هل أدت نتائج الربع الثالث القوية وعمليات إعادة شراء الأسهم الكبيرة إلى إعادة صياغة قصة ربحية شركة Paychex (PAYX)؟

بايتشيكس PAYX | 0.00 |

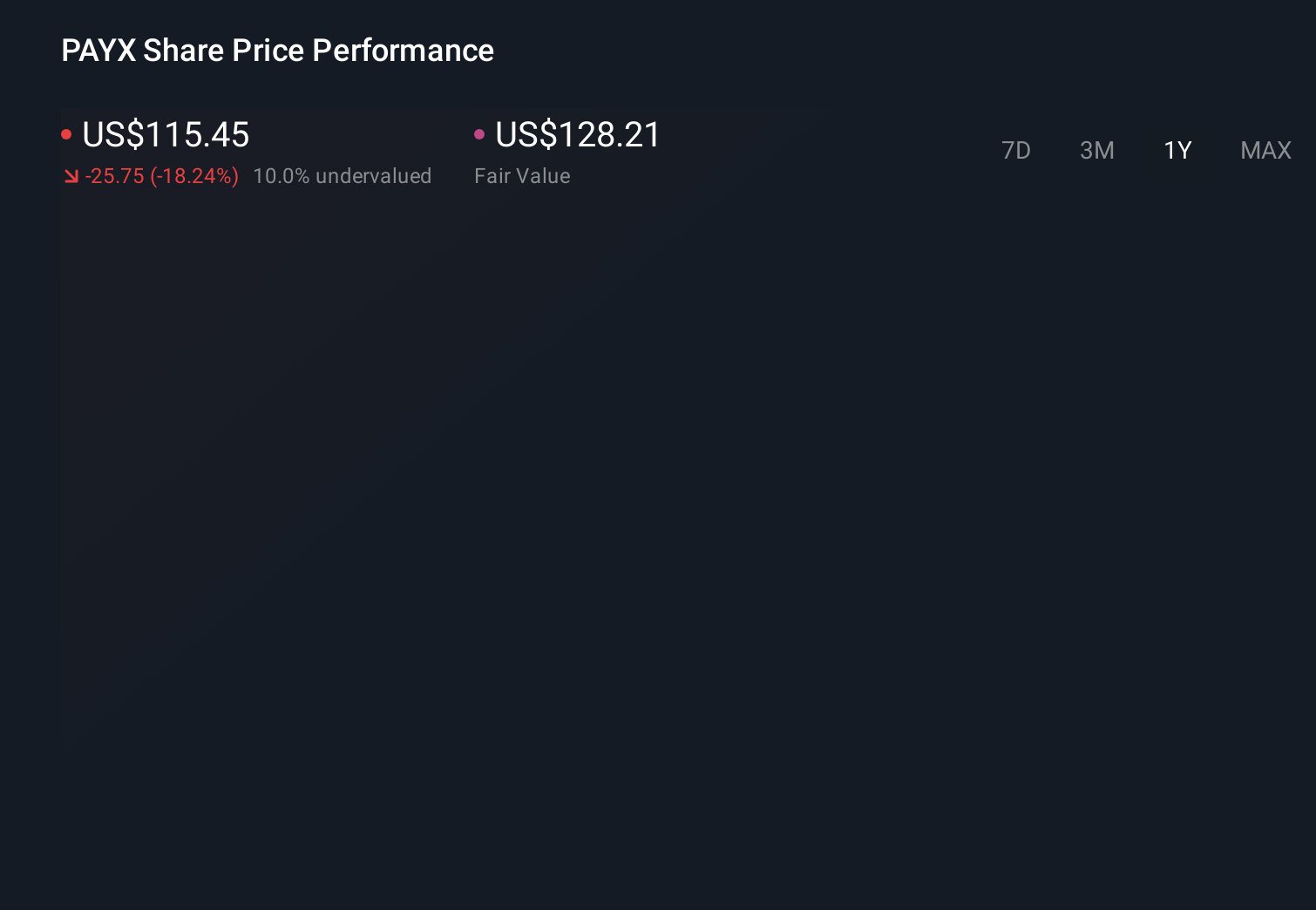

- في أواخر مارس 2026، أعلنت شركة Paychex عن إيرادات الربع الثالث بقيمة 1808.9 مليون دولار أمريكي وصافي دخل بقيمة 560.3 مليون دولار أمريكي، إلى جانب تحديثات حول إتمام عمليتي إعادة شراء أسهم بقيمة إجمالية قدرها 400 مليون دولار أمريكي و352.22 مليون دولار أمريكي، وسلطت الضوء على تركيزها على الأمن السيبراني قبل عرض تقديمي في مؤتمر RSA.

- في حين زادت الإيرادات والأرباح الفصلية للسهم الواحد على أساس سنوي، كان صافي الدخل والأرباح للسهم الواحد على مدى تسعة أشهر أقل قليلاً، مما يؤكد أن النمو في المبيعات لم يترجم بعد إلى ربحية تراكمية أعلى.

- سندرس الآن كيف يمكن لهذا المزيج من النمو الفصلي القوي، وانخفاض أرباح الأشهر التسعة الماضية، وعمليات إعادة شراء الأسهم الكبيرة أن يؤثر على سردية الاستثمار لشركة Paychex.

مستقبل العمل هنا. اكتشف أفضل 33 سهماً في مجال الروبوتات والأتمتة التي تقود مسيرة الأتمتة المدعومة بالذكاء الاصطناعي والتحول الصناعي.

ملخص سردية استثمار Paychex

