CRH (NYSE:CRH) Valuation Check After Recent Share Price Swings

CRH public limited company CRH | 0.00 |

CRH (NYSE:CRH) is back in focus for investors after recent share price swings, with the stock showing a mix of short term declines and a gain over the past month.

At the latest share price of $114.44, CRH has a 1 month share price return of 12.48%, while the year to date share price return of 9.49% and 1 year total shareholder return of 23.76% suggest momentum has recently picked up after earlier weakness.

If you are comparing CRH with other materials and infrastructure names, it can be helpful to see what is moving alongside it by checking out 33 power grid technology and infrastructure stocks

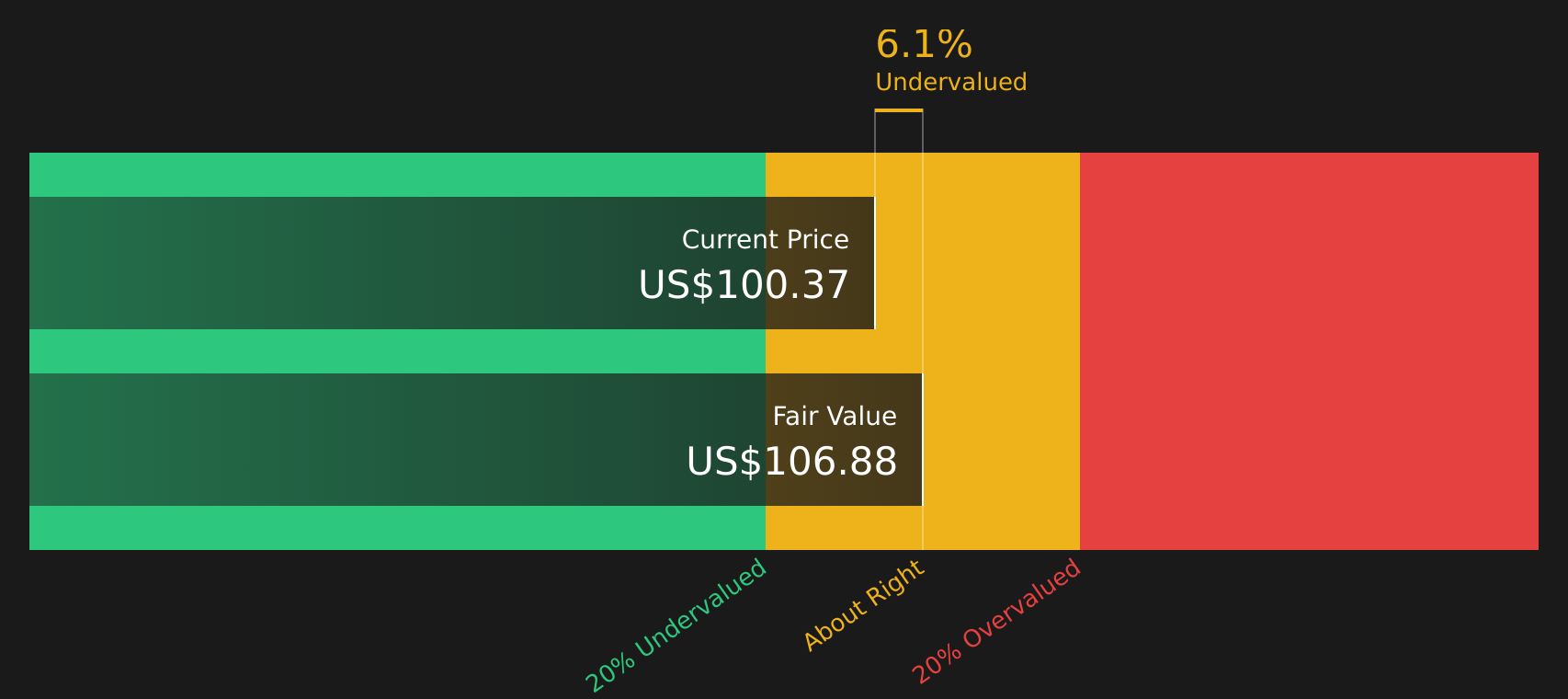

With CRH trading at $114.44, an intrinsic value estimate that sits at a 7.35% premium to the current price and a 24.92% discount to analyst targets raises a simple question: is this a genuine entry point, or is the market already pricing in future growth?

Most Popular Narrative: 19.9% Undervalued

With CRH at $114.44 and a narrative fair value of $142.95, the widely followed view is that the current price leaves meaningful upside on the table, built on specific expectations for future earnings and cash flows.

The ongoing rollout of U.S. federal infrastructure funding (less than 40% of the IIJA highway funds have been spent) and an encouraging outlook for the next highway bill create a substantial, multi-year runway for demand in CRH's core public infrastructure segments, offering the prospect for sustained revenue growth and backlog visibility. Acceleration in sustainable construction and decarbonization is catalyzing large investments into eco-friendly materials, exemplified by the Eco Material Technologies acquisition, uniquely positioning CRH to capture higher-margin business from the rapidly expanding supplementary cementitious materials market, benefiting both top-line growth and net margins amid market shifts toward green building.

Curious what kind of revenue path, margin profile, and future earnings multiple justify that higher fair value? The narrative leans on specific growth, profitability, and valuation assumptions that are not obvious from the share price alone.

Result: Fair Value of $142.95 (UNDERVALUED)

However, you still need to weigh the reliance on public infrastructure funding and the execution risk around large acquisitions like Eco Material, which could pressure margins.

Another View: Cash Flows Tell a Different Story

The popular narrative suggests CRH is 19.9% undervalued, but the SWS DCF model points the other way, with a future cash flow value of $106.60 versus the current $114.44. On this view, the stock screens as overvalued. Which story do you think fits the business better?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CRH for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment split between upside potential and valuation questions, it makes sense to check the numbers yourself and decide where you stand, then weigh both the 1 or more risks and 1 or more rewards that our analysis has highlighted by reviewing the 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

If CRH has your attention, do not stop there. The best portfolios come from comparing fresh ideas, pressure testing them, and acting before the crowd catches on.

- Spot potential mispricing by scanning 53 high quality undervalued stocks that combine quality fundamentals with attractive valuation signals.

- Strengthen your income stream by reviewing 14 dividend fortresses that aim to pair higher yields with resilient business models.

- Reduce portfolio stress by focusing on 72 resilient stocks with low risk scores that show sturdier balance sheets and more stable risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.