Did Chipotle’s (CMG) Aggressive Expansion Amid Softer Same-Store Sales Just Recast Its Growth Trade-Offs?

Chipotle Mexican Grill, Inc. CMG | 33.16 | +1.62% |

- In recent months, Chipotle Mexican Grill has continued to open new restaurants and pursue menu, loyalty, and operational initiatives, even as same-restaurant sales last year fell 1.7% amid weaker customer traffic and broader macroeconomic pressures.

- This combination of aggressive expansion to more than 4,000 locations and a price-to-earnings ratio below the sector average has sharpened investor focus on how effectively Chipotle can convert its growth plans into resilient performance.

- Next, we’ll examine how Chipotle’s ongoing store expansion, despite recent same-restaurant sales pressure, reshapes the company’s broader investment narrative and risks.

Rare earth metals are the new gold rush. Find out which 30 stocks are leading the charge.

Chipotle Mexican Grill Investment Narrative Recap

To own Chipotle today, you need to believe its rapid new store growth and menu, loyalty, and operational efforts can offset recent 1.7% same-restaurant sales pressure and softer traffic. The key short term catalyst is whether new units and initiatives stabilize comparable sales, while the biggest risk remains that weaker consumer spending and traffic trends persist. The latest update on expansion and valuation sharpens, but does not fundamentally change, that near term risk reward focus.

Among recent announcements, Chipotle’s guidance for roughly flat 2026 comparable restaurant sales is particularly relevant. It frames expectations for how quickly new restaurants, menu innovation, and loyalty programs might translate into steadier transaction trends after last year’s decline, while also reminding investors that any prolonged consumer pullback or competitive intensity could leave comps subdued even as the store count keeps rising.

Yet behind the appealing growth story, there is still the underappreciated risk that sustained macro pressure and softer traffic could...

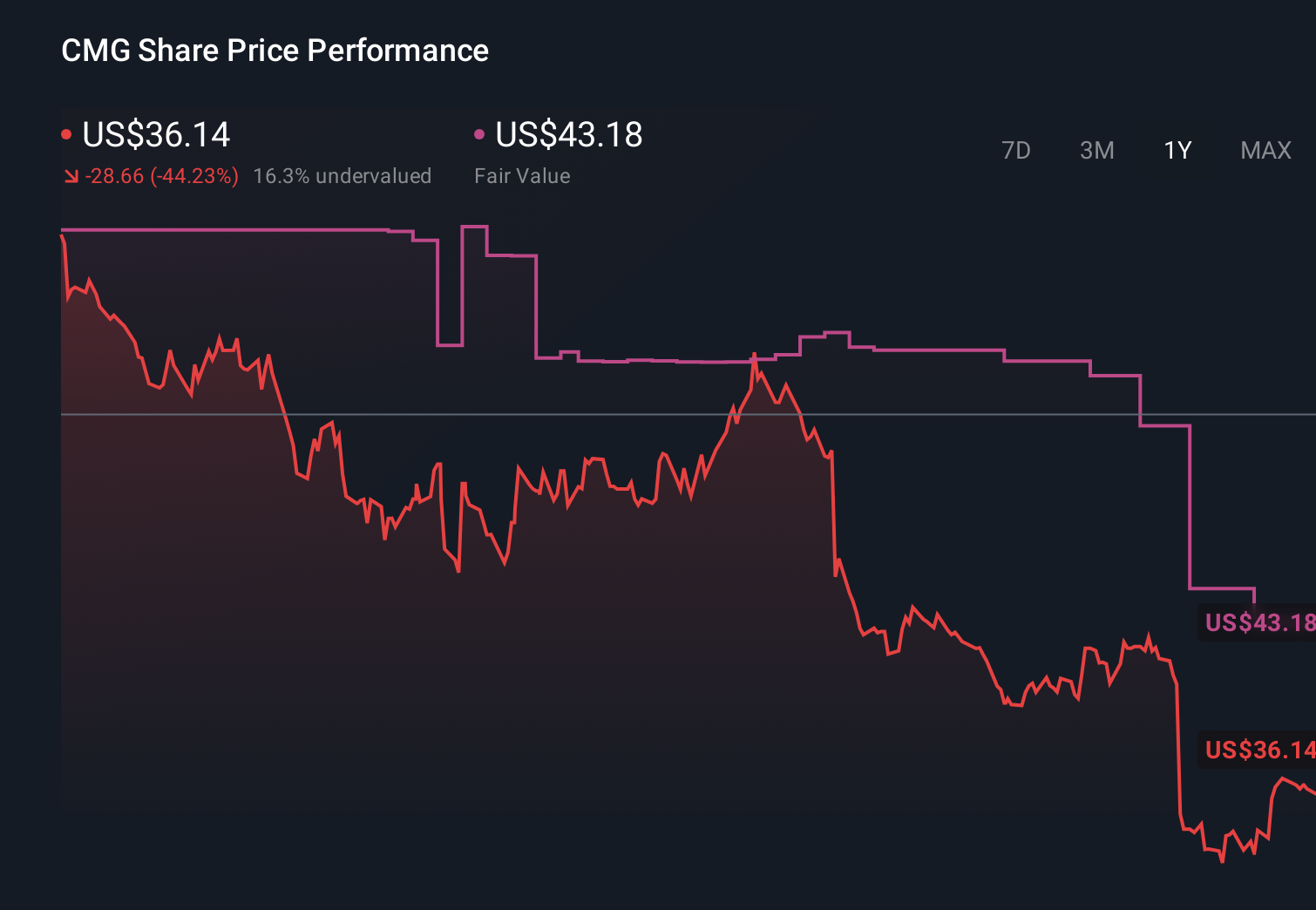

Chipotle Mexican Grill's narrative projects $16.4 billion revenue and $2.3 billion earnings by 2028. This requires 12.3% yearly revenue growth and about a $0.8 billion earnings increase from $1.5 billion today.

Uncover how Chipotle Mexican Grill's forecasts yield a $44.24 fair value, a 18% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$17.1 billion and earnings US$2.2 billion by 2028, which is far more upbeat than consensus and puts a very different spin on risks like whether younger, value conscious diners keep shifting toward eating at home.

Explore 19 other fair value estimates on Chipotle Mexican Grill - why the stock might be worth as much as 49% more than the current price!

Form Your Own Verdict

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Chipotle Mexican Grill research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Chipotle Mexican Grill research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Chipotle Mexican Grill's overall financial health at a glance.

Looking For Alternative Opportunities?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Uncover the next big thing with 32 elite penny stocks that balance risk and reward.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.