لامتلاك أسهم Paychex، يجب أن تؤمن بأن منصتها الشاملة لإدارة الموارد البشرية وكشوف المرتبات، بالإضافة إلى استحواذها على Paycor ومبادراتها في مجال الذكاء الاصطناعي، قادرة على تحويل نمو الإيرادات القوي إلى أرباح مستدامة للسهم الواحد مدعومة بالسيولة النقدية. يدعم الربع الأخير هذا التوقع للإيرادات، لكن انخفاض أرباح الأشهر التسعة الماضية يُبقي مخاطر التنفيذ حاضرة. على المدى القريب، يكمن العامل المحفز الرئيسي في قدرة دمج Paycor وأدوات الذكاء الاصطناعي على رفع هوامش الربح، بينما يبقى الخطر الأكبر هو أن ارتفاع التكاليف وتباطؤ نشاط العملاء يُبقيان الأرباح ثابتة. في الوقت الحالي، لا تُغير هذه النتائج المالية جوهريًا من هذا التوازن.

أهم ما تم الإعلان عنه مؤخرًا هو إتمام عمليتي إعادة شراء أسهم بقيمة إجمالية تبلغ حوالي 752 مليون دولار أمريكي، إلى جانب برنامج جديد بقيمة مليار دولار أمريكي. في ظل عام شهد تذبذبًا في نمو الأرباح وتراجعًا في سعر السهم، يمكن لعمليات إعادة الشراء هذه أن تعزز مؤشرات ربحية السهم إذا تحسنت الأرباح، ولكنها مهمة أيضًا لأنها تستثمر جزءًا كبيرًا من رصيد الشركة النقدي والاستثماري البالغ 1.8 مليار دولار أمريكي في وقت...

تتوقع شركة Paychex تحقيق إيرادات بقيمة 7.5 مليار دولار وأرباح بقيمة 2.3 مليار دولار بحلول عام 2029. ويتطلب ذلك نموًا سنويًا في الإيرادات بنسبة 5.6٪ وزيادة في الأرباح بنحو 0.7 مليار دولار من 1.6 مليار دولار اليوم.

اكتشف كيف أن توقعات Paychex تؤدي إلى قيمة عادلة تبلغ 102.80 دولارًا ، أي بزيادة قدرها 12٪ عن سعرها الحالي.

