Did Paychex’s (PAYX) 10% Dividend Hike Amid Firm Job Trends Just Reframe Its Stability Story?

Paychex, Inc. PAYX | 0.00 |

- In early May 2026, Paychex, Inc. raised its regular quarterly cash dividend to US$1.19 per share, a US$0.11 (10%) increase from the prior US$1.08, payable on May 29, 2026 to shareholders of record on May 13, 2026.

- Around the same time, the company’s Small Business Employment Watch showed a second straight month of improving U.S. small-business job growth, highlighting resilience in Paychex’s core client base.

- Next, we’ll examine how this 10% dividend increase could influence Paychex’s investment narrative, especially around cash returns and perceived stability.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 33 best rare earth metal stocks of the very few that mine this essential strategic resource.

Paychex Investment Narrative Recap

To own Paychex, you need to believe in steady demand for outsourced HR and payroll, supported by a broad small business client base and consistent cash generation. The 10% dividend hike and improving Small Business Employment Watch data both lean toward the same near term catalyst: confidence in cash returns to shareholders. The biggest current risk, in my view, is still macro uncertainty around small business hiring and hours worked, and this news does not remove that.

Among recent announcements, the Q3 2026 results stand out alongside the dividend increase. Paychex reported US$1,808.9 million in quarterly revenue and US$560.3 million in net income, while also lifting its regular dividend to US$1.19 per share. Together with ongoing buybacks, this reinforces the theme that a large part of the investment case today rests on disciplined capital returns and the company’s ability to sustain them if employment conditions soften again.

Yet against the appeal of a higher dividend and solid cash flows, investors should still be aware of the risk that small business hiring and hours could weaken again...

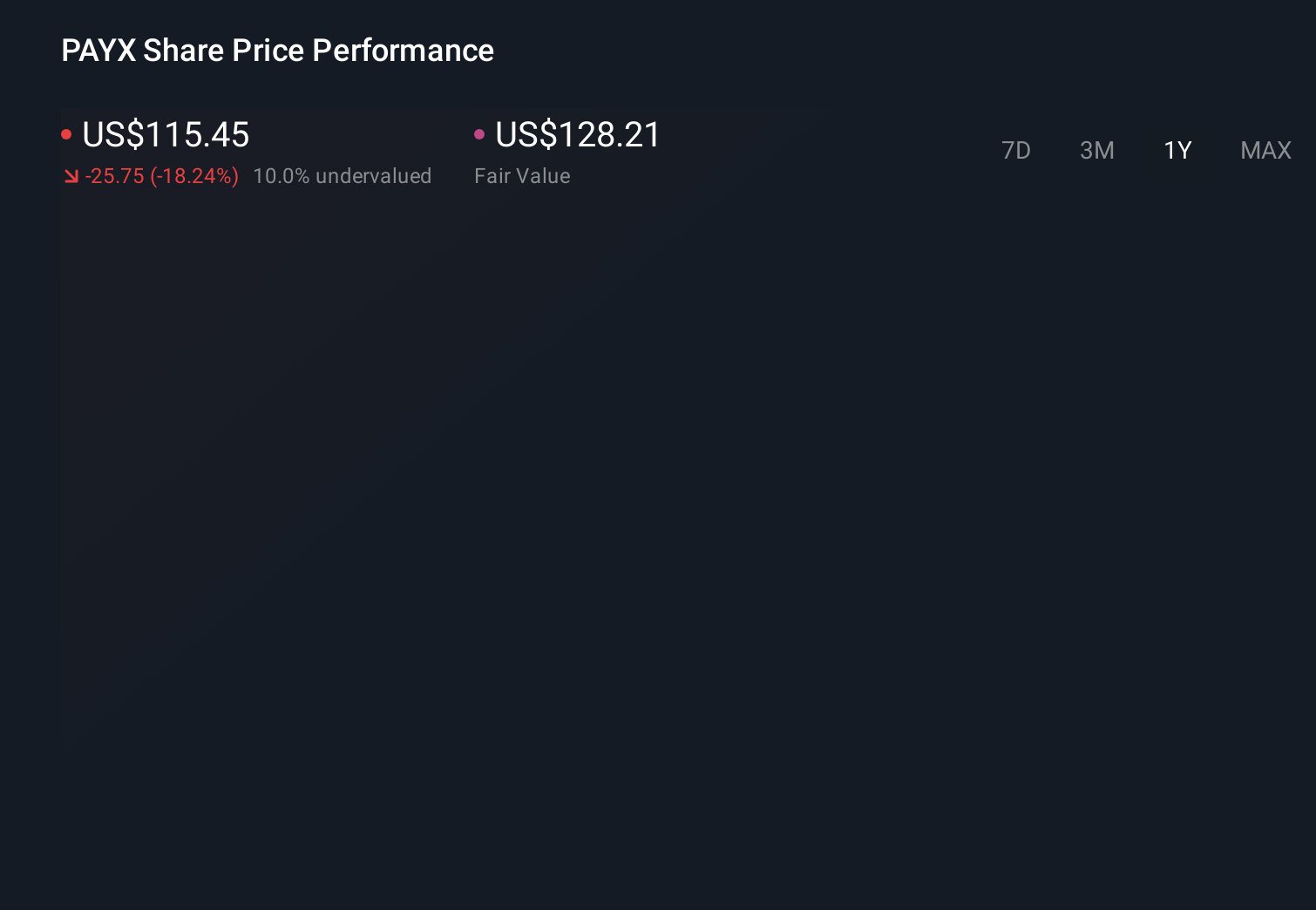

Paychex's narrative projects $7.5 billion revenue and $2.3 billion earnings by 2029. This requires 5.9% yearly revenue growth and about a $0.7 billion earnings increase from $1.6 billion today.

Uncover how Paychex's forecasts yield a $100.93 fair value, a 7% upside to its current price.

Exploring Other Perspectives

Some of the most cautious analysts were assuming Paychex would reach about US$7.4 billion of revenue and US$2.2 billion of earnings by 2029, which bakes in slower growth and a lower future valuation multiple than consensus. Compared with the more upbeat view that secular HR outsourcing and AI tools might keep supporting margins, this more pessimistic narrative shows how far expectations can differ and why it is worth weighing several viewpoints before deciding how this new dividend news fits into your own thesis.

Explore 6 other fair value estimates on Paychex - why the stock might be worth as much as 73% more than the current price!

Decide For Yourself

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Paychex research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Paychex research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Paychex's overall financial health at a glance.

No Opportunity In Paychex?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 51 companies with promising cash flow potential yet trading below their fair value.

- The future of work is here. Discover the 32 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- We've uncovered the 12 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.