Crescent Energy (CRGY) Is Up 5.2% After Record Q1 Output Amid Net Loss Expansion Has The Bull Case Changed?

Crescent Energy CRGY | 0.00 |

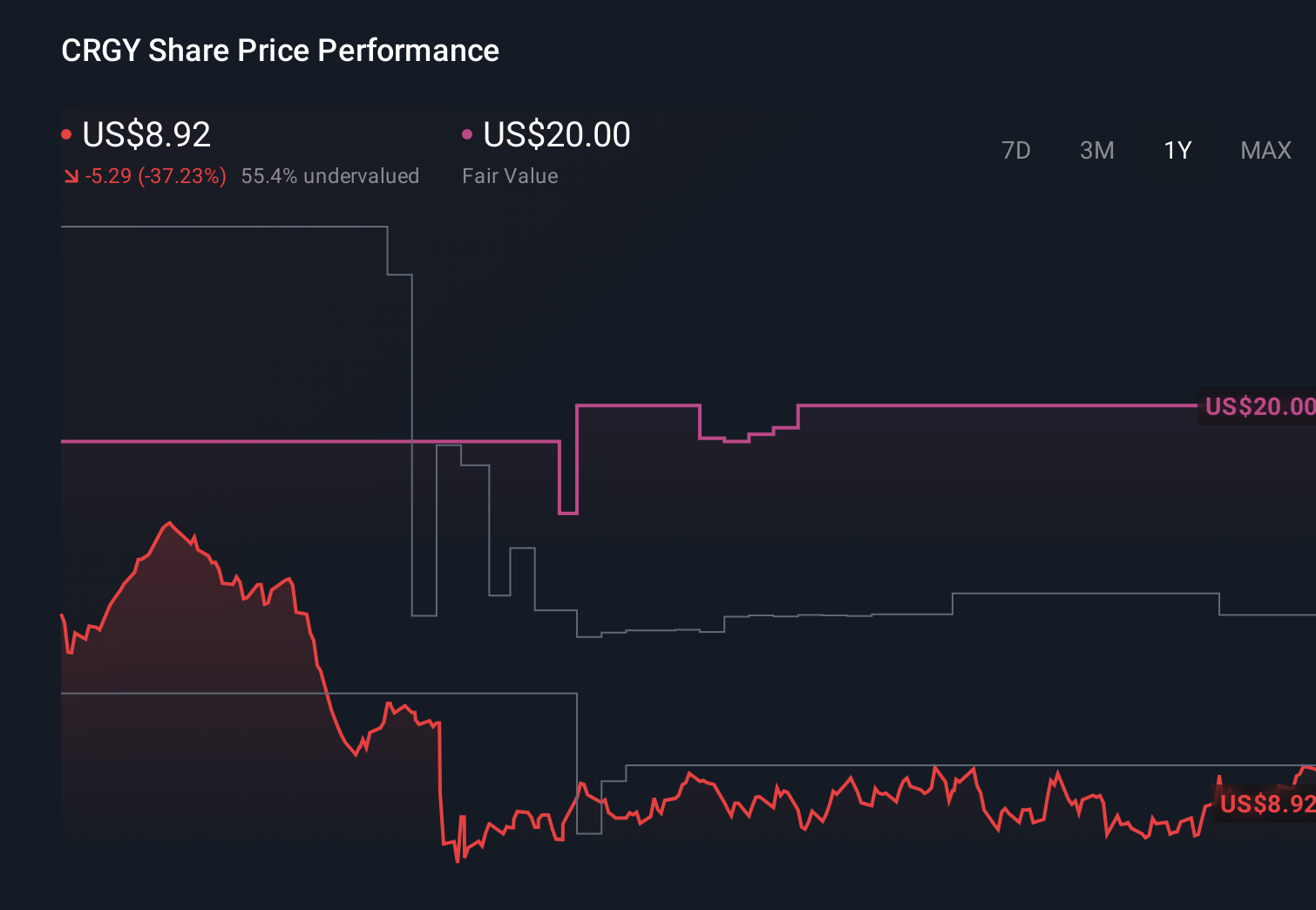

- Crescent Energy reported past first-quarter 2026 results with revenue of US$1,182.83 million and a net loss of US$419.85 million, while delivering record average production of 341 MBoe/d.

- Despite the larger loss, management emphasized record volumes, operational efficiency, and successful integration of newly acquired Permian assets as key drivers of the quarter’s operational outperformance.

- We’ll now examine how this record production and operational efficiency update affects Crescent Energy’s broader investment narrative and outlook.

Find 50 companies with promising cash flow potential yet trading below their fair value.

Crescent Energy Investment Narrative Recap

To own Crescent Energy, you need to be comfortable with a story built around scale, disciplined operations, and acquisition-driven growth, while accepting earnings volatility and integration risk. The Q1 2026 update reinforces the production and efficiency side of that thesis, but the larger net loss keeps the key near term catalyst focused on converting higher volumes into sustainable free cash flow. The biggest current risk remains that acquisition-heavy growth amplifies balance sheet pressure if cash generation lags.

Among recent announcements, the Q1 report that showed record average production of 341 MBoe/d is most relevant here, because it directly connects to expectations that Crescent can use operational efficiency and integration of Permian assets to support margins. However, the absence of share buybacks in early 2026, despite a still active authorization, may prompt some investors to watch even more closely how future cash flows are allocated between debt reduction, reinvestment, and potential capital returns.

Yet behind the record production and efficiency gains, there is a less visible risk investors should be aware of around Crescent’s dependence on acquisitions and the strain that could place on the balance sheet over time...

Crescent Energy's narrative projects $5.2 billion revenue and $672.6 million earnings by 2028.

Uncover how Crescent Energy's forecasts yield a $13.07 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming Crescent could grow revenue to about US$4.6 billion and earnings to roughly US$546.8 million by 2029, which is far more upbeat than consensus and puts Q1’s strong volumes but deep net loss in a different light, inviting you to compare these bolder expectations with the balance sheet and acquisition risks now in sharper focus.

Explore 4 other fair value estimates on Crescent Energy - why the stock might be worth just $13.07!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Crescent Energy research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Crescent Energy research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Crescent Energy's overall financial health at a glance.

Seeking Other Investments?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Capitalize on the AI infrastructure supercycle with our selection of the 42 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Neodymium and there are only 31 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.