Did Deere’s (DE) New Omnibus Shelf Plan Quietly Redefine Its Capital Raising Playbook?

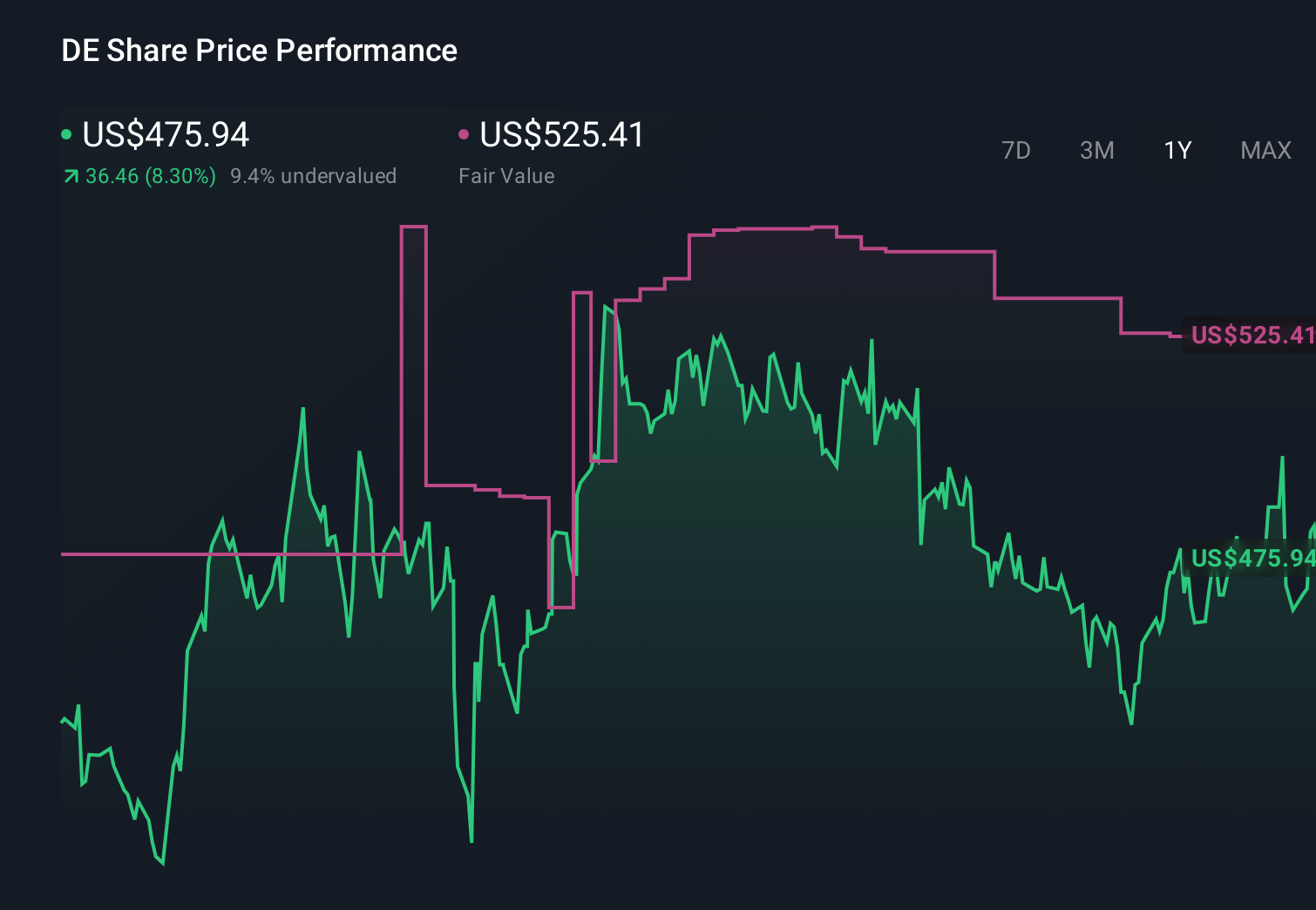

Deere & Company DE | 0.00 |

- Earlier this month, Deere & Company filed an omnibus shelf registration that covers a wide range of securities, including debt, preferred and common stock, depositary shares, multiple types of warrants, and stock purchase contracts and units.

- This broad financing toolkit, combined with rising analyst earnings estimates and revenue forecasts, highlights how Deere is positioning itself for flexible capital raising as its business outlook evolves.

- Next, we’ll examine how the stronger earnings expectations reflected in recent analyst revisions could reshape Deere’s existing investment narrative.

Capitalize on the AI infrastructure supercycle with our selection of the 49 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Deere Investment Narrative Recap

To own Deere, you have to believe in long term demand for high tech farm and construction equipment and the company’s ability to protect margins despite tariffs, volatile North American ag demand, and aggressive pricing from rivals. The new omnibus shelf registration itself does not materially change those big drivers or the near term risk that elevated incentives and financial services support could weigh on future revenue quality if underlying demand softens further.

What does stand out alongside the shelf filing is how analyst earnings estimates and revenue forecasts have been ticking higher in recent weeks. This growing optimism lines up with Deere’s raised full year 2026 net income guidance to US$4.5 billion to US$5.0 billion and its recent Q2 results, where revenue increased year over year even as net income dipped, reinforcing the idea that higher value precision technology and services remain a key potential catalyst.

But even with this brighter outlook, investors should watch the risk that heavier use of incentives and John Deere Financial could eventually pressure margins and credit quality...

Deere's narrative projects $48.4 billion revenue and $9.3 billion earnings by 2029. This requires fairly flat yearly revenue growth and an earnings increase of about $4.5 billion from $4.8 billion today.

Uncover how Deere's forecasts yield a $644.21 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some analysts took a far more optimistic view before this shelf news, assuming Deere could lift earnings to about US$10.3 billion and nearly double margins, which contrasts sharply with the more cautious concerns about tariff and ag cycle risks and shows how widely your view of Deere’s future can differ from others.

Explore 3 other fair value estimates on Deere - why the stock might be worth as much as 12% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Deere research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Deere research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Deere's overall financial health at a glance.

Looking For Alternative Opportunities?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 7 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 14 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.