CrowdStrike (CRWD) Valuation Check After HSBC Upgrade And Renewed AI Security Optimism

CrowdStrike CRWD | 399.12 | +1.48% |

Recent analyst upgrades have pushed CrowdStrike Holdings (CRWD) back into focus, with HSBC’s move to a Buy rating highlighting refreshed confidence in its cloud-native, AI-driven security platform and its role in endpoint and identity protection.

The recent HSBC upgrade and news around partnerships with NordVPN and Aramco come after a mixed period for the stock. A 1 day share price return of 4.4% and a 7 day share price return of 8.63% contrast with a 30 day share price return decline of 5.34% and a 90 day share price return decline of 18.9%. At the same time, the 3 year total shareholder return of about 2.8x highlights how longer term holders have experienced a very different journey from those focused on recent volatility.

If you are looking beyond CrowdStrike and want more AI exposure, take a look at our screener of 57 profitable AI stocks that aren't just burning cash as a starting point for other ideas.

With HSBC highlighting an attractive entry point and the shares still trading at around a 20% intrinsic discount and roughly 28% below the average analyst target, you have to ask: is this a reset buying opportunity, or is the market already baking in years of AI driven growth?

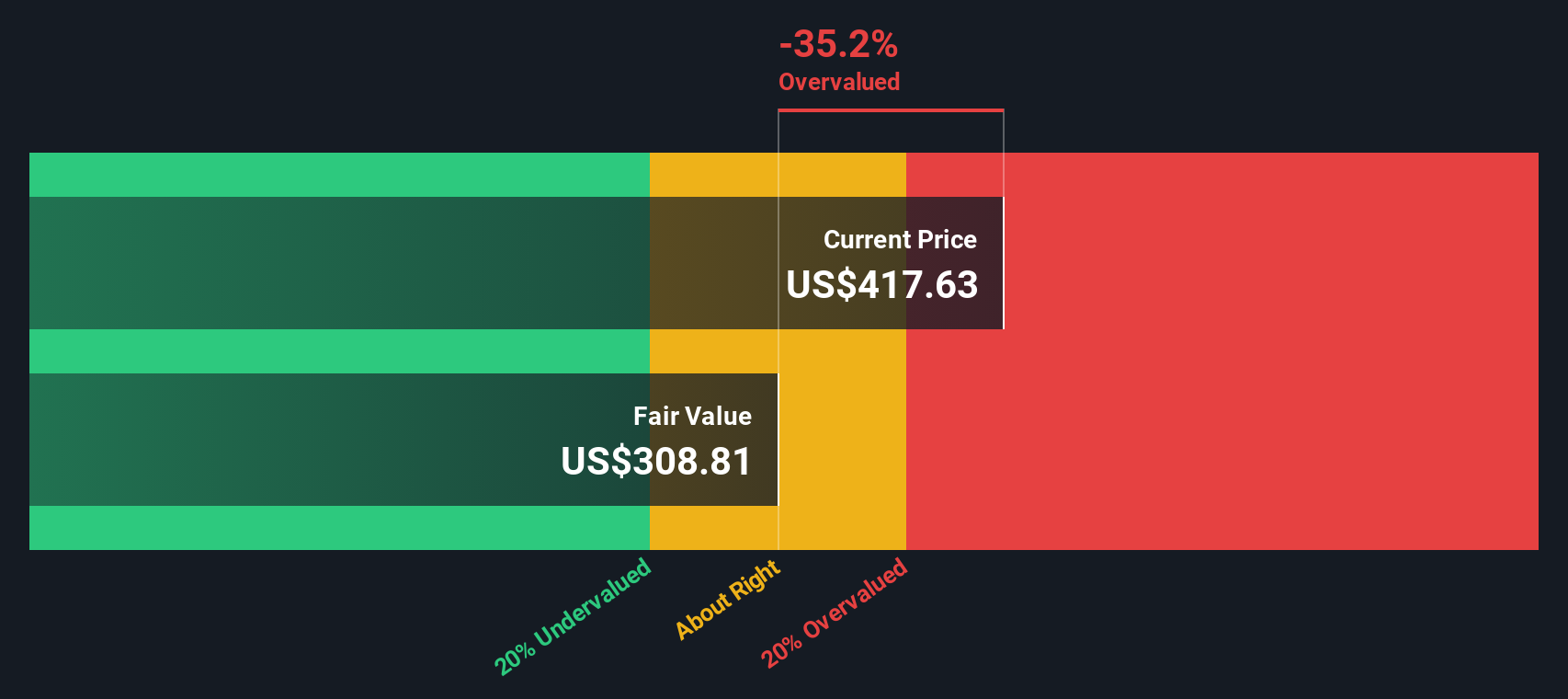

Most Popular Narrative: 32.5% Overvalued

Compared to the last close of $429.64, the most followed narrative pegs CrowdStrike Holdings at a fair value of $324.30, which frames the recent enthusiasm in a different light.

The company’s subscription revenues have been strong, accounting for 94.3% of total revenues in Q2 2024. Their Falcon Data Protection offering also presents attractive cross-sell opportunities.

Want to see what kind of growth story needs this kind of price tag? The narrative leans on aggressive revenue compounding, thick margins, and a rich future earnings multiple. Curious which specific assumptions sit under that overvaluation call? The full breakdown spells out every step behind that fair value line.

Result: Fair Value of $324.30 (OVERVALUED)

However, this hinges on bullish assumptions, and tougher competition or slower cybersecurity spending could quickly challenge that 32.5% overvaluation call.

Another Take: DCF Points the Other Way

That 32.5% overvaluation call sits awkwardly next to our DCF model, which puts fair value at $540.17 per share, compared with the current $429.64 price. In other words, the SWS DCF model suggests CrowdStrike is trading at a 20.5% discount. So which story do you trust more: cash flows or multiples?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out CrowdStrike Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own CrowdStrike Holdings Narrative

If you are not fully on board with these narratives or prefer to weigh the numbers yourself, you can build a customized view in just a few minutes, Do it your way.

A great starting point for your CrowdStrike Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If you stop with just one stock, you could miss other opportunities that better match your style, risk comfort, and income needs.

- Hunt for quality at a discount by scanning our list of 53 high quality undervalued stocks that pair solid fundamentals with more modest prices.

- Target resilience first by reviewing 84 resilient stocks with low risk scores that score well on financial strength and business stability.

- Spot early stage potential by checking our 29 elite penny stocks with strong financials that already show stronger balance sheets than many would expect in this corner of the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.