Cullen/Frost Bankers (CFR) Could Be 31% Undervalued Following Dividend And Earnings Optimism

Cullen/Frost Bankers, Inc. CFR | 0.00 |

Why Cullen/Frost Bankers Stock Is Back on Income Investors' Radar

Recent commentary around Cullen/Frost Bankers (CFR) has focused on its dividend profile, highlighting a yield above both its industry and the S&P 500, alongside consistent increases and a projected earnings uplift this fiscal year.

For income oriented investors, this mix of a higher-than-peer yield, a record of five dividend increases over five years, and an expected 6.45% year-over-year earnings improvement helps frame how the stock currently stacks up.

Cullen/Frost Bankers’ recent 3.12% 1 day share price return, a 5.39% 7 day gain, and an 11.77% 30 day share price return have added to its 27.58% year to date share price return and 21.67% 1 year total shareholder return, indicating that recent momentum has coincided with investors evaluating its income profile and earnings outlook.

If you are assessing how income ideas like Cullen/Frost Bankers fit alongside growth opportunities, it can be useful to see what else is moving in high quality banking and finance stocks and compare them with companies exposed to long term themes using tools such as the Simply Wall St screener for 18 top founder-led companies

For Cullen/Frost Bankers, the strong recent share price and income story could either be catching up with fundamentals or leaning on sentiment around the projected earnings uplift. How does the current valuation actually look?

Most Popular Narrative: 5.3% Overvalued

On the most followed narrative, Cullen/Frost Bankers' fair value of $155.36 sits below the recent $163.52 close, which puts the current income story against a slightly rich valuation backdrop using a 7.12% discount rate.

The analysts have a consensus price target of $155.36 for Cullen/Frost Bankers based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $168.0, and the most bearish reporting a price target of just $139.0.

The fair value narrative references steady revenue expansion, a modest step down in profit margins, and a richer future earnings multiple than the broader US banks sector. This raises the question of which specific growth and margin path is reflected in that outcome, and how much earnings power the narrative assumes Cullen/Frost Bankers will deliver by the end of the decade.

Result: Fair Value of $155.36 (OVERVALUED)

However, the Cullen/Frost Bankers narrative still hinges on branch expansion paying off as planned and on regional Texas concentration not exposing earnings to sharper local shocks.

Another View: Cullen/Frost Bankers Through a Cash Flow Lens

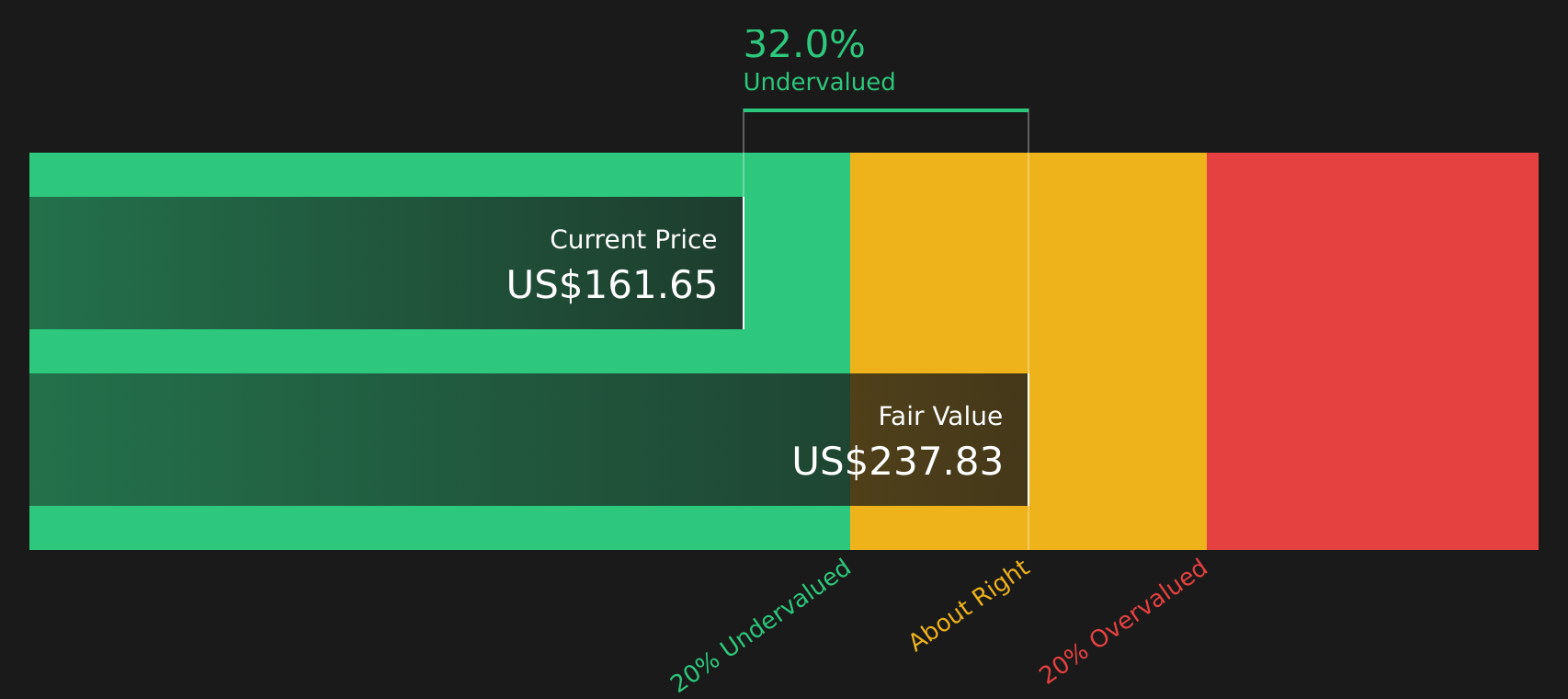

The analyst target of $155.36 presents Cullen/Frost Bankers as modestly overvalued, but the Simply Wall St DCF output points in the opposite direction. On this model, CFR at $163.52 trades about 31% below an estimated future cash flow value of $236.60, indicating a wide valuation gap. For investors, that split raises a basic question: which perspective on Cullen/Frost Bankers’ earnings power is more persuasive, the market’s multiple or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Cullen/Frost Bankers for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Given the mixed signals around Cullen/Frost Bankers, are you comfortable with where you stand or ready to pressure test that view against the data? If you want to move quickly and see what is driving optimism, start with the 3 key rewards.

Looking For More Investment Ideas Beyond Cullen/Frost Bankers?

If you only stop at Cullen/Frost Bankers, you could miss other stocks that fit your goals, diversify your income, and potentially strengthen your overall portfolio mix.

- Target steady potential by reviewing companies focused on income strength and capital discipline through the 8 dividend fortresses.

- Spot opportunities that combine quality with attractive pricing before they are widely followed using the screener containing 20 high quality undiscovered gems.

- Prioritise resilience by filtering for companies that carry lower risk profiles and more defensive characteristics with the 81 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.