Cushman And Wakefield (CWK) Stock Could Be 30% Undervalued After Its Annual Report

CUSHMAN & WAKEFIELD PLC CWK | 0.00 |

Cushman & Wakefield (CWK) is back in focus after investors revisited the stock following its latest annual report, which highlighted US$9.4b in 2024 revenue across services, leasing, capital markets, and valuation related lines.

At a share price of US$12.90, Cushman & Wakefield has seen short term pressure, with the 7 day share price return down 4.44%. However, the 90 day share price return of 5.13% and 1 year total shareholder return of 23.09% point to improving momentum over a longer window.

If this has you thinking about where else capital could work hard in real assets and infrastructure, it might be worth scanning 34 power grid technology and infrastructure stocks

With Cushman & Wakefield trading at US$12.90 despite an intrinsic value estimate implying a sizable discount, and with revenue growth accompanied by faster net income growth, investors now face the key question: is this a buying opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 30% Undervalued

The most followed Cushman & Wakefield narrative anchors fair value at $18.38 per share versus the last close of $12.90, which means a meaningful implied discount before even considering how that value is built up.

High client retention rates (notably 96% in Global Occupier Services) and expanding recurring services revenue, especially in facilities management, project management, and advisory, bolster earnings stability and support sustainable growth in net margins and cash flow.

Want to see what sits behind that Cushman & Wakefield valuation gap? The narrative leans heavily on recurring revenue, margin uplift, and a future earnings profile that looks very different to today. The key levers, and how hard they are pulled, only show up in the full set of assumptions.

Result: Fair Value of $18.38 (UNDERVALUED)

However, Cushman & Wakefield’s narrative could be tested if cyclical leasing and capital markets activity weakens, or if high debt levels start to restrict financial flexibility.

Another View on Cushman & Wakefield’s Valuation

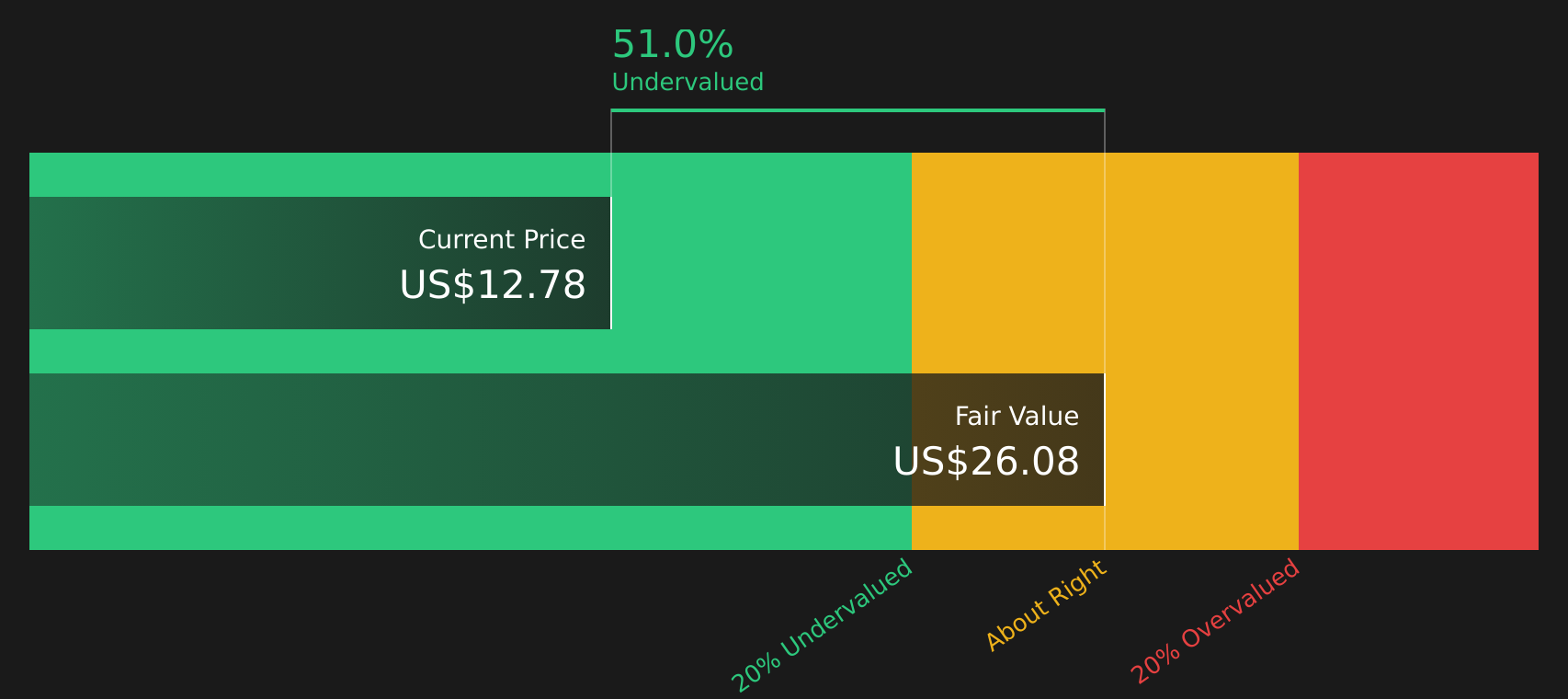

The first narrative around Cushman & Wakefield leans on discounted cash flows, with the stock trading at a 50.5% discount to an intrinsic value estimate of $26.08. On that view, CWK appears heavily undervalued, but it also assumes future cash generation and discount rates occur as modeled.

Our DCF model is only one lens, and it is sensitive to long term growth, margins and risk assumptions that may change as commercial real estate conditions evolve. For investors, the key question is how much weight to give this cash flow narrative compared with shorter term market signals.

Next Steps

Mixed on the Cushman & Wakefield story so far? Take a closer look at the data, weigh both the concerns and the upside, and check the 3 key rewards and 4 important warning signs

Looking for more investment ideas beyond Cushman & Wakefield?

Do not stop with Cushman & Wakefield; broaden your watchlist with fresh ideas from the Simply Wall St screener so your next opportunity does not pass you by.

- Target companies with compelling valuations by scanning 45 high quality undervalued stocks that may offer a stronger balance between quality, cash flows, and price.

- Prioritise resilience by reviewing 65 resilient stocks with low risk scores so potential downside is front of mind before you commit new capital.

- Hunt for tomorrow's standouts with the screener containing 19 high quality undiscovered gems that most investors may not yet be watching closely.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.