Did Surging Smoke-Free Product Sales Just Shift Philip Morris International's (PM) Investment Narrative?

Philip Morris International Inc. PM | 165.34 165.41 | +0.31% +0.04% Pre |

- In its recently reported second-quarter 2025 results, Philip Morris International announced that shipment volumes for smoke-free products, including IQOS, ZYN, and VEEV, rose 11.8%, fueling a 15.2% increase in net revenues.

- Smoke-free products now contribute 41% of total revenues and 42% of gross profit, underscoring the company's significant progress in pivoting away from traditional cigarettes.

- We'll now examine what Philip Morris International's accelerating revenue growth in smoke-free products means for its long-term investment narrative.

The end of cancer? These 26 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Philip Morris International Investment Narrative Recap

To be a shareholder in Philip Morris International today, you need confidence in its ability to manage the transition from legacy cigarettes to smoke-free products like IQOS, ZYN, and VEEV. The latest quarter’s strong smoke-free revenue growth supports the main short-term catalyst, accelerated adoption of reduced-risk products as traditional cigarette volumes decline. However, regulatory pressures, illicit trade, and lingering exposure to combustibles remain material risks; this recent performance doesn’t meaningfully reduce those risks but demonstrates tangible progress.

Among recent announcements, the launch of IQOS ILUMA earlier this year stands out as particularly relevant, showcasing the company’s ongoing investment in product innovation to strengthen its smoke-free segment. This aligns closely with the current catalyst: scaling smoke-free alternatives to offset combustible revenue declines and support margin expansion, especially as margins for these products already significantly exceed those of traditional lines.

Yet, against the optimism, investors should be aware that challenges tied to regulatory risk and illicit trade are increasingly coming into focus...

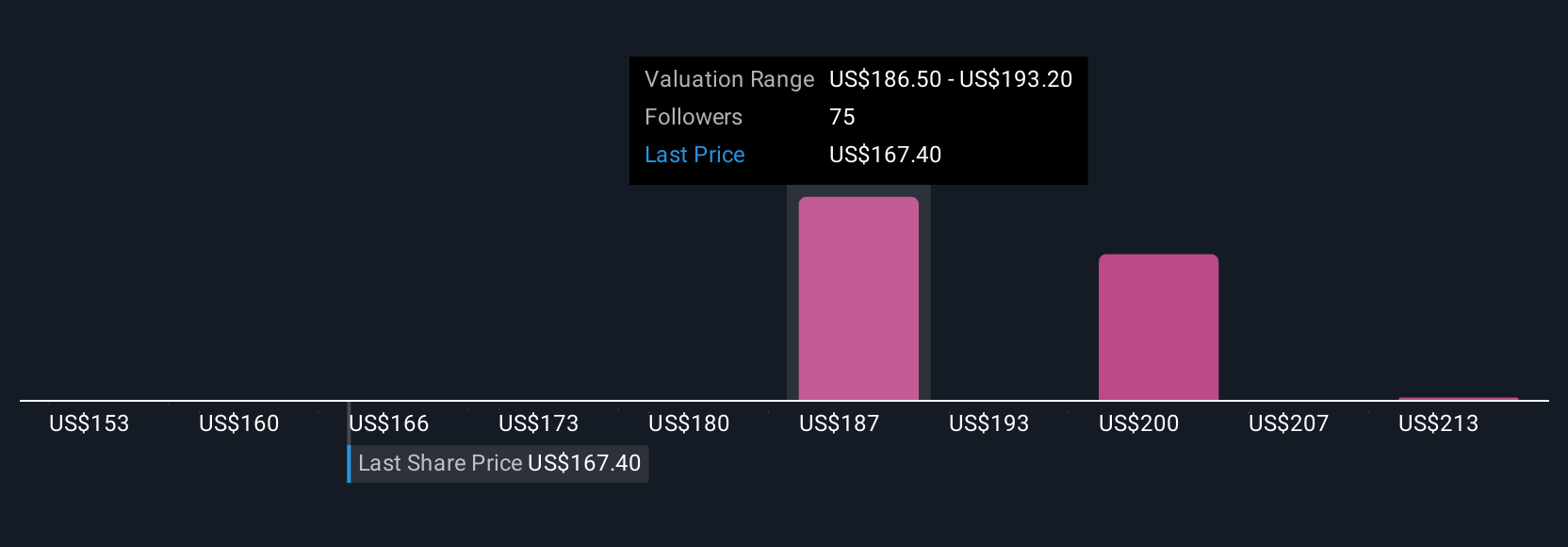

Philip Morris International’s outlook projects $49.4 billion in revenue and $14.5 billion in earnings by 2028. Achieving these targets requires 8.2% annual revenue growth and a $6.3 billion increase in earnings from the current $8.2 billion.

Uncover how Philip Morris International's forecasts yield a $190.20 fair value, a 14% upside to its current price.

Exploring Other Perspectives

The most pessimistic analysts forecasted Philip Morris International would achieve just US$47.1 billion in revenue and US$14.4 billion in earnings by 2028, citing regulatory and public health headwinds as key risks. While these expectations reflected a much more cautious outlook before this quarter’s smoke-free surge, opinions vary widely. You should consider how new growth trends might shape both the bullish and bearish cases going forward.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth as much as 32% more than the current price!

Build Your Own Philip Morris International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Philip Morris International research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Seeking Other Investments?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- This technology could replace computers: discover 23 stocks that are working to make quantum computing a reality.

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.