استكشاف وجهات نظر أخرى

كان بعض المحللين الذين وضعوا أدنى التقديرات يفترضون بالفعل نموًا سنويًا في الإيرادات بنسبة 5.5% فقط وأرباحًا بقيمة 2.2 مليار دولار أمريكي بحلول عام 2029، لذا بالمقارنة مع الرأي الأكثر حذرًا الذي يرى أن قاعدة عملاء Paychex التي تضم 800 ألف عميل قد تشهد مستويات توظيف ثابتة ونموًا أبطأ في حجم العمل، فإن روايتهم أكثر تشاؤمًا بشكل ملحوظ؛ بعد قفزة الإيرادات في هذا الربع ولكن مع انخفاض أرباح الأشهر التسعة الماضية، يجدر التساؤل عما إذا كانت تلك التوقعات والمخاطر المتعلقة بالإيرادات المدفوعة بحجم العمل تبدو الآن أقرب إلى الواقع، أو أنها بحاجة إلى إعادة النظر فيها بالكامل.

استكشف 6 تقديرات أخرى للقيمة العادلة لسهم Paychex - لماذا قد تصل قيمة السهم إلى 75% أكثر من السعر الحالي!

توصل إلى استنتاجك الخاص

لا تكتفِ بمتابعة مؤشر الأسعار - تعمّق في البيانات وابنِ قناعة خاصة بك.

- تُعد تحليلاتنا التي تسلط الضوء على مكافأتين رئيسيتين وعلامتين تحذيريتين مهمتين قد تؤثران على قرارك الاستثماري نقطة انطلاق رائعة لبحثك في شركة Paychex.

- يقدم تقريرنا البحثي المجاني عن شركة Paychex تحليلاً أساسياً شاملاً مُلخصاً في رسم بياني واحد - ندفة الثلج - مما يسهل تقييم الوضع المالي العام لشركة Paychex بنظرة سريعة.

هل تبحث عن استثمارات أخرى؟

لا تفوّت فرصتك في تحقيق أرباح هائلة. إليكم أحدث اختياراتنا من الأسهم:

- قد لا تكمن أفضل أسهم الذكاء الاصطناعي اليوم في شركات عملاقة مثل إنفيديا ومايكروسوفت. اكتشف فرصتك الاستثمارية الكبيرة القادمة مع هذه الشركات الـ 21 الصغيرة المتخصصة في الذكاء الاصطناعي، والتي تتمتع بإمكانات نمو قوية بفضل ابتكاراتها في المراحل المبكرة في مجالات التعلم الآلي والأتمتة وتحليل البيانات، ما قد يضمن لك مستقبلاً مالياً مزدهراً.

- اكتشف الفرصة الكبيرة القادمة مع 32 سهمًا رخيصًا من النخبة يوازن بين المخاطرة والعائد.

- تُعدّ المعادن الأرضية النادرة عنصرًا أساسيًا في معظم الأجهزة عالية التقنية، والأنظمة العسكرية والدفاعية، والمركبات الكهربائية. ويتنافس العالم بشدة لتأمين إمدادات هذه المعادن الحيوية. اكتشف أفضل 25 شركة في مجال المعادن الأرضية النادرة، من بين الشركات القليلة التي تستخرج هذا المورد الاستراتيجي المهم.

هذا المقال من Simply Wall St ذو طبيعة عامة. نقدم تعليقاتنا بناءً على البيانات التاريخية وتوقعات المحللين فقط، باستخدام منهجية محايدة، ولا يُقصد بمقالاتنا أن تكون نصائح مالية. لا يُشكل هذا المقال توصيةً بشراء أو بيع أي سهم، ولا يأخذ في الاعتبار أهدافك أو وضعك المالي. نهدف إلى تزويدك بتحليلات طويلة الأجل مدفوعة بالبيانات الأساسية. يُرجى ملاحظة أن تحليلنا قد لا يأخذ في الاعتبار آخر إعلانات الشركات الحساسة للسعر أو المعلومات النوعية. لا تمتلك Simply Wall St أي أسهم في أي من الشركات المذكورة.