Del Monte (DMC) Following Treatt Partnership Has Valuation Back In Focus

Del Monte Corporation DMC | 0.00 |

Del Monte (DMC) has partnered with Treatt to launch a new line of upcycled fruit-derived extracts for beverage makers, using pineapple, watermelon, mango and cantaloupe materials from its processing operations.

That upcycled extracts launch comes as Del Monte’s 1 day share price return of 3.65% and 7 day return of 3.91% contrast with a weaker 90 day return. The 3 year total shareholder return of 26.34% also highlights a different picture than the more recent 1 year result.

If you are considering where else product driven stories could emerge, it may be worth broadening your watchlist with the 19 top founder-led companies

So is this recent bounce in Del Monte simply traders warming back up after a weaker 90 day stretch, or does it better reflect how the core business and earnings profile are being valued at today’s price?

Most Popular Narrative: 44.2% Undervalued

Analysts see Del Monte’s fair value at $52 per share versus a last close of $29, which sets up a clear narrative gap for investors to unpack.

Strong recent pricing and ongoing global consumer demand for pineapples (especially premium and proprietary varieties) have supported robust sales and margin expansion. However, the current industry-wide supply shortage, driven by weather disruptions and crop disease, could be interpreted by investors as a sustainable tailwind and may lead to overestimation of future revenue growth and net margin resilience once supply gradually normalizes.

Curious what sits behind that $52 fair value for Del Monte? The narrative focuses on a specific revenue ramp, margin rebuild, and a tighter future earnings multiple. The full story connects those assumptions into one pricing roadmap.

Result: Fair Value of $52 (UNDERVALUED)

However, there are still meaningful risks for Del Monte, including climate and disease threats to pineapple and banana supply, as well as rising compliance and logistics costs that are pressuring margins.

Another View on Del Monte’s Valuation

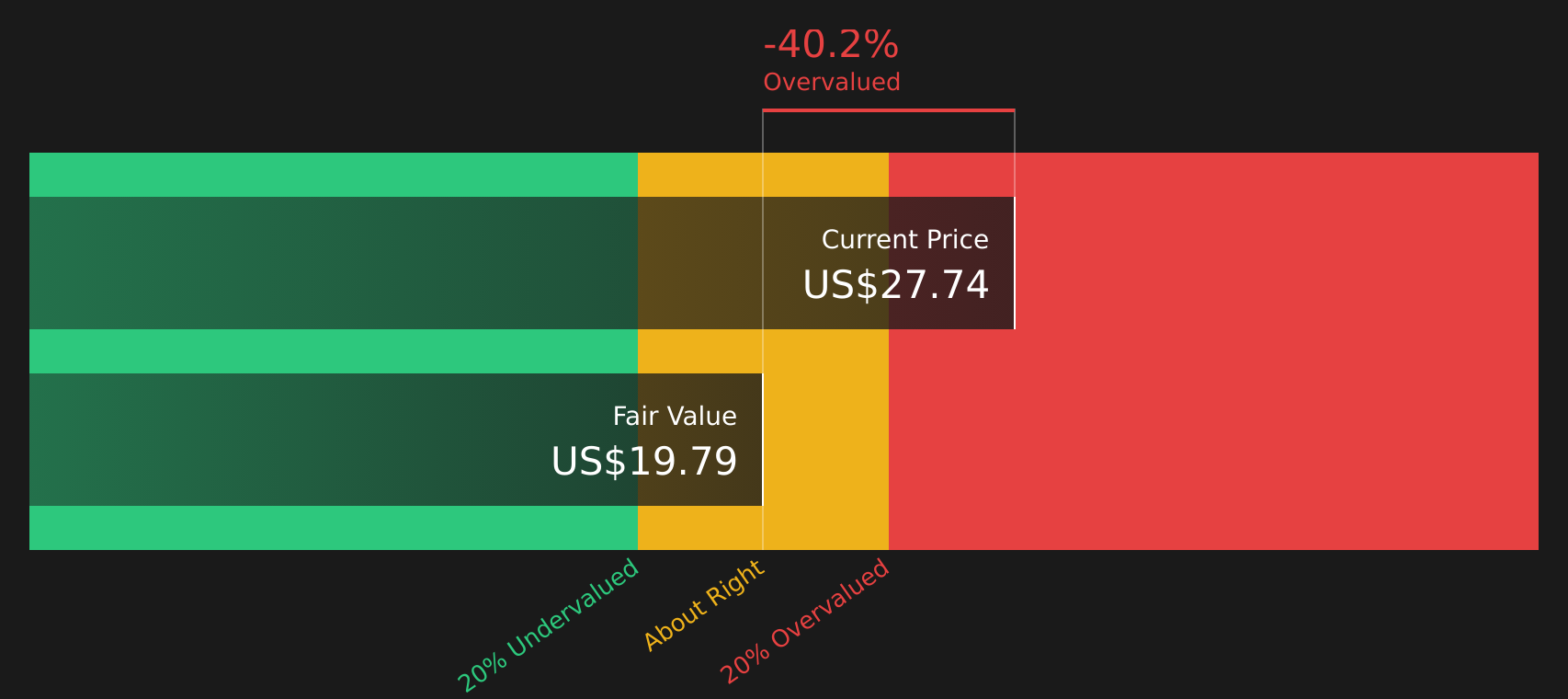

The analyst fair value of $52 for Del Monte leans on earnings forecasts and an assumed future P/E of 12.7x, yet the SWS DCF model points to a future cash flow value of $19.79 with the current price at $29. If cash flows matter more than multiples in this context, how comfortable are you with that gap?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Del Monte for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

The mix of optimism and concern around Del Monte is clear. Take a moment to review the data, pressure test the assumptions, and then weigh up the 1 key reward and 3 important warning signs.

Looking for more investment ideas beyond Del Monte?

If you like the story around Del Monte but want a wider set of options, use the Simply Wall St Screener to spot other opportunities that fit your style.

- Spot potential bargains early by scanning 45 high quality undervalued stocks that pair solid fundamentals with prices that may not fully reflect their financial profile.

- Strengthen your core holdings with companies from the solid balance sheet and fundamentals stocks screener (47 results) that focus on resilience and financial discipline.

- Hunt for under-the-radar stories using the screener containing 18 high quality undiscovered gems before they sit squarely on every investor’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.