Did Everus Construction Group's Broad Russell Growth Index Addition Just Shift Everus Construction Group's (ECG) Investment Narrative?

Everus Construction Group, Inc. ECG | 0.00 |

- On 27 June 2026, Everus Construction Group, Inc. (NYSE: ECG) was added to multiple Russell growth benchmarks, including the Russell 1000 Growth, 2500 Growth, 3000 Growth, 3000E Growth, Small Cap Comp Growth, and Midcap Growth indices.

- This broad inclusion across the Russell growth family can increase ECG’s visibility with institutional investors and index-linked funds that track these benchmarks.

- We’ll now explore how Everus Construction Group’s broad addition to Russell growth indices may influence its investment narrative and longer-term positioning.

Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

Everus Construction Group Investment Narrative Recap

To own Everus, you have to believe that demand for complex power and data center infrastructure can support healthy earnings while execution risks and a relatively new leadership team are managed. The broad addition to Russell growth indices may lift trading liquidity in the near term, but it does not materially change the key near term catalyst of data center and T&D project flow, nor the biggest risk around sustaining backlog and margins as execution tailwinds normalize.

The Russell inclusions land just weeks after Everus raised its 2026 revenue outlook to US$4.3 billion to US$4.4 billion on the back of strong Q1 results and the SE&M acquisition. That guidance increase sharpened focus on whether recent revenue and earnings strength can be repeated without stretching capital deployment or project execution. Index inclusion now adds an additional attention point around how effectively Everus converts that higher visibility into durable, high quality growth.

Yet against this stronger visibility, investors should still be mindful of how lumpier data center demand could affect Everus’ earnings momentum and backlog resilience over time...

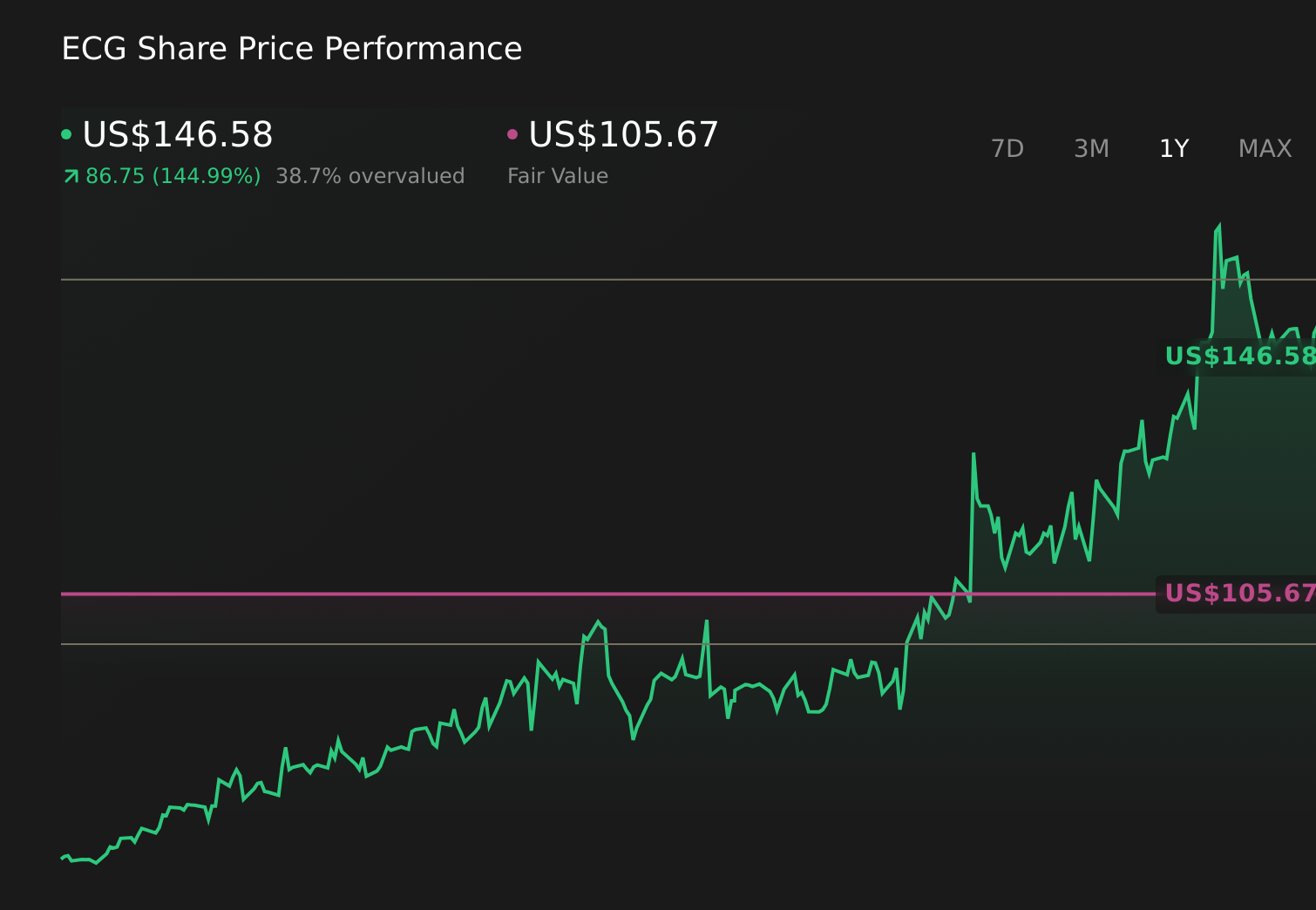

Everus Construction Group's narrative projects $4.3 billion revenue and $220.5 million earnings by 2028. This requires 7.2% yearly revenue growth and a $39.5 million earnings increase from $181.0 million today.

Uncover how Everus Construction Group's forecasts yield a $105.67 fair value, a 24% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts were already cautious, assuming revenue of about US$5.1 billion and earnings of roughly US$305 million by 2029, which contrasts with the backlog strength and margin resilience that could, in light of the new Russell index attention, lead you to reassess how much execution and capex risk you are really pricing in.

Explore 4 other fair value estimates on Everus Construction Group - why the stock might be worth as much as 22% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Everus Construction Group research is our analysis highlighting 5 key rewards that could impact your investment decision.

- Our free Everus Construction Group research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Everus Construction Group's overall financial health at a glance.

Searching For A Fresh Perspective?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find 44 companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.