given its value score of 2 and a consensus price target near US$38, or if the turnaround still leaves a genuine buying opportunity that markets are not fully pricing in.

Most Popular Narrative: 48.8% Overvalued

At a last close of about $46.69 versus a narrative fair value near $31.38, the widely followed model implies investors are paying a steep premium for the turnaround story.

Cracker Barrel's remodel and refresh program, which remains in the test-and-learn phase, aims to significantly enhance store atmosphere and guest experience, potentially leading to increased foot traffic and higher sales, positively affecting revenue growth.

Want to see what is baked into that premium price tag? The narrative leans on gentle revenue progress, slimmer margins and a rich future earnings multiple. The exact mix of assumptions might surprise you. The full breakdown joins traffic, earnings and valuation into one tight story.

Result: Fair Value of $31.38 (OVERVALUED)

However, there is still a risk that softer traffic and consumer spending, as well as higher interest costs on refinancing US$300m of convertible debt, could undercut this upbeat turnaround story.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View: Cash Flows Tell a Softer Story

While the analyst narrative points to Cracker Barrel trading about 48.8% above the $31.38 fair value, the SWS DCF model paints a milder picture, with the stock at $46.69 sitting only about 1.1% below its estimated future cash flow value of $47.22. So which signal do you trust more: the earnings multiple or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cracker Barrel Old Country Store for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Uncertain about whether this upbeat tone really fits the full story? Take a closer look at the data now and shape your own view with 2 key rewards and 4 important warning signs

Looking for more investment ideas?

If Cracker Barrel has sharpened your focus, do not stop there. Use the Simply Wall Street Screener to quickly surface more focused ideas that match your style.

- Target potential bargains by zeroing in on companies that screen as 44 high quality undervalued stocks based on solid fundamentals and cash generation.

- Prioritize resilience by scanning for 70 resilient stocks with low risk scores that may offer steadier profiles when markets feel choppy.

- Get ahead of the crowd by searching through a screener containing 20 high quality undiscovered gems before they are widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.