Deere (DE) Is Up 5.1% After US$99 Million Right-to-Repair Settlement Agreement With Farmers

Deere & Company DE | 592.42 | +0.33% |

- Earlier this month, Deere & Company agreed to a US$99.0 million class-action settlement over right-to-repair claims, pledging 10 years of expanded access to digital repair tools, manuals, and diagnostic software for farmers and independent service providers, subject to court approval and without any finding of wrongdoing.

- This settlement not only reduces legal uncertainty but also signals a shift in Deere’s approach to equipment repair access, which could reshape relationships with customers, dealers, and regulators.

- Next, we’ll examine how resolving the right-to-repair lawsuit and committing to broader repair access could influence Deere’s longer-term investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Deere Investment Narrative Recap

To own Deere, you need to believe that its mix of high tech equipment, precision farming tools and financing can stay relevant even as cycles and tariffs bite into demand. The right to repair settlement looks manageable financially, but it could matter for the biggest near term risk: margin pressure from pricing, incentives and higher costs if repair revenue or dealer economics are affected.

The most relevant recent announcement here is Deere’s raised full year 2026 net income guidance to US$4.5 billion to US$5.0 billion, which came alongside stronger construction and small ag demand. That improved outlook sits in tension with ongoing tariff, input cost and North American large ag headwinds, and the new repair access commitments may subtly influence how investors think about Deere’s pricing power and long term earnings quality.

Yet behind these positives, investors should be aware that competitive pricing pressure and high equipment costs could still...

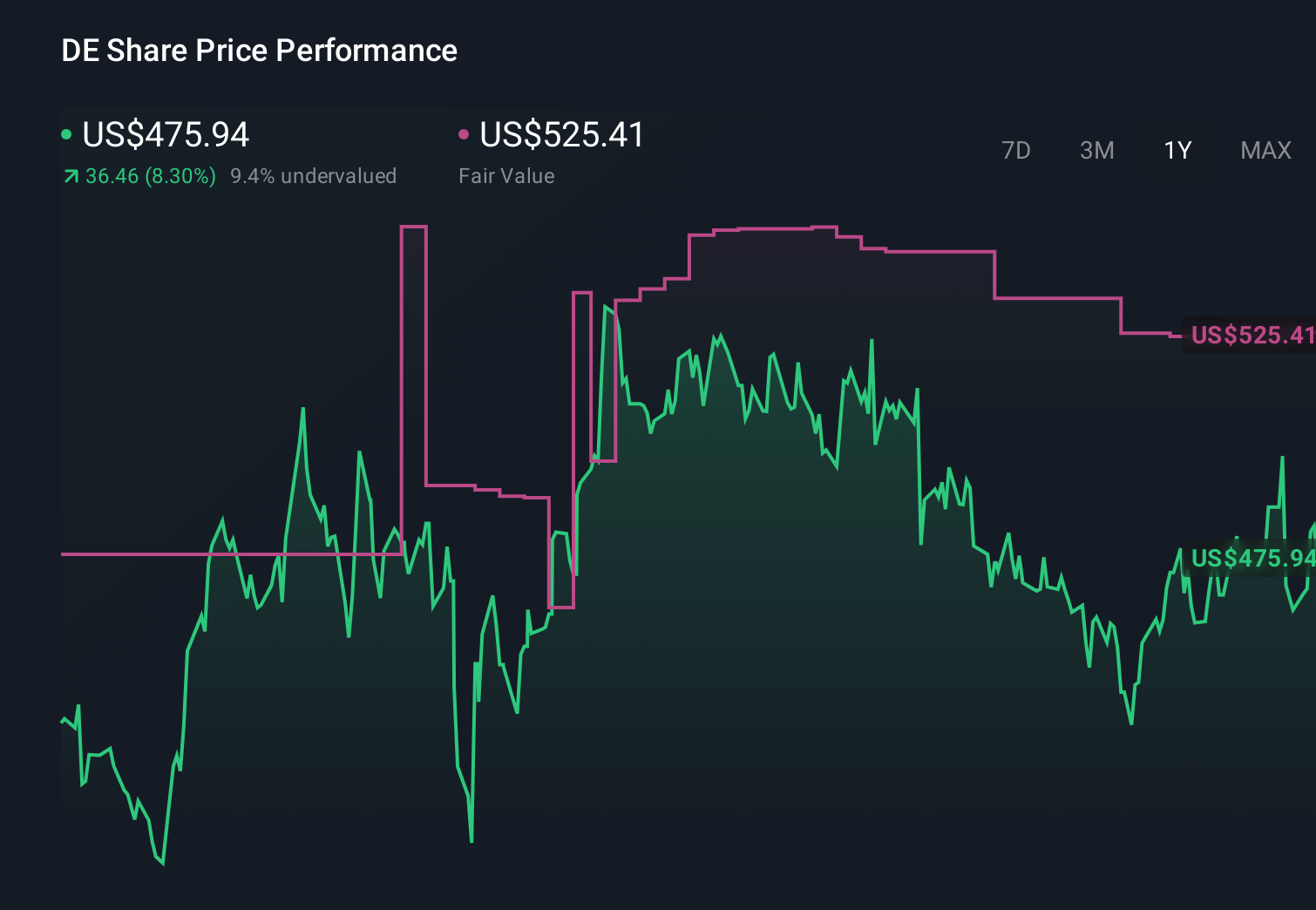

Deere's narrative projects $47.6 billion revenue and $8.4 billion earnings by 2029. This requires fairly flat yearly revenue growth and a $3.6 billion earnings increase from $4.8 billion today.

Uncover how Deere's forecasts yield a $664.01 fair value, a 10% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming roughly flat revenue near US$45.6 billion by 2029 and needing higher margins to justify US$6.1 billion in earnings, so it is worth asking whether the right to repair settlement and repair access commitments pull Deere closer to that more pessimistic view or help support the stronger precision tech story instead.

Explore 4 other fair value estimates on Deere - why the stock might be worth as much as 14% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Explore 24 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

- Rare earth metals are the new gold rush. Find out which 27 stocks are leading the charge.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.