Did Mixed Wall Street Caution and Contrarian Interest Just Shift MercadoLibre's (MELI) Investment Narrative?

MercadoLibre, Inc. MELI | 0.00 |

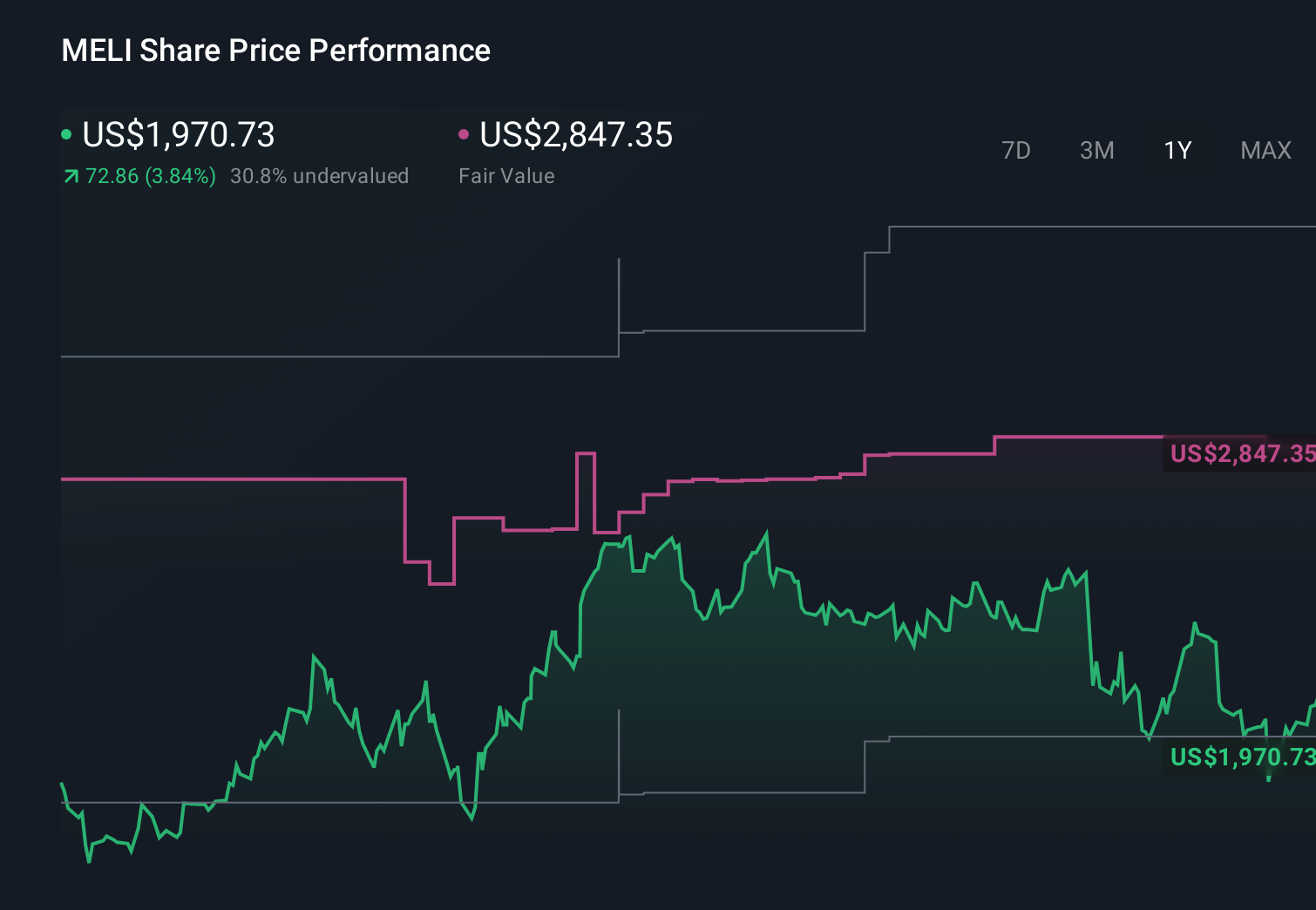

- In mid-May 2026, MercadoLibre drew mixed reactions as major banks flagged margin and monetization pressures while prominent market commentators highlighted it as a contrarian opportunity amid weak retail sentiment and evidence of institutional accumulation.

- This contrast between cautious analyst views and growing interest from professional investors and media voices has sharpened the debate over MercadoLibre’s long-term role in Latin American e-commerce and fintech.

- Now we’ll examine how rising contrarian interest and institutional accumulation could influence MercadoLibre’s pre-existing investment narrative and risk profile.

The latest GPUs need a type of rare earth metal called Terbium and there are only 31 companies in the world exploring or producing it. Find the list for free.

MercadoLibre Investment Narrative Recap

To own MercadoLibre, you have to believe its dual e commerce and fintech ecosystem can keep compounding in Latin America despite intensifying margin and monetization pressure. The latest JPMorgan and Citi downgrades point to take rate and profitability headwinds that may weigh on the key near term catalyst of operating leverage. At the same time, evidence of institutional accumulation suggests the core long term thesis is intact, so the short term impact on the overall narrative looks limited so far.

The most relevant recent data point is Q1 2026, where revenue rose to US$8,845 million while net income declined to US$417 million. That combination of strong top line growth and softer profitability fits directly with the banks’ concerns about margin pressure and monetization, and it is central to how investors frame both the upside from MercadoLibre’s expansion and the risk that rising costs and lower take rates could weigh on results if conditions stay tight.

Yet beneath the growth story, investors should be aware that rising credit exposure and thinner margins could quickly become more important if...

MercadoLibre's narrative projects $57.9 billion revenue and $4.8 billion earnings by 2029. This requires 26.1% yearly revenue growth and a $2.8 billion earnings increase from $2.0 billion today.

Uncover how MercadoLibre's forecasts yield a $2440 fair value, a 44% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already expecting revenue of about US$59.3 billion and earnings of US$3.5 billion by 2029, which paints a far more cautious picture than the consensus and highlights how sharply opinions can differ, especially when fresh concerns about margins and competition emerge and may still reshape both the bullish and bearish cases.

Explore 25 other fair value estimates on MercadoLibre - why the stock might be worth as much as 94% more than the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your MercadoLibre research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free MercadoLibre research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate MercadoLibre's overall financial health at a glance.

Seeking Other Investments?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- AI is about to change healthcare. These 37 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 88 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.