Crane (CR) Valuation Check After Strong Earnings Guidance Upgrade And 11% Dividend Increase

Crane Company CR | 168.00 | -2.85% |

Crane (CR) drew fresh attention after reporting fourth quarter and full year 2025 results, issuing 2026 sales guidance that includes acquisition driven growth, and approving an 11% dividend increase alongside these announcements.

Despite the solid 2025 results, upbeat 2026 sales guidance and planned CEO transition, Crane’s recent share price performance has been mixed. The 1 day share price return was 1.82%, but the 7 day share price return showed a 12.93% decline, while the 1 year total shareholder return of 8.44% and very large 5 year total shareholder return suggest longer term momentum has been stronger than the latest pullback implies.

If earnings updates have you rethinking the sector, it could be a useful moment to scan other aerospace and defense stocks that share some of Crane’s end markets.

So with Crane trading at $182.64, showing strong recent earnings, an 11% higher dividend, and guidance for higher 2026 sales, is the current pullback an opening for buyers, or is the market already pricing in future growth?

Most Popular Narrative: 14.7% Undervalued

Crane's most followed narrative places fair value at $214.22, above the recent $182.64 share price, framing the current pullback against a richer long term outlook.

Crane's recent acquisition of PSI (Druck, Panametrics, Reuter-Stokes) positions the company to capture rising demand for advanced sensing and fluid control in both aerospace and process industries, directly benefiting from infrastructure modernization and growing automation supporting sustained revenue and future margin expansion.

Curious what it takes for that fair value to stack up? The narrative leans on faster revenue compounding, higher margins, and a future earnings multiple that assumes Crane continues to earn its way into a premium slot.

Result: Fair Value of $214.22 (UNDERVALUED)

However, this hinges on European chemical demand and smooth PSI integration, and setbacks in either could quickly challenge the growth, margin and P/E assumptions underpinning that fair value.

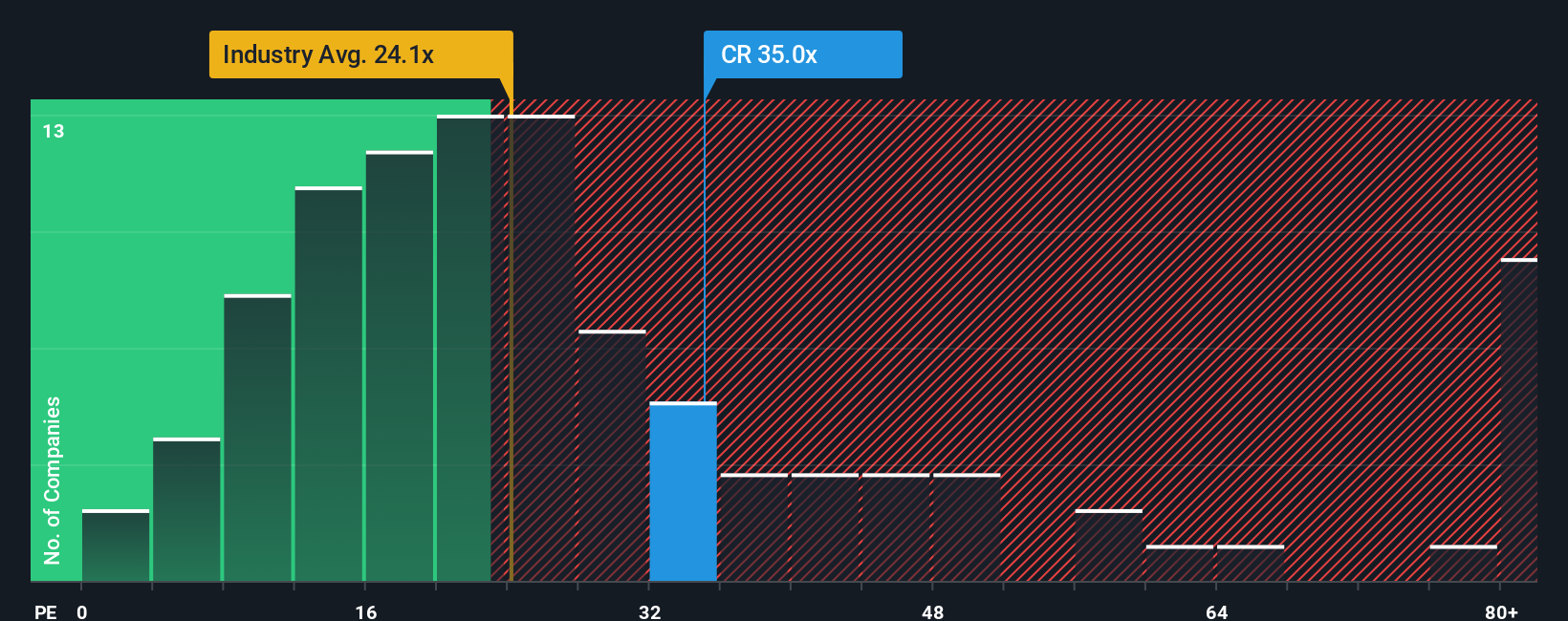

Another View: Rich P/E Signals A Full Price

While the narrative and our DCF work point to Crane being modestly undervalued at $182.64 versus a fair value of $185.78, the current P/E of 31.7x is higher than peers at 30.4x and above a fair ratio of 26.7x, which implies limited room for error if growth stumbles.

Build Your Own Crane Narrative

If you see the numbers differently, prefer your own research, or want to test another angle, you can build a custom view in minutes by starting with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Crane.

Ready for more investment ideas?

If Crane has you thinking differently about where you put your next dollar, consider lining up a few more ideas before the market moves.

- Spot potential high risk, high reward plays early by scanning these 3536 penny stocks with strong financials that already show stronger financial footing than many tiny peers.

- Explore the theme of automation and data by checking out these 24 AI penny stocks that are tied directly to real world applications.

- Focus on price versus fundamentals by reviewing these 888 undervalued stocks based on cash flows that currently screen as attractively priced based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.